A tax refund can feel like a bonus, but it’s really just money you paid in taxes that you didn’t need to. Since it’s your own money coming back to you, it’s worth thinking carefully about how you use it.

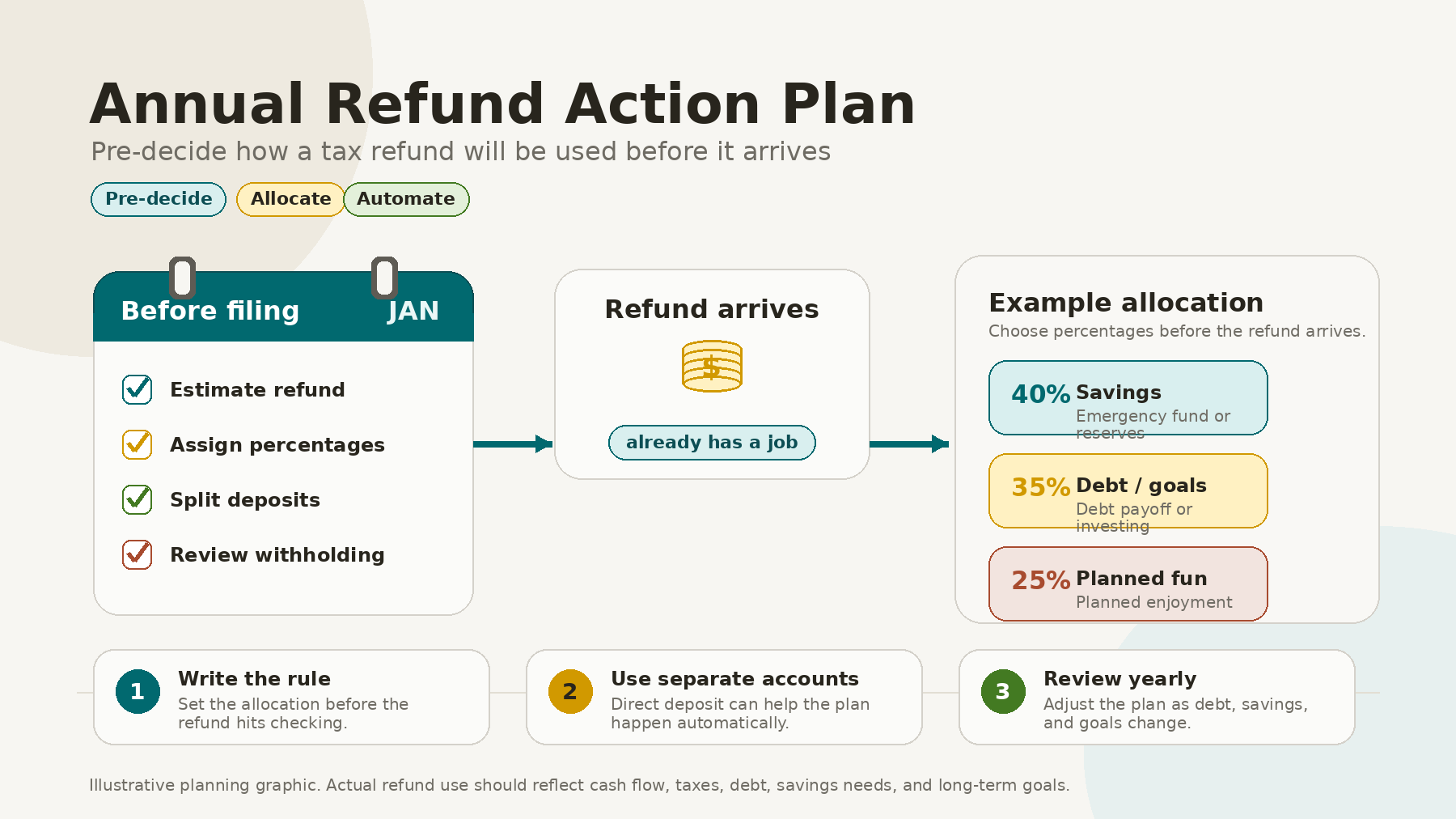

One of the smartest ways to use your refund is to decide in advance what you’ll do with it. Creating a simple “Refund Action Plan” each year can help you avoid impulsive spending and turn tax season into a possibility to advance your financial goals.

The point isn’t to eliminate flexibility—it’s to make sure your refund fits into your bigger financial picture before it lands in your account.

Why Planning Beforehand Matters

Refunds often arrive as a lump sum, which can make them psychologically different from regular income. A paycheck is usually assigned to bills, savings, and monthly spending before it arrives. A refund, by contrast, may feel separate from the household budget.

That feeling sometimes leads to sudden decisions—a vacation upgrade, a big purchase, or several small splurges that quickly use up the whole refund. None of these choices are automatically bad, but it’s important to pause and ask how that money could help your long-term goals first.

A Refund Action Plan creates a simple rule in advance. For example:

“Whenever we receive a refund, 50% goes to savings, 25% goes to debt reduction, and 25% can be used for family spending.”

Deciding in advance takes the pressure off when the money actually arrives.

Start With the Most Important Question

Before deciding how to allocate a refund, ask:

“What would strengthen our financial position the most this year?”

For some households, the answer may be emergency savings. For others, it may be paying down high-rate debt, increasing retirement contributions, funding an IRA, adding to an HSA, adding to a 529 plan, or building cash for a home project.

The Consumer Financial Protection Bureau suggests estimating your refund, identifying important bills, planning for special purchases, figuring out what’s left, and deciding how much to save—before the money shows up. Here’s a helpful resource: https://www.consumerfinance.gov/about-us/blog/make-a-tax-refund-savings-plan/.

This solution helps separate your needs, goals, and wants before the refund arrives, so you can make clear-headed decisions.

A Simple Refund Action Plan Framework

A practical plan can categorize the refund. The percentages can vary, but the structure must be decided in advance.

1. Rebuild or strengthen cash reserves

If emergency savings are below target, consider assigning a portion of the refund to cash. This can help reduce future reliance on credit cards or short-term borrowing.

A refund can be especially useful for households that had unanticipated expenses during the prior year and want to rebuild liquidity.

2. Pay down high-rate debt

Credit cards and other high-rate debt can create a drag on long-term progress. Using part of a refund to reduce those balances may improve monthly cash flow and lower total interest costs.

Investors should compare the interest rate on debt with the expected long-term benefit of investing. In many cases, eliminating high-rate debt should take priority over adding to taxable investment accounts.

3. Add to retirement savings

A refund can help investors increase long-term investments. Depending on eligibility and timing, that may include an IRA, a Roth IRA, a workplace retirement plan contribution strategy, or a taxable investment account.

A refund itself cannot always be deposited directly into every type of retirement account in the same way payroll contributions work, so investors should work with their tax professional, custodian, or plan administrator before acting.

4. Fund health care or education goals

For eligible individuals, an HSA can be an effective way to cover qualified medical expenses and plan for long-term health care. A refund may also help fund education goals through a 529 plan or other savings vehicle.

The right choice depends on the household’s tax situation, account eligibility, expected expenses, and time horizon.

5. Reserve some for enjoyment

A good plan does not have to direct every dollar toward a serious goal. In fact, allowing a planned spending portion may make the overall plan easier to follow.

For example, you might decide ahead of time that 10% to 20% of any refund can go toward travel, a home project, or family fun. The important thing is to decide in advance, not on the fly.

Consider Splitting the Refund Automatically

One practical way to follow the plan is to send the refund to multiple destinations.

The IRS says taxpayers can use Form 8888 to split a federal tax refund among two or three accounts, either electronically through tax software or on paper. https://www.irs.gov/refunds/frequently-asked-questions-about-splitting-federal-income-tax-refunds

The IRS also notes that taxpayers can direct deposit a refund into one, two, or three accounts, and that direct deposit can be faster than receiving a paper check: https://www.irs.gov/refunds/get-your-refund-faster-tell-irs-to-direct-deposit-your-refund-to-one-two-or-three-accounts.

This is helpful because it makes the plan automatic. If some of your refund goes straight into savings, you’re less likely to spend it impulsively.

Example: A Pre-Decided Allocation

Assume a household expects a $4,000 refund. Before filing, they decide on the following plan:

40% to emergency savings: $1,600

25% to credit card or personal debt reduction: $1,000

20% to an IRA, HSA, 529 plan, or taxable investment account: $800

15% to planned family spending: $600

This plan gives every dollar a purpose. It also lets you enjoy some of the money while still using most of it to move your finances forward.

The exact percentages don’t matter as much as having a plan and sticking to it.

Review Withholding Too

A large refund may feel satisfying, but it may also mean too much tax was withheld during the year. Some investors prefer a larger refund because it acts like forced savings. Others would rather adjust withholding and increase monthly cash flow.

The IRS Tax Withholding Estimator is designed to help taxpayers see how withholding affects their refund, paycheck, or amount owed, and it can help generate a pre-filled Form W-4 or Form W-4P if alterations are necessary: https://www.irs.gov/individuals/tax-withholding-estimator.

You don’t need to aim for a refund of zero—the important thing is to be intentional. If you prefer to use tax withholding as a way to save, that’s fine—as long as it’s a choice, not just something that happens by accident.

Make It an Annual Habit

A Refund Action Plan works best when it becomes part of the yearly financial calendar. Consider reviewing it each January or February, before filing a tax return.

A simple annual checklist might include:

Estimate the likely refund or amount owed.

Review emergency savings.

Review high-rate debt.

Identify retirement, health care, education, or investment goals.

Decide what percentage can be spent guilt-free.

Choose accounts for direct deposit.

Confirm routing and account information before filing.

Revisit withholding after the return is filed.

This whole process can be simple. A one-page plan is often all you need.

The Bottom Line

A tax refund can vanish fast without a plan. By deciding ahead of time how you’ll use it, you can avoid impulsive spending and make sure your refund helps you reach your financial goals.

The best Refund Action Plan is realistic, flexible, and written down before your refund arrives. It should reflect your current needs and priorities—like cash savings, paying down debt, retirement, education, health care, or simply some planned fun.

Tax season is already a time to review your finances. With a little planning, it can also be a great opportunity to set yourself up for a stronger year ahead.

Sources

IRS, “Tell IRS to direct deposit your refund to one, two, or three accounts”

https://www.irs.gov/refunds/get-your-refund-faster-tell-irs-to-direct-deposit-your-refund-to-one-two-or-three-accounts

IRS, “Frequently asked questions about splitting federal income tax refunds”

https://www.irs.gov/refunds/frequently-asked-questions-about-splitting-federal-income-tax-refunds

IRS, “Tax Withholding Estimator”

https://www.irs.gov/individuals/tax-withholding-estimator

Consumer Financial Protection Bureau, “Make a plan to save some of your tax refund”

https://www.consumerfinance.gov/about-us/blog/make-a-tax-refund-savings-plan/

Consumer Financial Protection Bureau, “Five ways to keep more of your tax refund”

https://www.consumerfinance.gov/about-us/blog/five-ways-to-keep-more-of-your-tax-refund/

Disclosure

This material is for informational and educational purposes only and should not be considered personalized investment, tax, legal, or financial planning advice. Tax laws, IRS rules, account eligibility requirements, contribution limits, and filing procedures may change. Any examples are hypothetical and are not recommendations for any specific individual or household. Investors should consult their financial advisor, tax professional, or legal advisor before making decisions about tax refunds, withholding, debt repayment, retirement contributions, investment accounts, or other financial planning strategies. Investing involves risk, including the possible loss of principal, and no strategy can guarantee a profit or protect against loss.

Recent Articles

%20Investment%20Menu.png)

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119