Rates, Returns, and Risk: How to Put the Fed’s Latest Move in Proper Context

The Fed’s December decision to cut rates again is important, but it is only one of many forces that will shape long‑term investment outcomes. For individual investors, the real work is integrating this move into a thoughtful plan around rates, returns, and risk rather than reacting to a single meeting.

What the Fed Just Did

The Federal Reserve lowered the federal funds target range by 0.25 percentage point at its December 2025 meeting, to 3.50%–3.75%, marking the third cut this year and the lowest level since 2022. Officials signaled a more cautious, “wait‑and‑see” stance from here, with projections pointing to only gradual additional cuts over the next few years.

This shift reflects a balance between cooling inflation and concerns about a softening labor market, rather than an attempt to stimulate a deep recessionary downturn. Markets had widely anticipated the move, which means much of the near‑term impact on bond yields and equities may have been priced in ahead of the announcement.

Rates, Returns, and the Big Picture

Over long horizons, investor returns are driven more by earnings growth, starting valuations, and inflation trends than by any single policy move. Historical episodes show that rate cuts can coincide with either rallies or drawdowns in stocks depending on whether they reflect a gentle slowdown or a more serious economic shock.

Similarly, bond returns over time are linked to the path of yields, reinvestment rates, and credit fundamentals, not one FOMC press conference. Global developments—from growth in major economies to geopolitical risks—also shape the backdrop for U.S. assets and can amplify or mute the effect of Fed policy.

Rethinking Cash After Rate Cuts

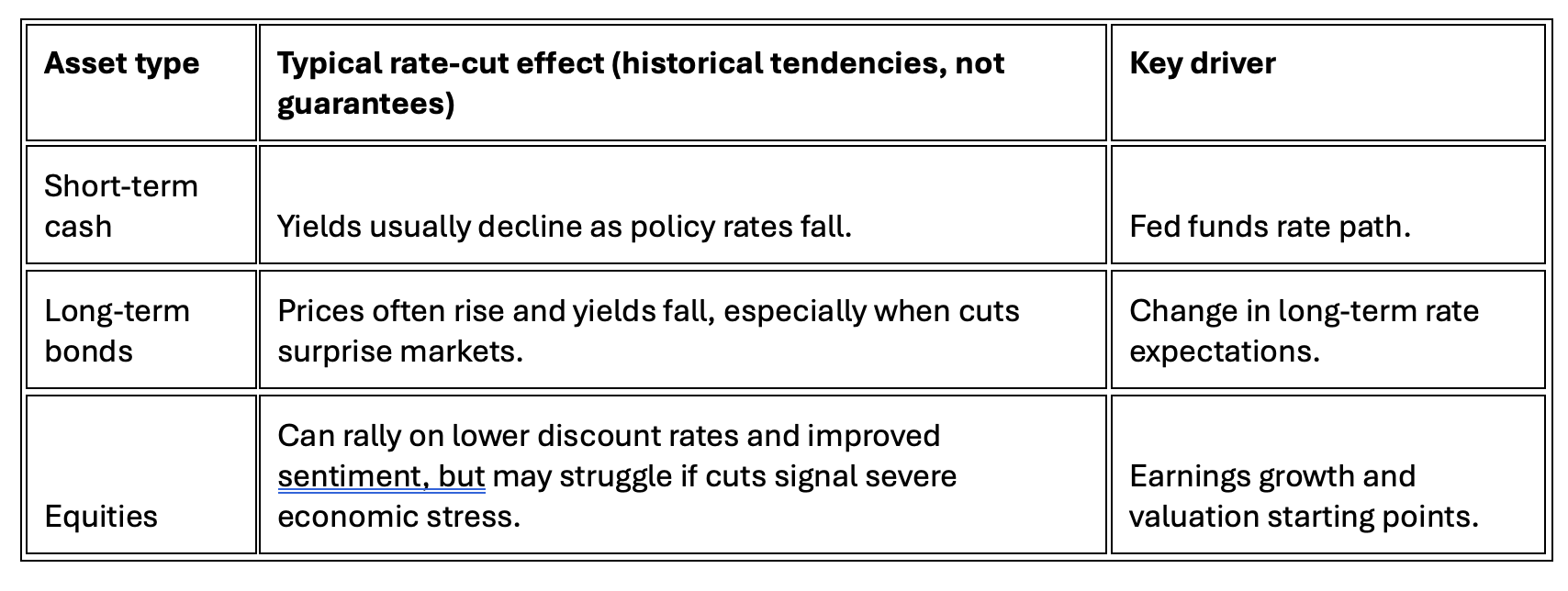

Short‑term cash vehicles and savings accounts tend to follow the fed funds rate relatively quickly, so repeated cuts can reduce the yield on idle cash. For investors holding sizeable balances beyond an emergency reserve, that means the opportunity cost of staying in cash may rise as real (after‑inflation) returns decline.

A practical response is to segment cash into:

- True emergency reserves, which remain in highly liquid, low‑volatility vehicles regardless of rate moves.

- Near‑term spending needs, which might still warrant conservative instruments but can be laddered to modestly improve yield.

- Long‑term capital, which may be better aligned with diversified stock and bond portfolios rather than excess cash awaiting a “perfect” entry point.

Bond Portfolios and Interest‑Rate Risk

Lower policy rates and shifting expectations for future cuts influence the entire yield curve, changing the trade‑off between income and interest‑rate risk. When long‑term yields fall, existing bonds with higher coupons often appreciate, but prospective returns from new purchases may be lower going forward.

Investors can respond by:

- Reviewing duration: ensuring the average maturity of bond holdings aligns with the need for stability and income, rather than just “chasing yield.”

- Diversifying across sectors and credit quality, balancing government, municipal, and corporate exposure instead of concentrating in one segment.

- Considering bond ladders or barbell strategies to manage reinvestment risk if rates move differently than expected.

How Assets Tend to React

Equities: Avoid “Green Light / Red Light” Thinking

Equity markets frequently move ahead of the Fed, reacting to expectations for growth and inflation rather than waiting for formal decisions. In many past cycles, some of the strongest stock returns occurred before or in the early stages of a rate‑cutting campaign as investors anticipated easier conditions.

This makes it risky to treat any single Fed move as an all‑clear or stop sign for stock exposure. A more durable approach is to anchor equity allocations to time horizon, risk tolerance, and diversification across sectors and regions, adjusting gradually as fundamentals evolve rather than in response to headlines.

Turning Information into a Plan

The most important task for individual investors is to keep Federal Reserve actions in proportion to the rest of the financial picture. That means using policy shifts as a prompt to revisit allocations—cash, bonds, and equities—in light of goals, timeframes, and capacity to withstand volatility, not as triggers for all‑or‑nothing market timing.

A coherent long‑range plan typically:

- Starts with clear objectives (retirement, education, legacy) and required return targets.

- Aligns asset mix and risk level to those objectives while acknowledging that rates, inflation, and markets will change over time.

- Builds in rules for periodic rebalancing and review so that each Fed meeting is an input into an ongoing process, not a make‑or‑break event.

Disclosure: This material is for informational purposes only and does not constitute investment, tax, or legal advice. Past performance is not indicative of future results. Investment decisions should be made based on an investor’s individual objectives, risk tolerance, and financial circumstances, preferably in consultation with a qualified financial professional. All market and economic data cited are believed to be from reliable sources but are not guaranteed for accuracy or completeness. Investing involves risk, including possible loss of principal.

Sources:

Federal Reserve FOMC statement, December 2025: https://www.federalreserve.gov/newsevents/pressreleases/monetary20251210a.htm

FOMC projections, December 2025: https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20251210.htm

Trading Economics – U.S. Fed funds rate: https://tradingeconomics.com/united-states/interest-rate

FRED – Effective fed funds rate: https://fred.stlouisfed.org/series/FEDFUNDS

Nuveen – FOMC meeting commentary, December 2025: https://www.nuveen.com/en-us/insights/investment-outlook/fed-update

Fidelity – Fed meeting December 2025: https://www.fidelity.com/learning-center/trading-investing/the-fed-meeting

Investopedia – How interest rates influence U.S. stocks and bonds: https://www.investopedia.com/articles/stocks/09/how-interest-rates-affect-markets.asp

Central Trust – Implications of Fed rate cuts: https://centraltrust.net/fixed-income-investments-blog/fed-dot-plot

Bankrate – Federal funds rate history: https://www.bankrate.com/banking/federal-reserve/history-of-federal-funds-rate/

Forbes Advisor – Federal funds rate history: https://www.forbes.com/advisor/investing/fed-funds-rate-history/

ADM – FOMC reduces interest rates at December 2025 meeting: https://americandeposits.com/insights/fomc-reduces-interest-rates-december-2025/

USA Today – Consumer impacts of Fed rate cut: https://www.usatoday.com/story/money/2025/12/16/fed-rate-cut-mortgage-rates-credit-cards/87792292007/

New York Life Investments – What history reveals about rate cuts (PDF): https://www.newyorklifeinvestments.com/assets/documents/perspectives/infographic-what-history-reveals-about-interest-rate-cuts.pdf

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119