How Long-Term Investors Can Separate Significant Information From Daily Market Noise

For many Americans, their 401(k) isn’t just a retirement account—it’s an emotional companion, something they think about often even if retirement is still decades away.

You might get a breaking alert on your phone while eating lunch. Financial news channels flash dramatic red banners about inflation, interest rates, oil prices, elections, or worldwide tensions. Social media turns up the volume on fear, urgency, and speculation—right as you scroll.

All of this creates a constant stream of information, each piece fighting for your focus—and your emotions.

If you’re saving for retirement, one of the most valuable financial skills isn’t predicting the market—it’s learning how to filter what matters.

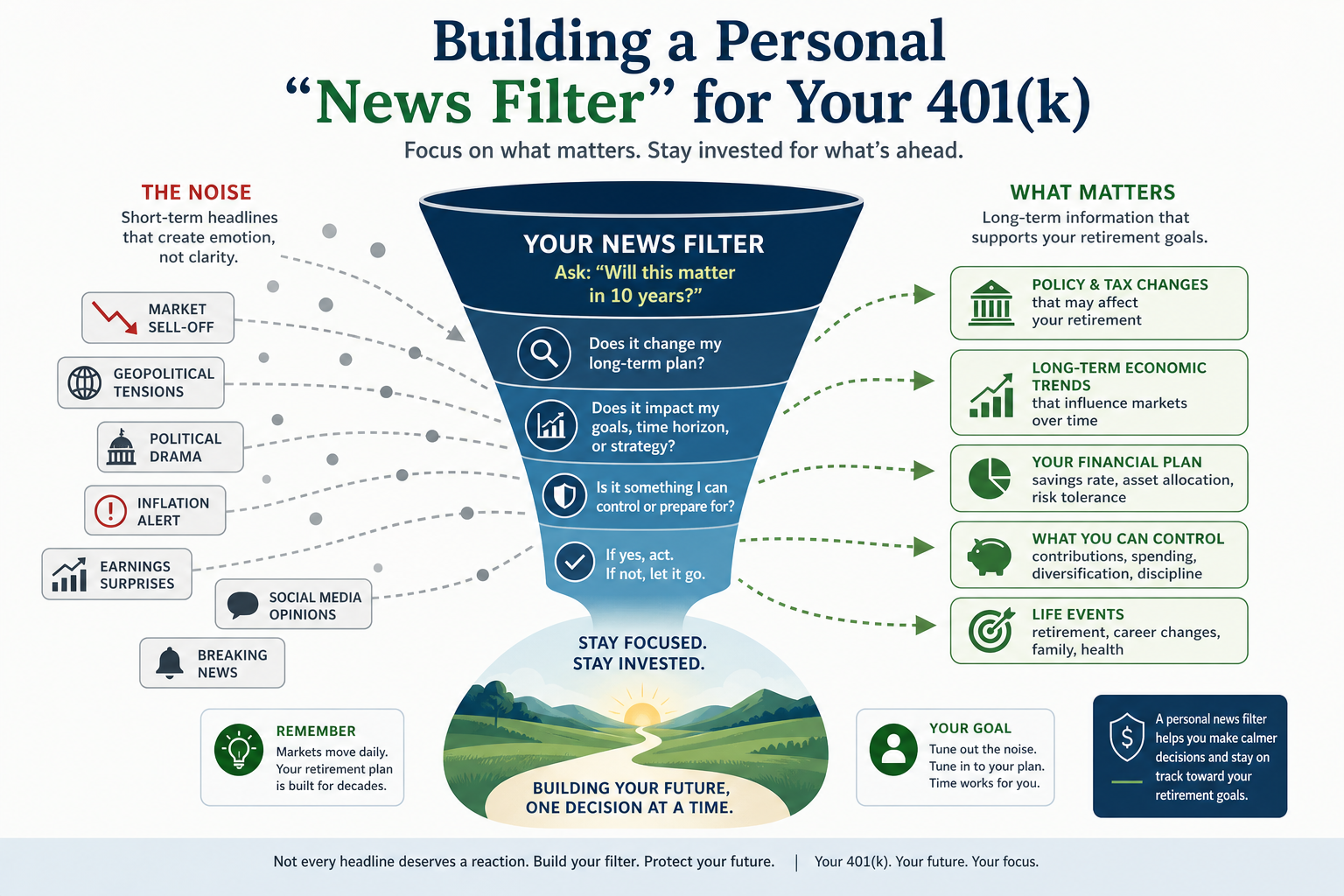

Building your own “news filter” can help you separate what really counts for your long-term retirement plan from what’s just noise or short-term financial chatter.

Why News Feels So Urgent

Modern financial media is designed to reward immediacy. Headlines are written to attract clicks, views, and engagement. Market movements that may be statistically normal are frequently portrayed as dramatic events.

A 1% market decline can become:

- “Stocks Plunge”

- “Markets in Turmoil”

- “Investors Panic”

Yet historically, short-term volatility has been a normal part of investing.

If you’re investing for the long run, reacting to every scary headline can do more harm than the news itself.

The real challenge isn’t tuning out all news—it’s learning how to put it in perspective.

A Useful Question:

“Will This Issue in 10 Years?”

One helpful framework for filtering financial news is asking:

Will this news really change my long-term retirement strategy?

Some events may have enduring implications:

- Major changes to tax law

- Retirement account legislation

- Long-term inflation trends

- Structural financial shifts

- Changes in interest rate environments

- Major life events such as retirement, inheritance, divorce, or career changes

Other headlines can dominate the conversation for days or weeks, with little lasting effect on a decades-long investment plan.

Examples of short-term commentary often include:

- Daily market swings

- Political speculation

- Earnings surprises

- Intraday volatility

- Predictions about “imminent crashes.”

- Constant recession forecasts

- Social media market opinions

That doesn’t mean you should ignore all short-term news—markets do react to current events. But building a secure retirement is usually more about being consistent, staying diversified, and keeping up your contributions over time, not about dealing with every news item.

The Difference Between Information and Noise

Not all financial content fulfills the same purpose.

Some information is educational as well as strategic:

- Understanding diversification

- Reviewing asset allocation

- Evaluating risk tolerance

- Learning about tax-efficient retirement planning

- Monitoring contribution rates

- Rebalancing periodically

Other content is designed primarily for entertainment or emotional involvement.

Investors may benefit from identifying the difference between:

- analysis intended to improve long-term decision making, and

- commentary designed to provoke immediate reactions.

This distinction matters because emotional investment decisions often occur in phases of uncertainty or fear.

Building Your Own News Filter

Every investor’s filter may look different, but several principles can help.

1. Separate Market News From Personal Financial Planning

Markets move constantly. Personal financial plans should usually move much more slowly.

A daily market decline does not necessarily require:

- changing retirement allocations,

- stopping contributions,

- moving entirely to cash, or

- abandoning long-term goals.

Many successful retirement strategies are built around consistency rather than constant adjustment.

2. Focus on Controllable Factors

Investors cannot control:

- Federal Reserve decisions

- Elections

- Inflation reports

- Oil prices

- Worldwide conflicts

- Quarterly earnings results

But investors may have influence over:

- contribution rates,

- savings habits,

- spending discipline,

- diversification,

- debt management,

- tax planning, and

- long-term asset allocation.

A good news filter helps you focus less on what you can’t control—and more on the financial habits you can.

3. Limit Constant Portfolio Monitoring

Checking retirement balances too frequently can increase emotional reactions to normal volatility.

Research in behavioral finance has suggested that investors who constantly monitor their portfolios may experience greater stress and become more vulnerable to short-term decision-making.

If you’re a long-term saver, checking your accounts every so often—not every day—can help you stay calm and stick to your plan.

4. Evaluate the Source

Not every financial opinion deserves the same importance.

Before reacting to commentary, investors may want to consider:

- Is the source reputable?

- Is the information data-based?

- Is the content educational or sensational?

- Does the source benefit from generating fear or alarm?

- Is the analysis centered on long-term investing principles?

Trusted financial journalism and evidence-based planning often differ significantly from emotionally driven online commentary.

5. Remember Historical Background

Markets have historically experienced:

- recessions,

- wars,

- inflation cycles,

- banking crises,

- political uncertainty,

- technology disruptions, and

- periods of elevated volatility.

Even through all these events, investors who stayed diversified and patient have often seen their investments recover—and grow—over time.

That does not guarantee future results. But historical background can help investors avoid viewing every market decline as unprecedented.

Long-Term Plans Usually Require Long-Term Thinking

A 401(k) is fundamentally designed as a long-horizon investment vehicle.

For someone 20 or 30 years from retirement, the larger risks may not always be short-term market variability. Instead, risks may include:

- insufficient savings,

- failing to stay invested,

- emotional reactions,

- poor diversification,

- inflation over time, or

- abandoning a long-term plan during uncertainty.

Creating a personal news filter does not imply ignoring the economy or avoiding financial education. It means developing a framework that helps distinguish:

- information that aids long-term planning,

from - commentary that encourages short-term emotional reactions.

In a world full of nonstop headlines, having this discipline might be one of the best investments you make for your future self.

Source URLs

- https://www.investor.gov/introduction-investing/general-resources/news-alerts/alerts-bulletins/investor-bulletins-95

- https://www.fidelity.com/learning-center/personal-finance/how-often-check-investments

- https://www.vanguard.com/investor-resources-education/article/tune-out-the-noise

- https://www.schwab.com/learn/story/behavioral-finance-how-emotions-affect-your-investing

- https://www.morningstar.com/personal-finance/how-ignore-market-noise

- https://www.finra.org/investors/insights/avoiding-emotional-investing

Disclosure

This article is for informational and educational purposes only and should not be considered investment, tax, or legal advice. Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. Individuals should consult with a certified financial advisor, tax professional, or legal advisor regarding their specific situation before making financial decisions. Advisory services are offered through a Registered Investment Advisor (RIA). This material may contain general market commentary and should not be construed as a recommendation to buy or sell any security.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119