Resilient Investing Before Fed Meetings: How to Build a Stress Tested Financial Plan

A stress‑tested financial plan helps long‑term investors stay focused on what they can control instead of guessing the exact outcome of the next Federal Reserve meeting. By running through a few realistic interest‑rate scenarios and adjusting cash, debt, and portfolio risk where needed, you can approach events like the December 10 announcement with more clarity and less anxiety.

Why stress testing matters

Stress testing is a technique that evaluates how a portfolio or financial plan might behave under adverse or unexpected conditions, such as sharp rate moves or market volatility. Large institutions are required to perform these kinds of exercises to ensure their capital and liquidity can withstand severe but plausible shocks, and individual investors can borrow the same mindset to strengthen their own plans.

Instead of concentrating on whether the Fed will hike, cut, or hold rates at a single meeting, stress testing reframes the question as, “Does my plan still work across a range of paths for growth, inflation, and interest rates?” This shift from prediction to preparation helps reduce the temptation to make emotional, short‑term bets around headlines.

Build simple interest‑rate scenarios

A practical way to stress test is to sketch three basic interest‑rate paths over the next few years: rates stay higher for longer, rates fall faster than expected, and rates move sideways in a choppy pattern. Each path can be informed by how markets are currently pricing the Fed’s future moves and by historical episodes when policy changed more slowly or more quickly than anticipated.

For a “higher for longer” scenario, assume that policy rates remain elevated or decline only gradually, which tends to pressure long‑duration bonds, rate‑sensitive sectors like real estate, and highly leveraged borrowers. For a “faster decline” scenario, imagine that growth slows and the Fed cuts more aggressively, which may support bond prices but could also signal economic softness that weighs on risk assets such as equities and high‑yield credit. A “choppy path” scenario considers repeated small hikes and cuts that keep uncertainty high and can increase day‑to‑day volatility in both bond and stock markets.

Examine cash, debt, and investments

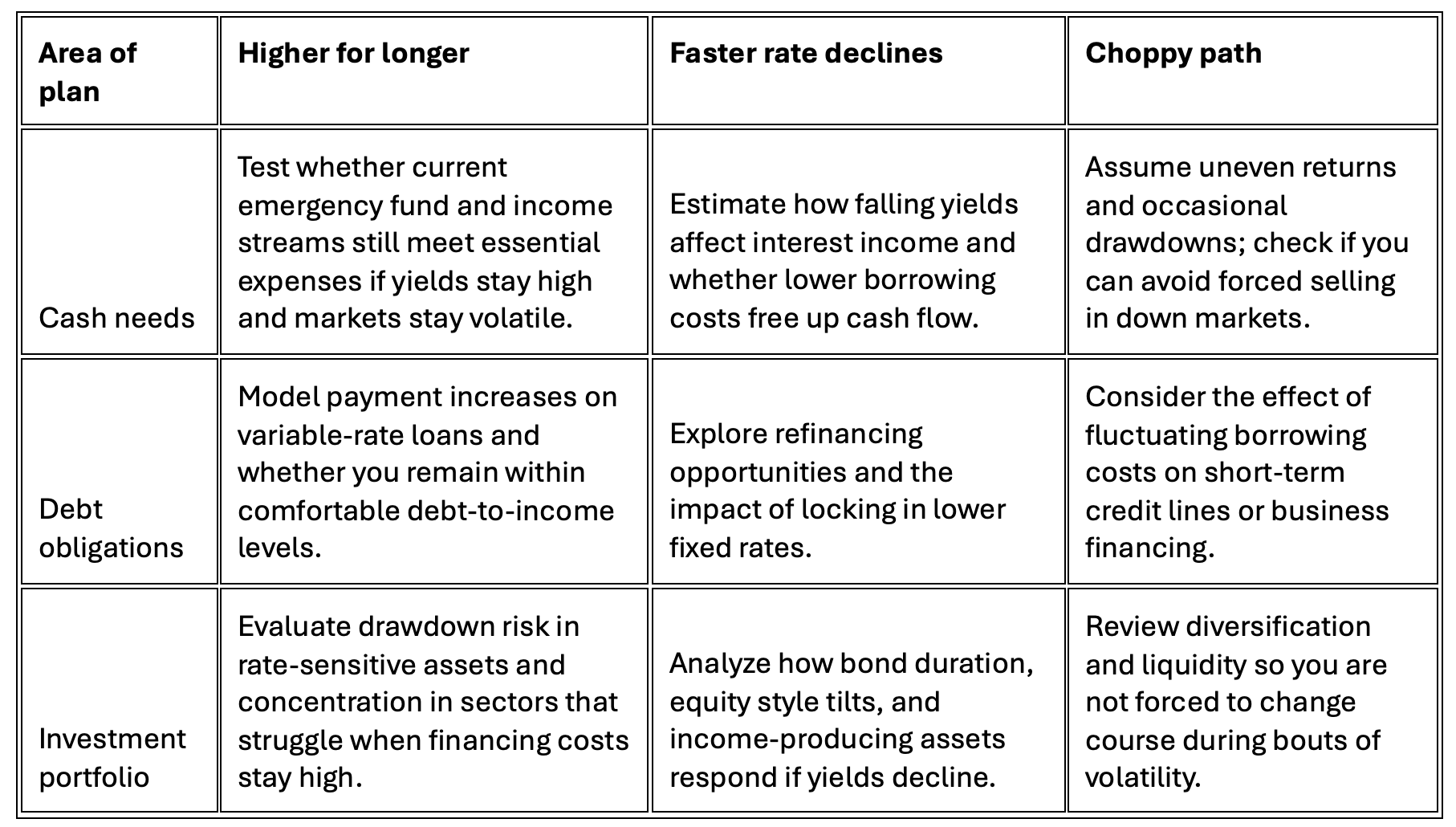

Once scenarios are defined, the next step is to map out how your household cash flows would respond in each environment. Consider questions such as whether your emergency savings and steady income sources (for example, salary, pensions, or laddered CDs) would still cover essential expenses if borrowing costs rose or investment income fell.

Debt obligations deserve special attention because changing interest rates directly influence adjustable‑rate mortgages, lines of credit, and business loans. In a higher‑rate scenario, payments on variable‑rate debt could increase, compressing your margin for error, while in a lower‑rate scenario, you might have opportunities to refinance or accelerate repayment. On the investment side, assess how sensitive your holdings are to interest‑rate moves—long‑duration bonds, certain growth stocks, real estate investment trusts, and private assets can all respond differently depending on the direction and speed of rate changes.

A simple way to organize this exercise is to compare how your plan behaves across scenarios:

Turn insights into practical adjustments

If this exercise exposes weaknesses, the aim is not to guess the Fed’s next move but to improve resilience in ways that make sense across multiple paths. Common responses include gradually building a larger cash buffer to cover several months of essential spending, trimming exposure to particularly leveraged or illiquid positions, and modestly rebalancing toward a mix of assets that behave differently under changing rate conditions.

Some investors may choose to shorten bond duration, diversify sources of income, or match the timing of major goals—such as home purchases or business expansions—with more stable funding sources. Others may focus on simplifying portfolios and establishing rules for when, or if, they will make allocation changes around major policy events, reducing the risk of emotional decision‑making on meeting days.

Staying calm through Fed meetings

A plan that has been rigorously stress tested tends to be easier to stick with during turbulent periods because you have already explored what could go wrong and how you would respond. Instead of reacting to every headline about the December 10 decision or future meetings, you can view each announcement as one new data point within a broader, long‑term framework.

Over time, this approach encourages discipline: savings, debt management, and diversified investing become ongoing processes rather than one‑off reactions to central bank news. By focusing on preparation instead of prediction, long‑term investors increase the odds that their financial plans will remain on track—whatever path interest rates ultimately follow.

Disclosure

This material is provided for informational and educational purposes only and should not be construed as individualized investment, tax, or legal advice. Investing involves risk, including the possible loss of principal, and no strategy, including stress testing, can guarantee performance or protect against all market or interest‑rate movements. Past performance is not indicative of future results, and any references to Federal Reserve policy decisions are illustrative and subject to change without notice. You should evaluate your own financial situation and consult with a qualified financial professional before making any investment or planning decisions.

Sources

Federal Reserve Board – Monetary Policy: https://www.federalreserve.gov/monetarypolicy.htm

Federal Reserve Board – FOMC Calendar: https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

Investopedia – Stress Testing: https://www.investopedia.com/terms/s/stresstesting.asp

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119