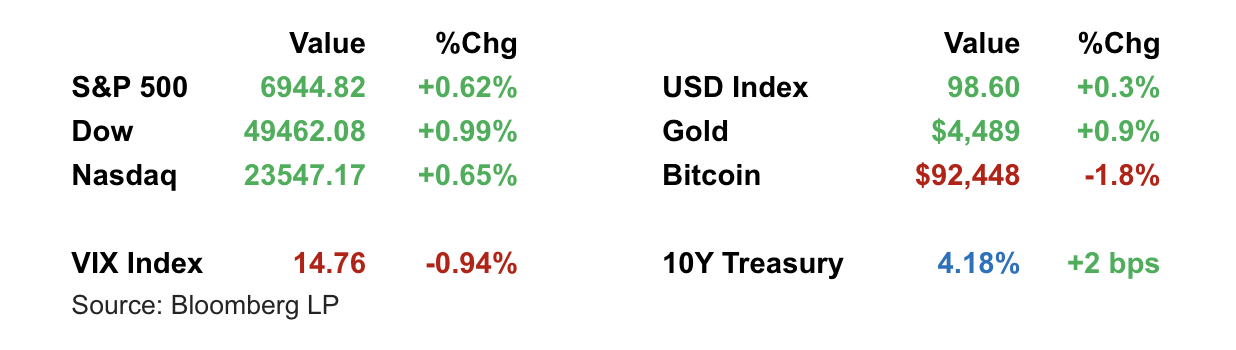

U.S. equities extended their rally Tuesday, with the S&P 500 closing at a new all-time high, buoyed by renewed enthusiasm for AI-related stocks and growing confidence in Fed rate cuts. The Nasdaq and Dow also advanced, with the Dow topping 49,000 for the first time. Markets shrugged off geopolitical uncertainty and some mixed earnings reactions, focusing instead on a weaker U.S. services PMI that bolstered dovish monetary policy expectations. The rally was broad-based, but especially strong in small-caps and data-storage names, while tech leadership showed some rotation.

Key Headlines & Market Movers:

- AI Momentum Powers Tech Sector but Leadership Rotates: AI remains a major tailwind, with chipmakers unveiling new products at CES. Nvidia and AMD both shared updates on next-gen data center chips, but their stocks slipped following the announcements, suggesting high expectations may have been priced in. Instead, investors rotated into data storage names like Sandisk, Western Digital, and Seagate, which surged double digits on optimism over growing demand for AI infrastructure.

Fed Rate Cut Bets Rise After Weak Services PMI: A softer-than-expected U.S. services PMI reinforced the narrative of slowing economic momentum and helped push up rate cut expectations. While Treasury yields remained stable, equity markets viewed the data as supportive of Fed easing, boosting appetite for risk assets. Markets are increasingly pricing in cuts starting mid-year, with upcoming labor and business activity data likely to shape near-term sentiment.

- Venezuela News Sparks Volatility in Energy: Markets largely brushed off geopolitical risk following the capture of Venezuela's Nicolás Maduro. Energy names spiked Monday but reversed Tuesday, with Chevron falling 4% and WTI crude giving back recent gains, down over 2%. The pullback reflects the complexity of reopening Venezuela’s oil industry, and profit-taking after Monday’s outsized moves.

Cash on the Sidelines, Seasonal Tailwinds in Play: Money market balances remain near record highs ($7.6T), offering potential fuel for further gains, especially with January’s historical tendency to see strong equity performance: the so-called “January Effect.” Citadel’s Scott Rubner noted that this liquidity backdrop could amplify early-year momentum, particularly in risk-on segments.

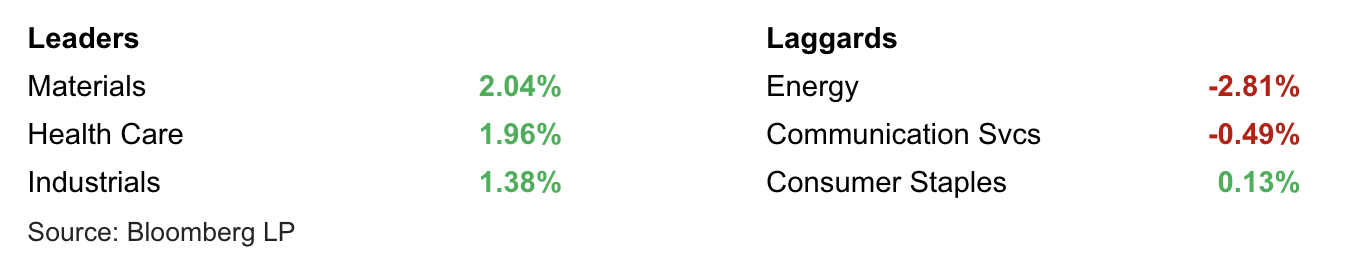

S&P 500 Sector Performance

Looking Ahead

Investors will be watching closely for upcoming labor market data and inflation prints to confirm or challenge the soft-landing narrative and guide Fed rate expectations. With equities pricing in a favorable policy pivot and continued AI growth, any surprises on inflation or wage growth could test the resilience of this rally. Meanwhile, watch for earnings from key sectors to validate or temper current valuation levels.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119