Markets rebounded sharply on Thursday as investors welcomed an interim US-Iran peace deal that reopened the Strait of Hormuz and eased concerns about another energy-driven inflation shock. That shift helped stocks recover from the prior session’s Fed-related selloff, while longer-dated Treasury yields moved lower as traders reassessed the odds of additional rate hikes. The tone was broadly risk-on, led by technology and especially semiconductors, even as some pockets of the market remained volatile.

Key Headlines & Market Movers:

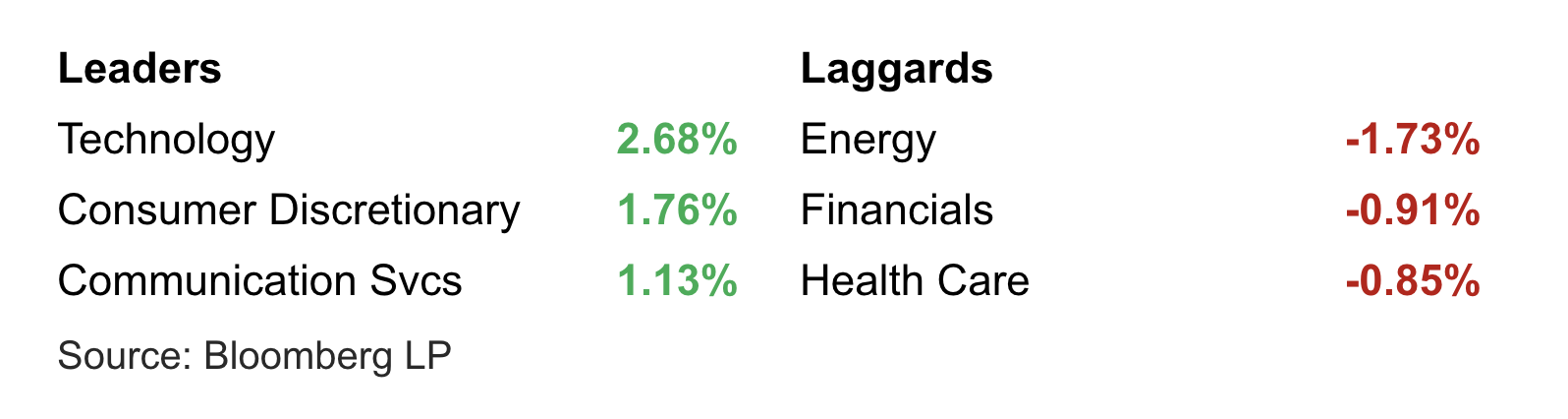

- US-Iran agreement eases inflation pressure: The main macro driver was the announced de-escalation between the US and Iran, which reduced fears of a prolonged disruption in global energy flows. With shipping beginning to return through the Strait of Hormuz, investors saw less risk of another spike in oil prices feeding through to headline inflation. That helped support both equities and bonds, as lower expected energy pressure can make it easier for central banks to stay patient.

Semiconductor stocks power the market higher: Chipmakers led the advance, with the sector rallying to fresh highs after President Trump said Intel would work with Apple to design and manufacture semiconductors in the US. Even without formal company confirmation in the text provided, the market clearly treated the statement as a meaningful positive for domestic chip production and AI-related spending. The move reinforced how concentrated leadership remains in large-cap tech and semiconductor names.

Fed tension remains, but lower yields steady sentiment: The rebound came just one day after markets sold off on concerns that the Federal Reserve may still need to tighten policy further if inflation stays sticky. Thursday’s decline in the 10-year Treasury yield suggested some of that concern faded as energy risks moderated, though the policy backdrop is still not fully settled. Corporate news also added to the day’s trading, with SpaceX shares continuing to slide after its IPO volatility while Accenture warned on revenue, highlighting that not all growth stories are being rewarded equally.

S&P 500 Sector Performance

Looking Ahead

The next key question is whether the Iran ceasefire holds and whether calmer oil markets persist long enough to influence incoming inflation data and reshape rate expectations. If energy prices remain contained, that could reduce pressure on the Fed and help preserve the current equity rebound, particularly in rate-sensitive growth sectors. Investors will also be watching whether semiconductor leadership broadens into a more durable market advance or remains a narrow theme in an otherwise selective tape.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119