Managing Social Security and 401(k) income can feel overwhelming, but the main challenge is tracking one key number: your combined (or provisional) income. This figure determines how much of your Social Security benefits are taxed and helps shape the tax impact of your 401(k) withdrawals. With thoughtful planning—deciding when to claim Social Security, how much to withdraw from your 401(k), and which accounts to use—you can avoid unexpected tax bills and keep more of your retirement income.

How combined income affects Social Security taxes

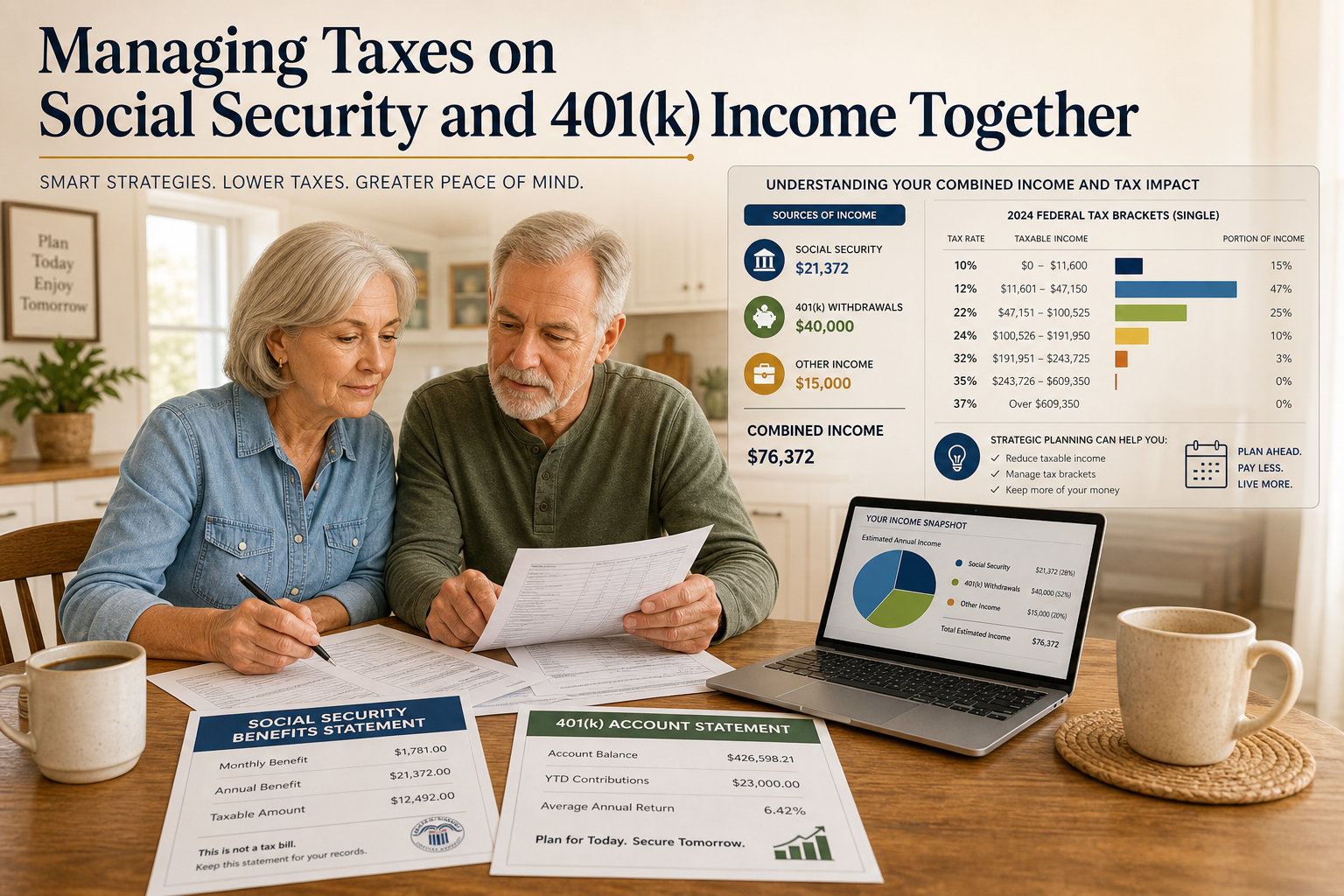

The IRS does not tax all Social Security benefits; instead, it looks at your combined (provisional) income and then decides what percentage of your benefit is taxable. For this calculation, combined income is defined as:

[\text{combined income} = \text{MAGI} + 50% \times \text{Social Security benefits}]

Here, MAGI (modified adjusted gross income) includes things like 401(k)/IRA withdrawals, pensions, wages, interest, dividends, and some tax‑exempt interest.

Current thresholds work roughly like this:

- Single filers

- Less than 25,000 combined income → 0% of benefits taxed

- 25,000–34,000 → up to 50% taxed

- Above 34,000 → up to 85% taxed.

- Married filing jointly

- Less than 32,000 combined income → 0% of benefits taxed

- 32,000–44,000 → up to 50% taxed

- Above 44,000 → up to 85% taxed.

These thresholds are not indexed to inflation, so more retirees are pulled into paying tax on their benefits over time.

Where 401(k) withdrawals fit in

Traditional 401(k) withdrawals are taxed as ordinary income, and they are a key driver of your combined income number. Every taxable dollar you pull from a traditional 401(k) or traditional IRA adds to MAGI, which can push a larger share of your Social Security into the taxable category and can push you into a higher federal tax bracket.

- It can push you into a higher federal tax bracket.

By contrast, withdrawals from Roth IRAs or Roth 401(k)s (if qualified) are generally tax‑free and do not count in MAGI or combined income, which makes them useful tools for getting cash without increasing Social Security taxation.

Required minimum distributions (RMDs) from traditional 401(k)s and IRAs begin at age 73 (75 for those born in 1960 or later), and those mandated withdrawals can suddenly increase MAGI and trigger tax on benefits if you haven’t planned ahead.

Practical strategies to manage both together

Several widely used strategies focus on shaping combined income over time rather than just reacting year by year:

- Delay Social Security and use a 401(k) as a bridge.

Some retirees delay claiming Social Security to increase their benefit and use controlled 401(k)/IRA withdrawals for income in the meantime. This can help do Roth conversions and spend down tax‑deferred balances before RMDs start, reducing later combined income. - Building up Roth and taxable investment accounts before retirement gives you more flexibility: you can choose whether a given year’s income comes from fully taxable sources (traditional 401(k)), partially taxable sources (taxable brokerage), or non‑taxable sources (Roth). That mix helps you keep your combined income under key thresholds.

- Coordinate withdrawals year by year.

Once you are collecting Social Security, you can pull more from Roth accounts or from low‑gain taxable holdings in years when other income is high, and tap traditional 401(k) more in lower‑income years. The goal is to avoid spikes that cause 85% of your benefits to be taxed. - Watch state taxes too.

Some states tax 401(k)/IRA withdrawals but exempt Social Security; others tax both or neither. Where you live can therefore change how painful combined income is on an after‑tax basis.

Even a simple example—say, 40,000 dollars of 401(k) withdrawals plus 18,000 dollars in Social Security benefits—shows how the system works: 58,000 dollars of combined income can easily cross the thresholds that make up to 85% of benefits taxable if you don’t manage the mix.

Disclosure

This article is for informational and educational purposes only and does not constitute personalized tax, investment, financial, or legal advice. It reflects general rules that may change over time and may not apply to your specific situation. Readers should consult a qualified tax professional or financial advisor before making decisions about Social Security, 401(k) withdrawals, Roth conversions, or any retirement‑income strategy.

Sources:

- https://www.ssa.gov/benefits/retirement/planner/taxes.html

- https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-required-minimum-distributions-rmds

- https://www.fidelity.com/learning-center/personal-finance/retirement/social-security-taxation

- https://www.kiplinger.com/retirement/social-security/603106/what-is-pr

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119