If the market dropped 25% this year, would your life plans still feel okay—or would everything suddenly be on hold? This isn’t about what’s on the news. It’s about whether your investments fit your real goals, your life’s timing, and how you really feel about risk.

Quick gut check

- What is each account for? (Retirement, a future home, college, or just a safety net?)

- When will you need the money?

- Could you stay invested if the market takes a dip, or would you want to pull the plug?

If your portfolio and your answers don’t line up, your risk might be out of sync with your real life.

Red Flags: Signs Your Risk Level Isn’t Right

- Most of the money you’ll need in the next 1–3 years is in stocks.

- You lose sleep or feel anxious when the market drops.

- You’re within 5–10 years of retirement but your investments are still set up like you’re just starting out.

- You’ve had major life changes (like marriage, kids, job changes, or health issues) but haven’t updated your portfolio in years.

If you see yourself in two or more of these, it might be time to take another look at your investments.

Money you need soon (0–3 years)

Short-term money is your “do not gamble” money. Think down payments, tuition that’s due soon, or a big purchase you know is coming up.

- Priority: Stability and liquidity.

- Typical approach: More cash and short‑term bonds, much less in stocks.

A big market drop right before you need the money can throw your plans off track if this bucket is too aggressive.

Money you won’t touch for a while (10+ years)

Long-term money—like retirement in 15, 20, or 30 years—usually needs room to grow. If you play it too safe here, you might come up short later.

- Priority: Growth that outpaces inflation.

- Typical approach: More stocks for growth, with bonds and cash for balance.

The real question: Can you ride out the market’s ups and downs without bailing at the worst possible moment?

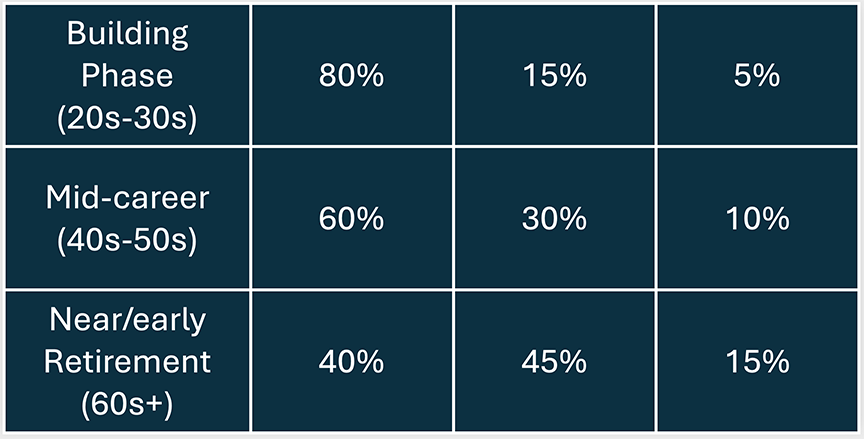

Simple example allocation (illustrative only)

This isn’t a recommendation—just an example of how your risk level might change as you move through different stages of life.

Your actual investment mix should fit your personal goals, your full financial picture, your comfort with risk, and your timeline.

Three actions to take today

1. Label each account with its purpose

- Write down what each account is for and when you expect to use that money.

2. Compare goal timing vs. risk

- Short-term goals: Make sure you’re not keeping too much in risky assets.

- Long-term goals: Check that you still have enough invested for growth

3. Run the “sleep test”

- If a normal market dip would make you want to sell everything, your portfolio may be taking more risk than you’re comfortable with.

Bringing your risk level in line with your real life isn’t about chasing the biggest returns. It’s about making sure your money is there when you need it, so you can live the life you really want.

Disclosure

This material is provided for informational and educational purposes only and is not intended as, and should not be construed as, investment, legal, tax, or accounting advice. It does not take into account the specific investment objectives, financial situation, or particular needs of any individual investor. Any references to asset allocation models, example portfolios, or “rules of thumb” are purely illustrative and are not recommendations to buy, sell, or hold any security or to adopt any particular investment strategy.

Investing involves risk, including the possible loss of principal. Equity investments are subject to market volatility; the value of an investor’s shares may fluctuate and, when sold, may be worth more or less than their original cost. Fixed‑income investments are subject to interest‑rate, credit, and inflation risk. Cash and cash‑equivalent investments may lose purchasing power over time due to inflation. Diversification and asset allocation do not ensure a profit or protect against loss in declining markets.

Past performance is not indicative, or a guarantee, of future results. All examples are hypothetical and are for illustrative purposes only. They do not represent the performance of any specific investment, index, or strategy and do not reflect fees, expenses, or taxes that an investor may incur.

Sources

- Vanguard model asset allocation examples:

https://investor.vanguard.com/investor-resources-education/education/model-portfolio-allocation - Charles Schwab: Retirement portfolio asset allocation by age:

https://www.schwab.com/learn/story/retirement-portfolio-assets-allocation-by-age - SoFi: Asset allocation by age and time horizon:

https://www.sofi.com/learn/content/asset-allocation-by-age/ - Capital Group: Sample asset allocation details:

https://www.capitalgroup.com/individual/planning/retirement-planning/sample-asset-allocations/sample-details.html - TIAA: Five steps to finding your ideal investment mix (PDF):

https://www.tiaa.org/public/pdf/Asset_Allocation_Guide_A38473.pdf

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119