For many of us, checking our 401(k) has become as routine as checking the weather. With just a few taps on your phone, you can see if your retirement savings are up, down, or holding steady. While this convenience is great, it also raises an important question:

How often should you actually look at your 401(k)?

The answer isn’t simply about numbers or picking the perfect time to invest. More often, it’s about our behavior, emotions, and how we react to the market’s ups and downs.

There may not be one “correct” schedule for everyone. Some investors feel more comfortable reviewing their accounts regularly, while others prefer to step back and focus toward long-term goals. What matters most is understanding how review frequency can influence decision-making.

The Emotional Side of Investing

A 401(k) is meant to help you save for the long haul. But the market moves all the time—sometimes by the hour. If you check your account too often, it’s easy to go from thinking long-term to reacting to every little change.

Studies show that we tend to feel losses much more strongly than gains. So, when the market dips, it can feel like a big deal—even if it’s just temporary. On the other hand, good news never seems quite as exciting.

These emotional swings can lead us to make spur-of-the-moment decisions, like:

- Moving investments to cash in downturns

- Reducing contributions after market declines

- Chasing performance after strong rallies

- Attempting to “time” the market

Over time, people who react emotionally to market swings often miss out on the market’s long-term gains. Research shows that making changes out of fear or thrill can actually hurt your returns in the long run.

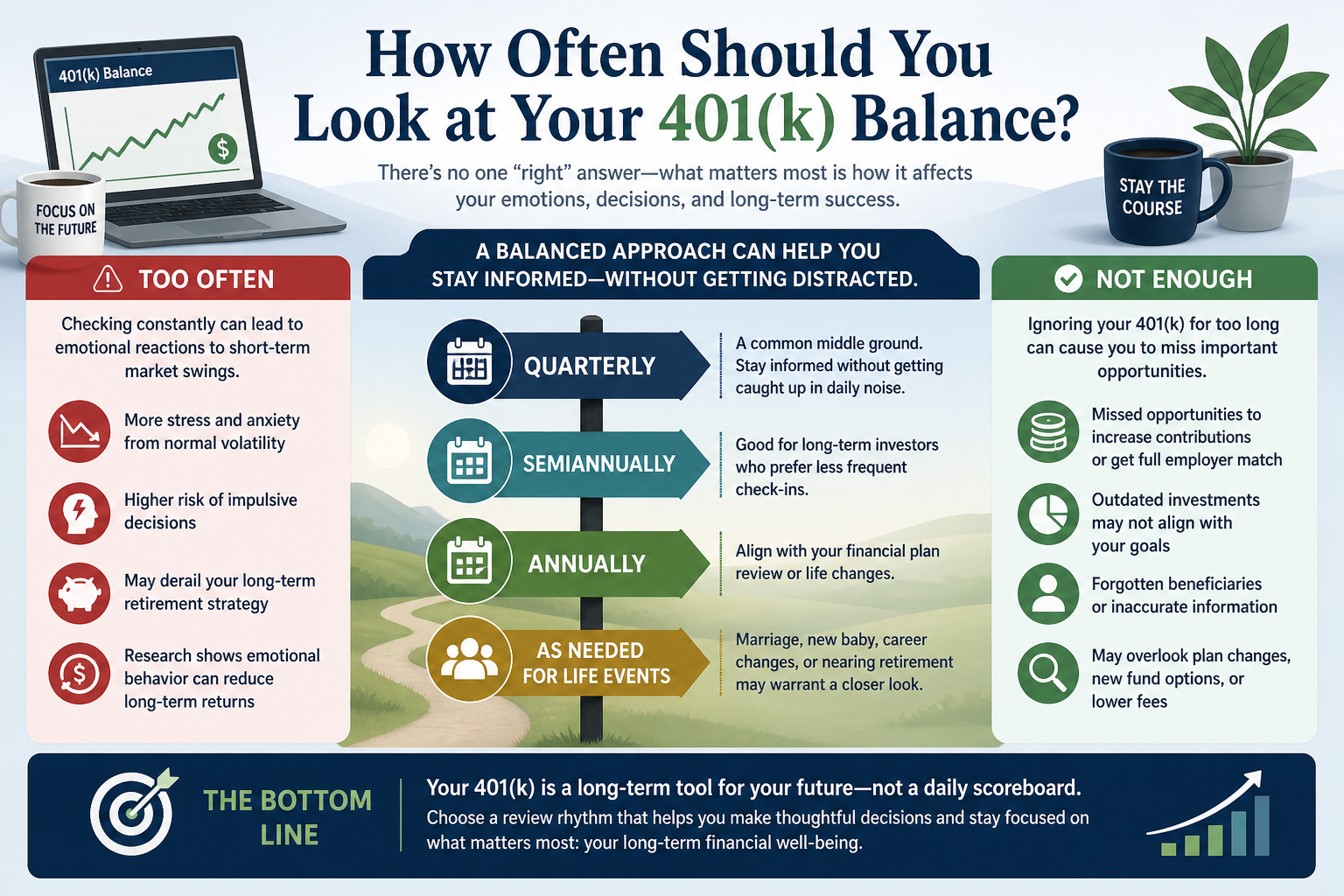

Why Frequent Checking Can Feel Stressful

It’s normal for the market to go up and down every day. But the more you check your balance, the more likely you are to see those short-term drops—and worry about them.

Some behavioral studies have illustrated this idea clearly. One analysis noted that checking a portfolio daily significantly increases the likelihood of seeing losses compared with reviewing it less frequently.

That doesn’t mean you should ignore your 401(k) completely. It just means that checking too often can ramp up your anxiety when markets get rocky.

When the market is rough, checking every day can fool you into thinking you need to act right away—even if your long-term plan is still on track.

The Case for Regular Reviews

On the other hand, completely ignoring a 401(k) may create different problems.

Periodic reviews can help investors:

- Confirm contribution levels

- Monitor employer matching contributions

- Review beneficiary designations

- Evaluate investment allocations

- Rebalance when appropriate

- Modify plans after major life changes

Marriage, divorce, a new child, career changes, or approaching retirement may all justify reviewing retirement strategies more carefully.

Additionally, employers occasionally modify investment menus, add new target-date funds, or lower plan expenses. Investors who never review their accounts could miss opportunities to improve their overall retirement strategy.

Quarterly Reviews Are Common—But Not Universal

Some financial professionals suggest quarterly reviews as a reasonable middle ground. Quarterly check-ins may provide enough oversight to remain kept informed without becoming consumed by daily market noise.

Others may prefer:

- Monthly reviews during active saving years

- Semiannual reviews for long-term investors

- Annual comprehensive retirement checkups

How often you check really depends on your personality, how much risk you’re comfortable with, and how you handle your emotions.

For example:

- An investor prone to panic in downturns may benefit from checking less often.

- A highly engaged investor who can remain disciplined during volatility may feel comfortable reviewing balances more frequently.

- Investors nearing retirement sometimes monitor accounts more closely because withdrawals may soon begin.

The real question is whether checking your account helps you plan better—or just makes you more anxious.

Long-Term Investors Frequently Gain From Staying the Course

Recent retirement data from Fidelity and Vanguard continue to strengthen the value of long-term participation in retirement plans. Average 401(k) balances increased meaningfully in 2025 as markets recovered and consistent contributions continued.

Importantly, many retirement savers who maintained regular contributions through phases of uncertainty benefited from market rebounds over time.

Fidelity reported that only a relatively small percentage of participants changed their asset allocations during periods of market turbulence, suggesting many investors maintained a long-term perspective.

This strengthens a broader principle of retirement investing: consistency often matters more than constant activity.

Technology Has Changed Investor Actions

Mobile apps and real-time account access have transformed the retirement experience. In previous decades, investors might have reviewed retirement statements quarterly by mail. Today, balances can be checked several times a day.

Convenience can be valuable, but constant visibility may also amplify emotional reactions to ordinary market swings.

Some investors intentionally reduce notifications or avoid frequent app checks at volatile markets. Others prefer automated contributions and target-date funds specifically because they help reduce the temptation to make emotional decisions.

Fidelity data shows strong adoption of target-date funds among younger investors, reflecting a wider preference for more automated, long-term retirement management.

A Better Question Than “How Often?”

Instead of asking, “How often should I check my 401(k)?,” a more useful question may be:

“How do I typically react when I check it?”

If reviewing an account encourages disciplined planning, savings increases, and thoughtful adjustments, frequent reviews may not be harmful.

But if every market decline creates stress or a desire to make drastic changes, less frequent monitoring may support better long-term decision-making.

Retirement investing isn’t simply about the numbers you see on a screen. It’s about managing your expectations, emotions, and habits through market ups and downs that can last for years.

Final Thoughts

There is no universally perfect schedule for reviewing a 401(k). Some investors prefer monthly oversight, others quarterly reviews, and some annual checkups tied to financial planning meetings.

What matters most is finding a routine that helps you stay disciplined for the long run—instead of reacting emotionally in the short term.

Markets will always rise and fall, and your retirement account will go up and down, too. But for most people, the real risk isn’t the market—it’s making emotional decisions in response to those ups and downs.

Sources

- Fidelity Retirement Analysis: Fidelity Q4 2025 Retirement Analysis

- Fidelity Retirement Data & Insights: Fidelity Retirement Analysis Data

- InvestmentNews – Vanguard & Fidelity 401(k) Trends: InvestmentNews Retirement Savings Report

- Investopedia – Portfolio Review Frequency: How Often Should You Really Check Your Portfolio?

- Investopedia – Reviewing Your 401(k): How Often Should You Review Your 401(k)?

- Yahoo Finance – Behavioral Investing & Portfolio Monitoring: Stop Checking Your Portfolio Every Day

- AOL Finance – Investor Psychology & Portfolio Checks: Why Experts Say to Stop Checking Your 401(k) Balance Constantly

Disclosure

This article is for informational purposes only and should not be considered investment, tax, or legal advice. Past market performance does not guarantee future results. Investors should consult with their financial advisor, tax professional, and other qualified professionals regarding their individual financial situation and retirement planning needs. Advisory services are offered through a Registered Investment Advisor (RIA).

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119