For most people planning for retirement, deciding how much to invest in stock funds versus bond funds is a key part of long-term investing. Stock funds can help your money grow, while bond funds often provide steady income, spread out risk, and add stability. The real challenge isn’t choosing stocks or bonds once and sticking with it forever—it’s finding a mix that matches your goals, timeline, comfort with risk, and need for stability as life changes.

Asset allocation—deciding how much of your money goes into stocks, bonds, and cash—is a personal choice. According to Investor.gov, the best allocation depends on how long you plan to invest and how much risk you can handle. FINRA puts it simply: it’s about splitting your investments among different asset types. For most people, figuring out the right stock-and-bond mix is the first step toward balancing growth with stability.

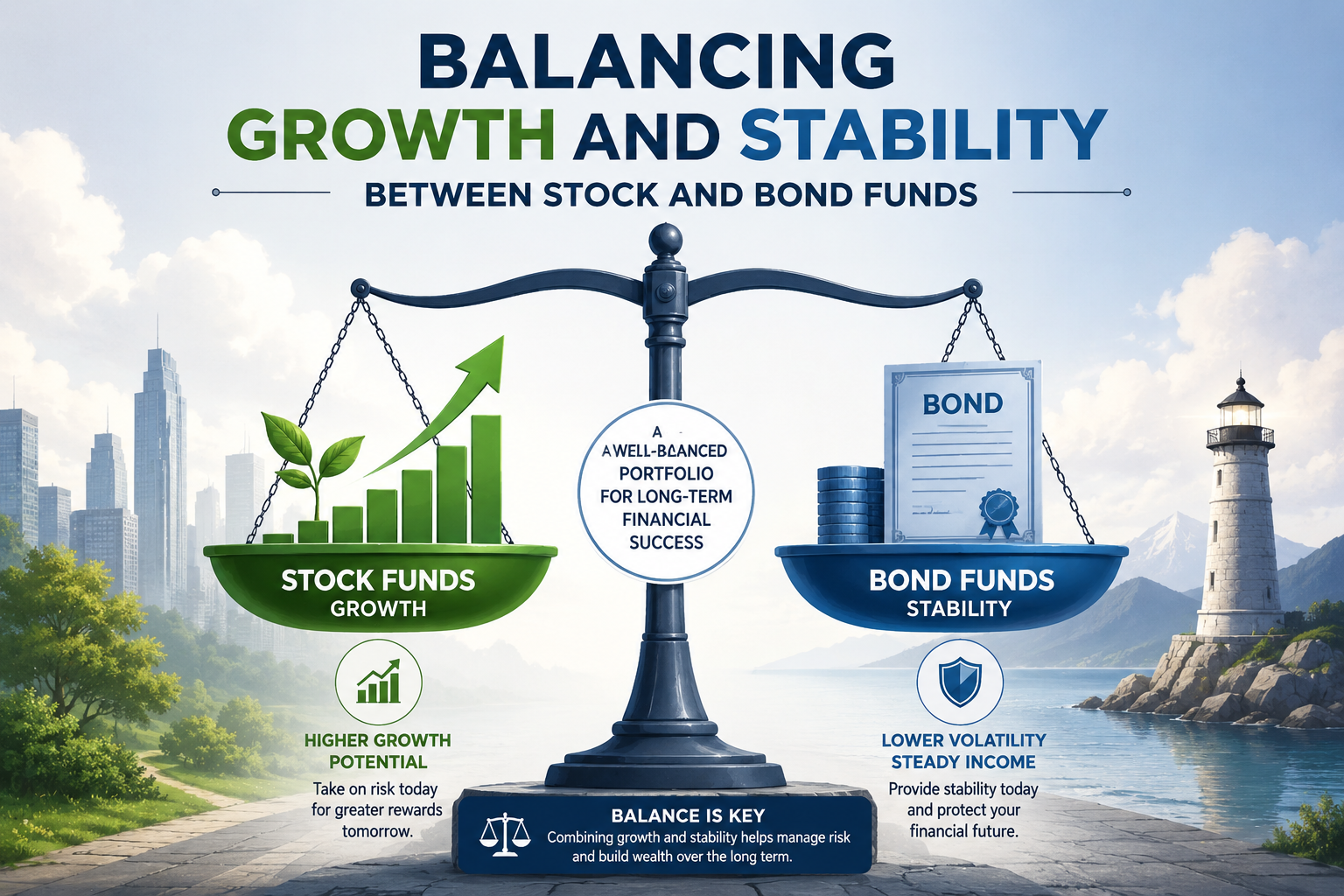

Why stock funds are often used for growth

Stock funds let you invest in companies that could grow over time. Historically, stocks have carried higher risk than bonds or cash, meaning their prices can rise and fall significantly. But over long periods, stocks have also offered the highest returns. This growth potential is especially important for long-term goals like retirement, where you want your money to grow as much as possible over many years.

But there’s a tradeoff: stocks can swing up and down a lot in the short term. In fact, big company stocks have lost money about one out of every three years. If you have a long time before retirement, you might be able to handle these ups and downs more easily, since you have time to recover from market drops.

That doesn’t mean every long-term investor should have the same amount in stocks. Risk tolerance isn’t just about what you can afford to lose—it’s also about what will keep you comfortable enough to stick with your plan. Even if a high percentage in stocks looks good on paper, it may not work if you’re likely to panic and sell during a downturn.

Why bond funds are often used for stability and income

Bond funds—sometimes called income funds—mainly invest in various types of bonds, such as government and corporate bonds. Bonds usually do not fluctuate in value as much as stocks, so they tend to carry less risk of sudden losses. However, because bonds are less risky, their average returns are also usually lower. Many people use bond funds to add more predictability to their investments and help provide stable returns over time.

However, bond funds are not risk-free. Risks include credit risk (the possibility that a bond issuer will default on its obligations) and interest rate risk (the risk that bond values decline if interest rates rise). You can lose money in a bond fund if these risks become reality.

Even bond funds that seem very safe, like ultra-short bond funds, can lose value—especially when interest rates go up. This is because when new bonds pay more interest, older bonds become less valuable. Also, unlike money in a bank account, these funds aren’t insured by the government. So, while bonds can be less risky than stocks, they do not guarantee a profit.

How the mix balances two needs

Mixing stocks and bonds balances two needs: growing your money and protecting it from swings. Stocks boost long-term growth, while bonds provide steadiness. Often, when stocks decline, bonds hold up better, so owning both helps manage risk.

By owning investments that don’t all move the same way, you can reduce risk and smooth out returns. If one part of your portfolio struggles, another can help offset losses. That’s the idea behind mixing stock and bond funds.

Even a portfolio that includes many different investments cannot eliminate all risks. Diversification—owning different types of investments—helps reduce the risk of large losses from any single asset. However, it cannot protect you from losses when the entire market declines, since both stocks and bonds can sometimes fall at the same time.

Let's consider how your investing time frame may affect your stock-bond balance.

How long you plan to invest—your time horizon—is key when deciding your stock-bond split. If you have many years before you’ll need the money, you may feel comfortable taking on more risk, knowing you have time to recover from market ups and downs.

As you get closer to retirement, your priorities may change. Most people gradually shift to more bonds and less stock—not because bonds are risk-free, but because having less volatility matters more when you’re getting ready to use your savings and don’t have as much time to bounce back from losses.

Target-date or lifecycle funds are built to handle these changes automatically—they gradually shift from stocks to bonds as you approach your retirement date. Even so, it’s still worth checking that any fund’s strategy, costs, and risk level make sense for your own situation.

Why risk tolerance and behavior matter

Two people with the same retirement date might need different mixes of stocks and bonds. One might be fine with big ups and downs for bigger long-term gains, while another might want a smoother ride to avoid feeling anxious during rough markets.

Risk tolerance is about both your financial ability to take losses and your emotional comfort with possible declines in value. For example, if having too much in stocks causes stress or makes you want to sell during a market drop, you might have too much stock, even if you have many years before retirement. Being honest about your comfort with risk helps prevent making decisions you’ll regret when markets are volatile.

Bond funds can help steady your portfolio, but not all bond funds are alike. Some are safer and less volatile, while others can be riskier and offer higher returns. It’s important to know what kind of bond fund you’re choosing and how it fits your goals.

Once your mix is chosen, how do you keep it on track over time?

Even if you pick the perfect stock-bond mix, it won’t stay that way on its own. Some investments will grow faster than others, and over time, your portfolio can drift away from your original plan.

Rebalancing means bringing your portfolio back to your intended mix. This could mean changing where new contributions go, moving money between funds, or using features that automatically do this for you—like some 401(k) plans offer.

Rebalancing isn’t about guessing which investment will do best next. Instead, it’s about keeping your portfolio in line with your plan, not chasing what’s hot at the moment.

Questions investors can ask over time

Your ideal mix of stock and bond funds can change as you get closer to retirement, your finances shift, or your comfort with risk changes. Here are some good questions to ask yourself along the way:

· What is the purpose of this account? A retirement account with a multi-decade time horizon may support greater growth exposure than the near-term funds needed.

· How much volatility can the investor withstand? Investor.gov emphasizes that risk tolerance includes both ability and the willingness to accept potential losses in pursuit of higher returns (Investor.gov).

What role should bond funds play? Bond funds may offer income and diversification, but they also carry risks. For example, bond funds can lose value due to credit risk (if issuers can’t pay back) and interest rate risk (if rising rates reduce bond values), as outlined by Investor.gov.

· Has the portfolio drifted? FINRA notes that rebalancing can help realign holdings with the original allocation after market performance changes the values of asset classes (FINRA).

· Do the funds overlap? FINRA notes that investors should make sure pooled investments are themselves diversified because owning multiple funds that invest in the same subclass may not provide meaningful diversification (FINRA).

Bottom line

Balancing stocks and bonds is really about matching your need for growth and stability to your long-term plan. Stocks can help you reach your retirement goals by growing your savings, while bonds can help smooth out the ride. The right mix depends on how long you’ll invest, your comfort with risk, your income needs, and your ability to stick with your plan when the market gets rocky.

It’s also smart to revisit your mix regularly—especially as retirement gets closer, you start withdrawing money, or your life circumstances change. A financial advisor can help you check if your stock and bond funds are still doing what you need them to do.

Source URLs

· https://www.finra.org/investors/investing/investing-basics/asset-allocation-diversification

· https://www.sec.gov/about/reports-publications/investorpubsultra-short_bond_fundshtm

This material is provided for informational and educational purposes only and should not be construed as personalized investment, tax, legal, retirement plan, or financial planning advice. The information does not constitute a recommendation to buy, sell, hold, or change any security, fund, asset allocation, or investment strategy. Stock funds and bond funds involve risk, including the possible loss of principal. Bond funds are subject to risks that may include interest rate risk, credit risk, prepayment risk, liquidity risk, and market risk. Asset allocation, diversification, and rebalancing do not assure a profit or protect against loss in declining markets. Past performance is not indicative of future results. Investors should consider their goals, risk tolerance, time horizon, income needs, financial circumstances, fees, and the specific options and rules available within their retirement plan before making investment decisions. Investors should consult their financial advisor, tax professional, or retirement plan representative before making changes to a 401(k) account or other investment portfolio.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119