A 401(k) plan is a valuable benefit for your team, but it also comes with ongoing responsibilities for you as a business owner and plan sponsor. Mid‑year is a practical time to pause and run a structured self-check on the plan, while there’s still time in the calendar year to correct issues and refine processes. The IRS 401(k) Plan Checklist and related resources offer a high‑level framework you can use as a self‑audit guide.

Why a mid‑year self‑audit matters

Running a mid-year self-audit can help you catch small operational missteps—like eligibility timing or deposit delays—before they become costly problems. Early detection may reduce the risk of expensive corrections, penalties, or participant complaints later on. It also demonstrates proactive fiduciary care and keeps your internal team aligned on how the plan is supposed to operate day-to-day, so you can address issues before year-end.

Understanding the IRS 401(k Checklist

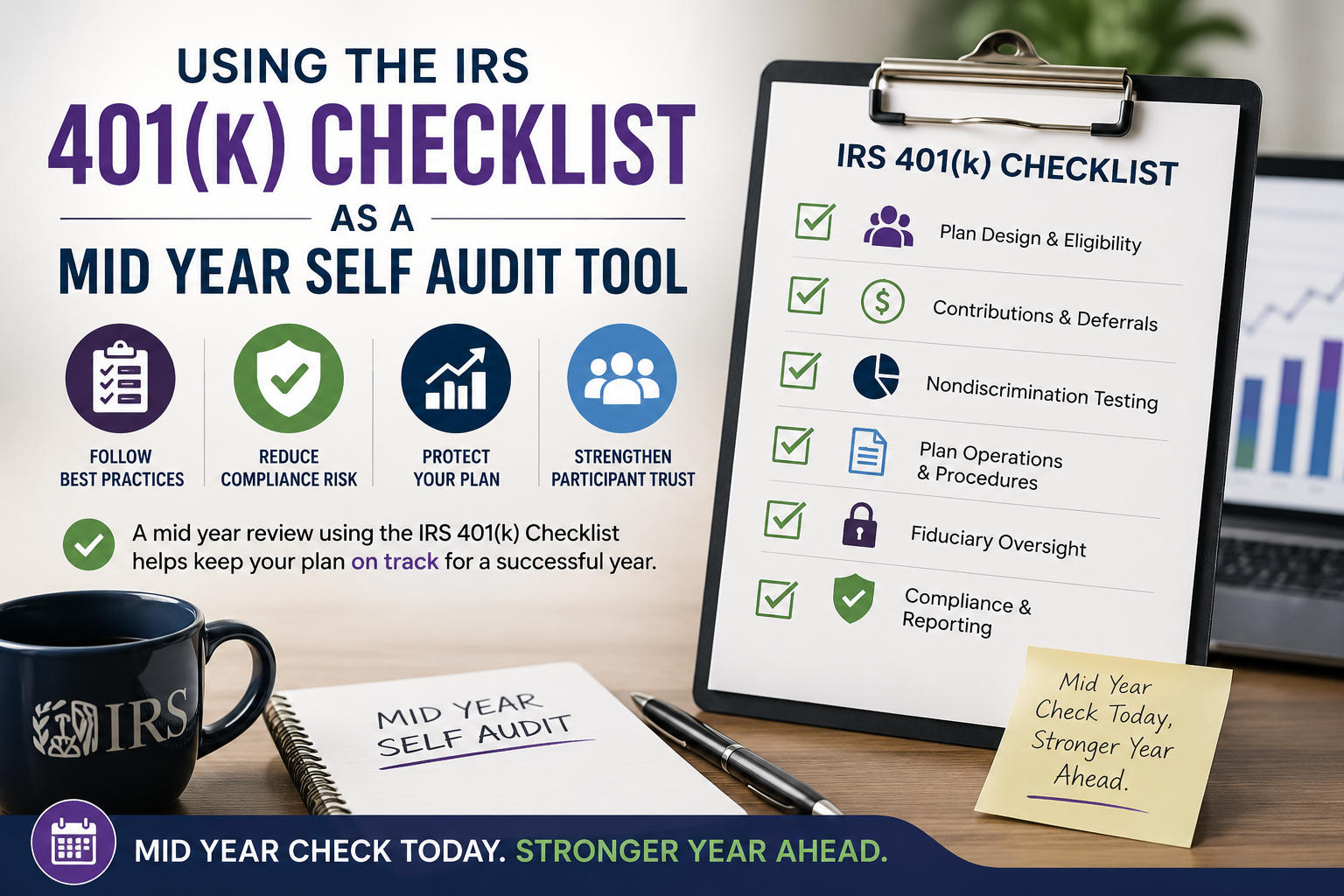

The IRS 401(k) Plan Checklist is designed as a practical tool for plan sponsors to review key operational areas, including eligibility, contributions, distributions, plan limits, and documentation. With those areas in mind, each item on the checklist is framed as a yes/no question, prompting you to confirm whether your plan is operating in line with the rules and the plan document.

Common checklist focus areas include:

- Eligibility and entry dates: Are you applying the eligibility rules and entry dates exactly as described in your plan document?

- Contribution timing and limits: Are employee deferrals being deposited as soon as reasonably possible, and are contributions staying within annual limits?

- Employer contributions: Are matching and profit‑sharing contributions calculated and allocated according to the formula in the plan document?

- Distributions and loans: Are hardship withdrawals and loans handled in line with written policies and applicable regulations?

The checklist also points you to additional IRS publications and the “Fix-It Guide,” which outline common errors and general approaches for correcting them. From there, you can use those resources to better understand potential issues and next steps.

How to use the checklist mid‑year

A practical mid‑year process might look like this:

- Gather key documents. Collect your plan document, adoption agreement, summary plan description, recent trust or recordkeeping reports, and payroll records related to contributions.

- Walk through the checklist systematically. As you compare the IRS questions with your actual processes, use the checklist as a prompt to review what your document says and what your internal processes actually do—for example, how eligibility is determined, how quickly deferrals move from payroll to the plan, and how employer contributions are calculated.

- Note any “no” or “not sure” answers. These are areas where you may want to dig deeper, review additional IRS guidance, or talk with your recordkeeper, third‑party administrator, or other professional advisors.

- Document observations and next steps. Keep a simple written record of your review: what you checked, what you found, and what follow‑up actions you plan to take. This documentation can be helpful if questions arise later or if you participate in a formal review with your advisors.

The goal is not to perform a formal compliance opinion, but to create a structured, repeatable mid-year habit of checking whether the plan is operating as intended. Use the checklist results to decide what needs follow-up and when you will take it up with your advisors.

Coordinating with professionals

If the checklist raises questions, using it as a conversation starter with your professional team can be helpful. Many plan sponsors review the results with their recordkeeper, third-party administrator, CPA, or legal counsel to discuss whether potential issues require attention. From there, IRS resources may describe general correction paths for common errors, but specific steps depend on your plan, your facts, and guidance from qualified professionals.

Building an annual “checkup” rhythm

Over time, integrating the IRS 401(k) Checklist into your annual rhythm—mid-year and perhaps again near year-end—can help make plan oversight more manageable. In that way, a simple calendar reminder to run a checklist review, document findings, and schedule any needed follow-up meetings can keep the plan on track without overwhelming your schedule.

Sources & further reading

- Internal Revenue Service – 401(k) Plan Checklist and Fix‑It Guide: https://www.irs.gov/retirement-plans/401k-plan-checklistirs+1

- Internal Revenue Service – IRC 401(k) Plans: Additional Resources: https://www.irs.gov/retirement-plans/irc-401k-plans-additional-resourcesirs

- Internal Revenue Service – Retirement Plans for Plan Sponsors: https://www.irs.gov/retirement-plans/plan-sponsorirs

- U.S. Department of Labor, Employee Benefits Security Administration – Employers and Advisers: https://www.dol.gov/agencies/ebsa/employers-and-advisersdol

Disclosure

This material is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. It is not intended to be, and should not be construed as, a recommendation to adopt any specific plan design, investment, or strategy. The information here is general in nature and may not reflect the current rules or guidance applicable to your specific situation. Business owners and plan sponsors should consult with their own qualified tax advisors, legal counsel, and retirement plan professionals before making any decisions related to their 401(k) or other retirement plans.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119