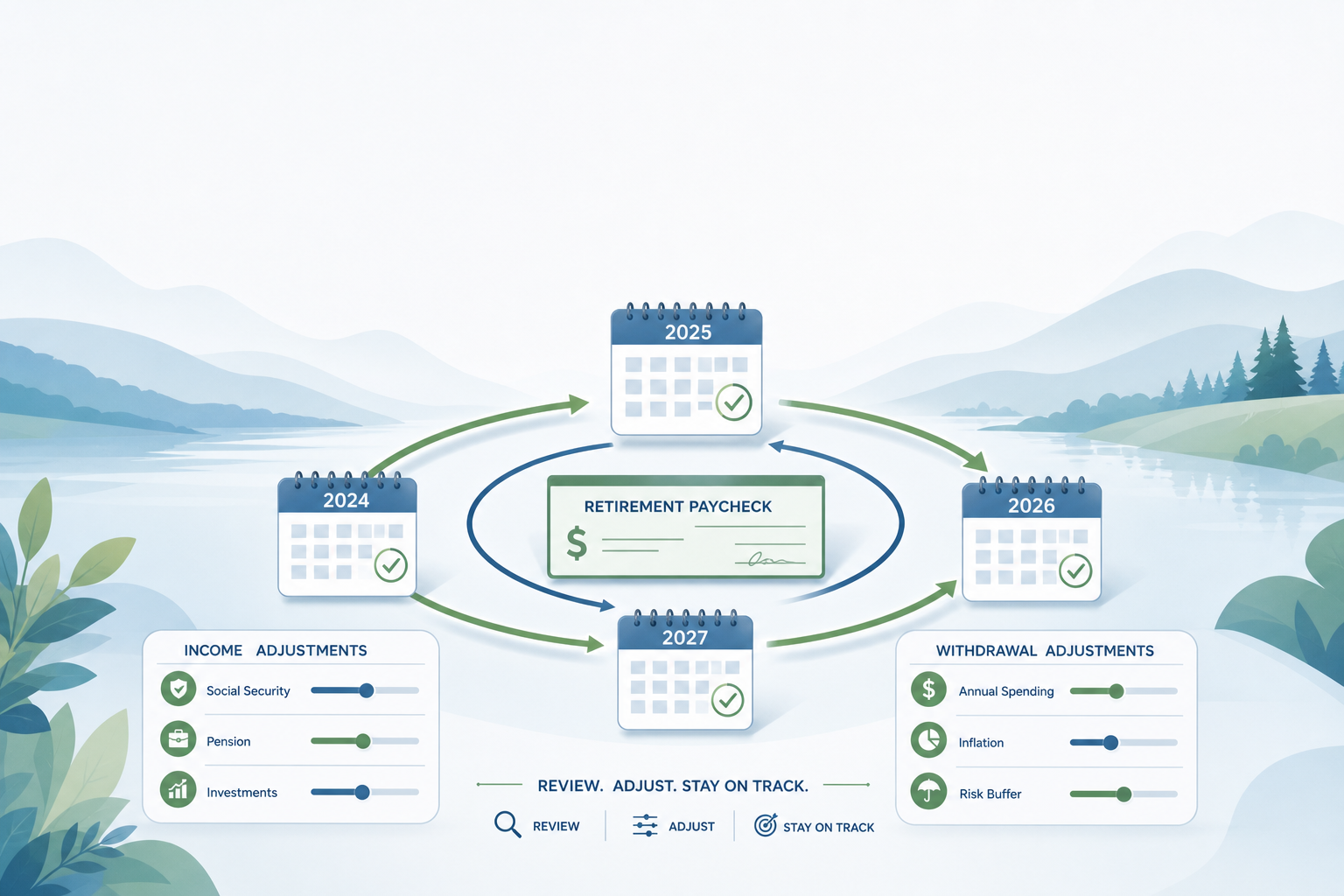

At Duncan Williams Asset Management, we understand that life rarely stays the same, especially in retirement. That’s why we encourage you to take a fresh look at your “retirement paycheck” every year—particularly if your 401(k) is a main source of income. This annual review helps you adjust your income to fit your current needs, while protecting your savings for the future.

Why an annual “retirement paycheck” review matters

Retirement is an ongoing adventure. The markets rise and fall, prices fluctuate, and your needs and goals can shift over time. The plan that worked last year might not be the best fit this year, especially if you’ve experienced changes in the market or in your personal life.

We see the annual review as your personal “raise and reality check.” Are you still on track for the lifestyle you want? Is your current income sustainable in light of today’s markets and your circumstances? For many, meeting with a Duncan Williams Asset Management advisor each year is how they stay confident and in control.

Connecting income to your 401(k) withdrawals

Most “retirement paychecks” are built from several components: traditional 401(k)s and IRAs, taxable investment accounts, Social Security, and sometimes pensions or annuities. Because traditional 401(k) withdrawals are generally taxed as ordinary income, each dollar you take out affects both your cash flow and your tax picture.

Our conversations often start with a simple question: “After Social Security and any other steady income, what do you actually need from your portfolio this year?” With that answer, we build a tax-smart withdrawal plan, helping you decide how much to draw from each type of account—401(k), taxable, or Roth.

Adapting to markets, inflation, and life changes

Research increasingly shows that flexible withdrawal strategies—where you adjust your spending in response to the markets—work better than rigid rules. For instance, you might scale back spending after a market downturn, or reward yourself with a “raise” in good years. This approach helps you start with more income, while still managing long-term risk.

Inflation is another reason for an annual review. If costs rise quickly, your money may not stretch as far unless you make adjustments. Simply increasing withdrawals year after year can be risky, so reviewing your spending lets you boost essentials when needed and cut back elsewhere if necessary.

Keeping your withdrawal rate in a healthy range

Rules of thumb—like the “4% rule”—can help you get started, but only a plan built around your specific needs will give you confidence. Each year, we check whether your withdrawal rate fits your evolving goals and the market climate.

When markets do well, you might deserve a small “raise”—especially if your essentials are covered elsewhere. If times are tough, holding steady or trimming extras can make your nest egg last longer.

Coordinating taxes and required minimum distributions (RMDs)

Withdrawals from 401(k)s and IRAs are taxed as regular income, so timing and order matter for your taxes. Many people use taxable accounts first, then tax-deferred, and save Roths for later or as an inheritance. But the right path depends on your tax bracket, required distributions, and other income.

During your annual review, we revisit questions such as:

- Should we take a bit more from the 401(k) this year to make use of lower tax brackets before RMDs begin?

- Does a partial Roth conversion make sense in a relatively low‑income year?

- How will this year’s withdrawals interact with Medicare premiums, Social Security taxation, and other thresholds?

Annual reviews help you stay ahead of tax surprises and keep your withdrawal plan in sync with your life.

How Duncan Williams Asset Management can help

For most retirees, the hardest part isn’t the calculations—it’s managing trade-offs, emotions, and uncertainty every year. At Duncan Williams Asset Management, we help you translate your lifestyle into a practical income plan, stress-test it under real-life scenarios, and make adjustments as your situation evolves.

Think of your “retirement paycheck” as a living plan you can update as life changes—not a strict rule. An annual review makes it easier to adapt and stay focused on your long-term goals. If you want to revisit your withdrawal strategy or start planning before you retire, our team is ready to help you run the numbers.

Sources

Sources: Internal Revenue Service guidance and publications related to retirement income and required minimum distributions; independent research on safe and flexible retirement withdrawal rates; and professional articles on tax‑efficient retirement income planning.

Disclosure

Disclosure: This material is provided for informational and educational purposes only and should not be construed as specific tax, legal, or investment advice, nor as a recommendation to buy, sell, or hold any security. Tax laws and regulations are subject to change, and their application may vary based on individual circumstances. Before making any decisions regarding retirement income strategies or 401(k) withdrawals, you should consult with a qualified tax professional and/or financial advisor. All investing involves risk, including the possible loss of principal, and there is no guarantee that any strategy will achieve its intended results or ensure success in any given market environment.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119