Markets Stumble as Jobs Data Sends Mixed Signals, Fed Cuts Remain in Play but Not Imminent

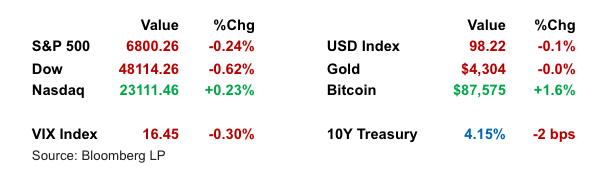

Markets closed mixed Tuesday after a noisy and inconclusive U.S. employment report kept investors guessing on the Fed's next move. While November payrolls rose more than expected, a higher unemployment rate and muted retail sales pointed to cooling economic momentum. Traders trimmed odds for a January rate cut, while longer-term easing expectations remained intact. Big tech helped the Nasdaq eke out a gain, but the S&P 500 and Dow slipped. Treasury yields fell slightly, oil plunged below $55, and investor focus now turns to December’s more reliable labor data.

Key Headlines & Market Movers:

- Jobs Report - Mixed Signals, No Urgency for Fed Action: November payrolls rose by 64,000, rebounding from October’s sharp drop, but the unemployment rate ticked up to 4.6%, the highest since 2021. The data was clouded by government shutdown impacts, making it difficult for markets or the Fed to draw clear conclusions. Most strategists agree: this report supports prior rate cuts but doesn’t strengthen the case for an early 2026 cuts. The January meeting remains a coin toss, with markets assigning a roughly 20-25% chance of a cut.

Retail and Business Data Show Flat Momentum: Retail sales in October were flat, disappointing modest expectations, and September business inventories rose more than anticipated. Together, these point to a slowing but not collapsing consumer backdrop. Analysts remain cautiously optimistic that resilient consumer spending and a stabilizing labor market could prevent a hard landing, but cracks are forming.

- Bond Market Choppy, But Rates Grind Lower: Treasuries held firm despite initial volatility, with the 10-year yield easing to 4.15%. Market participants appear content to hold current ranges until clearer signals arrive. Short-term expectations remain anchored to incoming inflation and jobs data, with the Fed seen as likely to pause in January and potentially resume cuts in Q2 if economic softness deepens.

Corporate Moves & AI Sentiment Shift: Corporate headlines were plentiful but mostly stock-specific. Tesla jumped to a record on driverless tech enthusiasm, while Broadcom and Oracle rebounded after recent AI-related selloffs. Visa's embrace of stablecoin settlements and Databricks’ $134B valuation underscored the continued momentum in digital assets and enterprise AI. Elsewhere, Pfizer warned of flat 2026 sales, and Kraft Heinz appointed a new CEO.

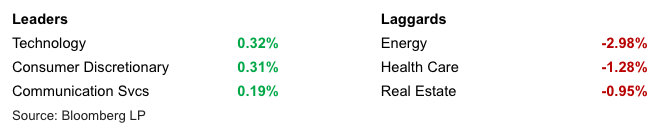

S&P 500 Sector Performance

Looking Ahead

With Fed policy now firmly in "wait and see" mode, the December jobs and inflation prints will carry outsized importance for shaping Q1 rate expectations. Markets appear to be in a holding pattern, and barring a major data surprise, the path forward likely favors selective positioning, income-generating assets, and quality over growth. Volatility may pick up in the final weeks of the year as investors reassess their outlooks ahead of what could be an eventful 2026 for rates, earnings, and the consumer.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119