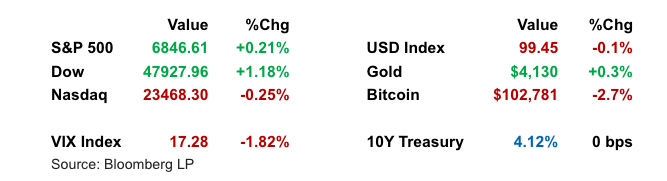

Markets advanced Tuesday as momentum built around the likely end of the historic U.S. government shutdown. The Dow led with a 1.2% gain, closing at a record high, while the S&P 500 edged higher and the Nasdaq dipped slightly amid pressure on tech stocks. Optimism that a funding resolution will restore access to economic data boosted confidence in the Fed’s policy outlook. With liquidity still robust and corporate commentary upbeat, investor sentiment leaned constructive despite tech sector volatility.

Key Headlines & Market Movers:

- Shutdown Resolution in Sight Spurs Rally: Investors welcomed signs that the 42-day federal government shutdown could end as soon as Wednesday. The Senate passed a temporary funding bill, and the House is expected to follow. This would reopen agencies and potentially allow delayed economic data, such as the September jobs report, to be released as early as next week. The return of official data could clarify the Fed's policy path and support GDP forecasts. Markets responded favorably, particularly cyclical names like FedEx and industrials.

Tech Stocks Mixed as AI Enthusiasm Faces Growing Scrutiny: The tech sector lagged, with Nvidia falling 3% following news that SoftBank exited its $5.8B stake to fund AI investments. AMD also slipped ahead of its analyst day, while CoreWeave plunged 16% on weak guidance. Broader tech sentiment remains constructive due to strong AI capex trends, but growing scrutiny over spending efficiency and valuation is driving near-term volatility. Investors appear to be recalibrating expectations ahead of Nvidia’s earnings next week, a key event for the sector.

- Corporate Commentary Stays Upbeat Despite Data Vacuum: Executives across sectors struck a surprisingly optimistic tone this earnings season. Mentions of “economic slowdown” have dropped to their lowest since 2007, reflecting underlying confidence in demand and margin resilience. Companies like Microsoft, Alphabet, and Meta continue to ramp up AI infrastructure investment, while broader industrial and consumer names (e.g., FedEx, Merck, Nike) delivered supportive guidance, reinforcing hopes for a strong Q4 earnings backdrop.

Liquidity, Rate Cut Hopes Fuel Year-End Rally Expectations: Market strategists maintain a bullish stance, citing robust liquidity, resilient earnings, and expectations for Fed easing, possibly starting as soon as December. JPMorgan reiterated its tactical bullish call, while UBS and Wells Fargo pointed to AI and tech capex as structural drivers of growth. While market breadth remains narrow, many see the potential for broader participation into year-end if macro data supports a softer Fed trajectory.

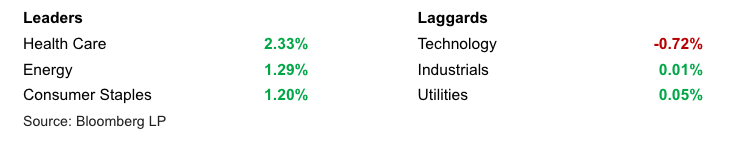

S&P 500 Sector Performance

Looking Ahead

The market’s next focus turns to the House vote on the shutdown bill and the potential resumption of delayed economic data. Nvidia’s earnings on Nov. 19 will serve as a critical test for AI-related momentum. While short-term choppiness in tech may continue, broader sentiment remains constructive into year-end, especially if the Fed signals a more dovish tilt. Traders appear intent on preserving the year-end rally theme unless disrupted by unexpected macro or geopolitical shocks.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119