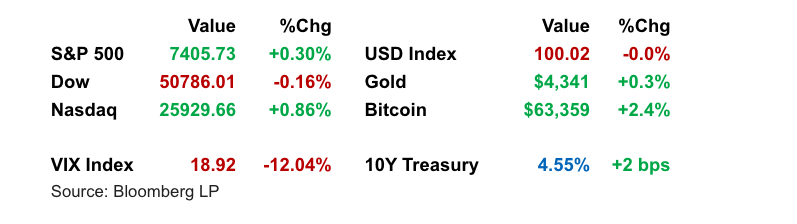

Wall Street recovered from Friday’s steep decline as dip buyers returned to the AI trade, led by a sharp rebound in semiconductor shares. The S&P 500 rose modestly and the Nasdaq outperformed, though market breadth was softer beneath the surface as most S&P 500 constituents declined. Sentiment was helped by easing oil-price pressure after Iran and Israel halted strikes, while Treasury yields edged higher as investors looked ahead to Wednesday’s inflation report.

Key Headlines & Market Movers:

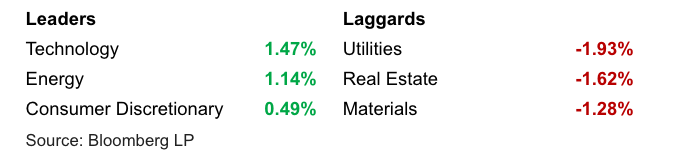

- Chip Stocks Revive AI Momentum: Semiconductor stocks rebounded sharply after their worst selloff since 2020, with Nvidia, Micron, Intel, and Marvell among the key gainers. Intel surged on reports that Google may rely on the company for millions of specialized AI chips in 2028, while Marvell rallied after being added to the S&P 500. The move reinforced investor confidence that the AI infrastructure buildout remains a durable market theme despite last week’s volatility.

Strategists Frame Selloff as a Healthy Reset: Morgan Stanley and Citi strategists leaned constructive, arguing that last week’s positioning-driven decline looked more like a pause than the start of a broader downturn. Morgan Stanley’s Mike Wilson maintained an upbeat year-end S&P 500 target, while Citi raised its target after stronger earnings expectations. UBS also argued that markets may be overstating central-bank hawkishness, with solid fundamentals still supporting risk assets.

Oil Eases as Geopolitical Tensions Cool: Crude prices initially jumped after Iran and Israel exchanged military strikes, but gains faded after both sides signaled a halt to attacks. That helped reduce one immediate risk for equities, even as WTI remained above $90 a barrel. The easing in energy pressure came at an important moment, with investors already focused on whether inflation data will complicate the outlook for Federal Reserve policy.

S&P 500 Sector Performance

Looking Ahead

The next major test is Wednesday’s May CPI report, with headline inflation expected to accelerate while core monthly inflation may cool slightly. A softer core reading could reassure investors that the Fed does not need to turn more hawkish despite strong job growth, while a hotter print would likely pressure rate-sensitive and high-valuation growth stocks. Markets will also watch whether demand for major IPOs, equity offerings, and corporate bond deals confirms that risk appetite remains intact after last week’s reset.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

%20plans.png)

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119