U.S. equities finished mixed to slightly lower on Wednesday as evidence of steady economic activity and easing cost pressures helped most stocks, but a sharp selloff in chipmakers dragged on the major indexes. Investors took some comfort from June manufacturing data that pointed to continued expansion and slower input-cost inflation, while Federal Reserve Chair Kevin Warsh reinforced his focus on price stability without signaling an imminent policy move. Treasury yields were little changed to slightly lower at the front end, oil fell on more constructive U.S.-Iran diplomacy, and leadership rotated away from semiconductors toward more cyclical and selected software names.

Key Headlines & Market Movers:

- Macro data eased inflation concerns without reviving rate-hike fears: The tone of the day was shaped by a combination of decent growth data and softer price pressure. ISM manufacturing stayed near a multiyear high, but the prices-paid component cooled sharply, suggesting the recent war-related input cost spike may be fading. Warsh’s comments reinforced that inflation risks have come down, yet his refusal to provide forward guidance also meant markets did not interpret the backdrop as a clear signal of a near-term rate move.

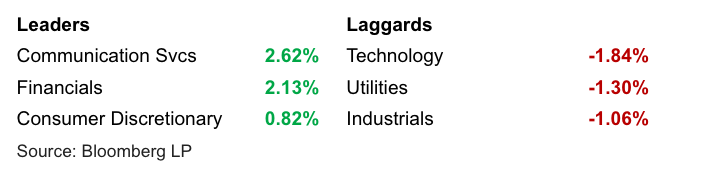

- Chip weakness masked stronger underlying market breadth: Even though most S&P 500 constituents advanced, the headline indexes were pulled lower by a steep decline in semiconductor shares. That created a split market in which broader participation improved, but the index-heavy tech complex still dominated performance at the top level. The result was a session that looked healthier beneath the surface than the major averages alone suggested, with cyclicals and some software names absorbing money as investors reassessed AI and supply-chain exposures.

Corporate stories reinforced a rotation into differentiated themes: Several idiosyncratic company developments added to the sector reshuffling. Meta stood out on reports it is exploring a cloud infrastructure and AI-compute offering, while software stocks gained after analyst upgrades argued that fears of AI permanently impairing the sector may be overdone. Elsewhere, Apple’s reported efforts to secure memory supply, Google’s legal setback in Europe, and Alcoa’s acquisition of South32 assets highlighted how supply chains, regulation, and strategic repositioning remain central stock-specific drivers.

S&P 500 Sector Performance

Looking Ahead

The next major test is Thursday’s U.S. employment report, which could either validate the market’s “goldilocks” view of resilient growth with contained inflation or reopen concerns about policy staying restrictive for longer. A payrolls number that is firm but not too hot would likely support the current preference for cyclicals and broader market participation, especially if unemployment remains stable. With markets then heading into the Independence Day holiday and an early bond close on Thursday, trading could become more event-driven and concentrated around labor data, rates reactions, and whether the recent pressure in semiconductors spills into the rest of tech.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119