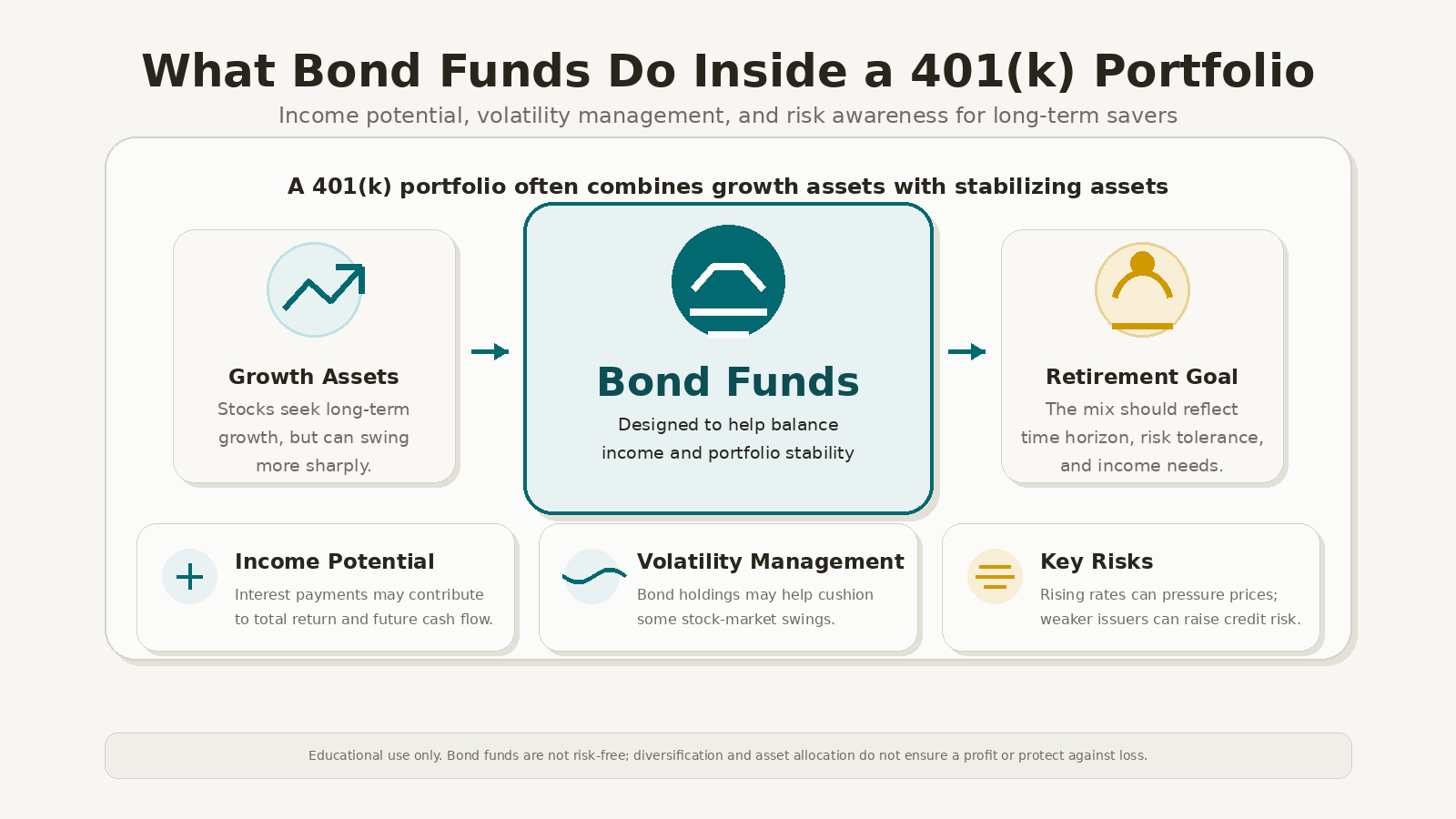

Bond funds are often called the “safer” side of a 401(k), but that label can be misleading. They don’t eliminate risk or guarantee income. Within a retirement portfolio, bond funds typically provide income, diversify beyond stocks, and help smooth market swings. Nevertheless, they have their own risks, which investors should understand before deciding how much to invest.

A 401(k) is a retirement plan offered by employers that lets employees choose how to invest their savings, often including mutual funds and target date funds (Investor.gov). Because you have control over where your money goes within the available options (U.S. Department of Labor), it’s important to understand what role bond funds can play in your 401(k).

Bond Funds Are Pooled Fixed-Income Investments

A bond is essentially a loan: you lend money to a government, city, or company, and in return, they promise to pay you interest—which is a regular payment for the use of your money—and eventually pay back your original investment (Investor.gov). Bond funds bundle lots of these loans together into one mutual fund or exchange-traded fund (ETF), which are investment funds traded on stock exchanges; so, you’re investing in a mix of many bonds instead of just one (Vanguard). Some funds may hold hundreds or even thousands of bonds at once (Vanguard).

This pooled approach is common in 401(k) plans, since most people invest through their plan’s chosen funds instead of individual bonds. Bond funds may focus on U.S. government, corporate, mortgage-backed securities, international bonds, or any mix (Vanguard; Fidelity). Some target short-term or long-term bonds, or higher-yield (riskier) bonds. Risks and rewards depend on the mix, bond duration, and creditworthiness of issuers (Vanguard).

The Income Role

A big reason bond funds are included in retirement portfolios is income. Bonds are designed to pay interest regularly, providing a steady stream of income before they mature (Investor.gov). Bond mutual funds and ETFs let your savings earn this interest, which can grow over time and help cover expenses (Vanguard).

In a 401(k), you don’t usually get that income as a check while you’re saving for retirement. Instead, it’s added to your account’s growth and may be reinvested automatically, depending on your plan and fund options. For retirees or those nearing retirement, bond income can help support withdrawals, though the amount may change over time (Fidelity).

It’s important not to confuse income with certainty. The income from bond funds can go up or down over time, since the fund is always buying and selling bonds (Fidelity). So, while bond funds do pay income, their value can still rise or fall.

The Volatility Management Role

Bond funds help manage a portfolio’s ups and downs. Mixing in bonds diversifies your investments, generates income, and adds some stability. Diversifying across different types of investments can help lower overall risk (Vanguard; U.S. Department of Labor).

That’s why target date funds—those all-in-one retirement funds—tend to add more bonds as you get closer to retirement. These funds start out with more stocks when you’re younger, then gradually shift toward more bonds for extra stability as you near your retirement date (Investor.gov).

The point isn’t that bonds always rise when stocks fall. The goal is a portfolio that doesn’t rely only on the stock market. Bonds can reduce swings compared to owning only stocks, but losses are still possible (Vanguard; U.S. Department of Labor).

Interest-Rate Risk: Why Bond Funds Can Lose Value

One of the biggest risks for bond fund investors is interest-rate risk. When interest rates go up, new bonds pay more, making older bonds less attractive, so their prices fall (Investor.gov). In short: when rates rise, bond prices drop—and when rates fall, bond prices go up (FINRA).

For bond funds, this sensitivity to interest rates is measured by something called “duration.” Duration measures how much the price of a bond or bond fund is expected to change when interest rates change; it is not the same as maturity, which is the length of time until a bond's principal is repaid (FINRA). As a rule of thumb, if interest rates change by 1%, a bond’s price will move in the opposite direction by about its duration (FINRA).

For example, a bond fund with a higher average duration will react more to interest rate changes than one with a lower duration. The longer the average duration or maturity, the greater the impact of rate changes (Fidelity). You can usually find a bond fund’s duration on its fact sheet, under sections like key facts or portfolio data (FINRA).

Credit Risk: Why Higher Yield May Come With Higher Risk

Bond funds also carry credit risk—the chance that the issuer, the entity or institution that borrows the money, won’t pay interest or repay what it owes (Investor.gov). Bonds can also be downgraded by credit rating agencies, which can hurt their price (Fidelity).

Credit risk depends on who issues the bond and how the fund is managed. Government bonds are usually seen as safer, while corporate bonds—especially those rated below investment grade, known as “high-yield” or “junk” bonds—carry more risk of default (Vanguard; Fidelity).

That’s why you shouldn’t judge a bond fund just by its yield. Higher yields might mean more credit risk, more interest-rate risk, or both. It’s smart to check the fund’s prospectus and credit quality guidelines. Keep in mind, funds themselves aren’t rated—even though the bonds inside them are (Fidelity).

Other Risks to Keep in Mind

Bond funds can also be affected by inflation risk—this is when rising prices reduce the purchasing power of your interest payments (Investor.gov). Liquidity risk is another factor, meaning it might be hard to buy or sell certain bonds when you want to—liquidity is how easily an asset can be converted into cash (Investor.gov).

Another key point: most bond funds don’t work like a single bond you hold until it matures. Bond funds and ETFs don’t have an end date, so their value will always go up and down (Fidelity). You can’t count on “holding the fund to maturity” to protect you from price swings—the way you might with an individual bond.

How 401(k) Investors Can Evaluate Bond Funds

If you’re looking at the bond options in your 401(k), start by asking a few practical questions: What’s the fund’s main purpose in your portfolio—income, diversification, capital preservation, inflation protection, or a mix? What’s its average duration, and how much might it change if interest rates move? How good is the credit quality, and how much does it invest in corporate, high-yield, or international bonds?

Your best starting points are the fund’s fact sheet and its prospectus. The fact sheet usually lists the fund’s duration, while the prospectus explains its credit quality guidelines (FINRA; Fidelity). The right mix of bond funds for you depends on your goals, time horizon, risk tolerance, income needs, and what else you own in your 401(k).

For long-term savers, the key takeaway is balance. Bond funds are important tools for managing risk in your 401(k), but they aren’t risk-free. When used thoughtfully, they can help provide income, lower your dependence on stocks, and make your investing journey less bumpy over time.

Source URLs

- Investor.gov, 401(k) Plans

- U.S. Department of Labor, Investing and Diversification

- Investor.gov, Bonds - FAQs

- Investor.gov, Target Date Funds

- FINRA, Brush Up on Bonds: Interest Rate Changes and Duration

- Vanguard, What Are Fixed Income or Bond Funds?

- Fidelity, Risks of Fixed Income Investing

Disclosure

This material is provided for informational and educational purposes only and should not be construed as individualized investment, tax, or legal advice. Investing involves risk, including the possible loss of principal. Bond funds are subject to risks including, but not limited to, interest-rate risk, credit risk, inflation risk, liquidity risk, call risk, and market risk. When interest rates rise, bond prices generally fall, and longer-duration bond funds are typically more sensitive to changes in interest rates. Lower-quality and high-yield bonds may offer higher income potential but carry greater credit and default risk. Diversification and asset allocation do not ensure a profit or protect against loss in declining markets. Retirement plan investment options, fees, tax treatment, and withdrawal rules vary by plan and individual circumstances. Investors should review plan documents, fund fact sheets, and prospectuses carefully and consult their financial advisor, tax professional, or plan provider before making decisions about their 401(k) or other retirement accounts.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119