Relying solely on cash isn’t a long-term strategy. While it can feel safe, cash usually won’t keep up with inflation or help your wealth grow over time. Even if your account balance looks stable, over a full market cycle, using cash as your main asset puts your portfolio at risk of quietly losing purchasing power.

The Comfort of Cash in Today’s Environment

It’s easy to see the appeal of higher short-term yields, especially after a choppy or low-rate period. Putting more money into money markets or savings accounts can feel like a way to earn a "risk-free" return and avoid big losses. But that sense of safety is mostly about what’s happening right now. Today’s yield is based on current policy—not on what you’ll need over the next 10, 20, or 30 years.

When rates return to more typical levels—as they always do—cash yields can drop quickly, sometimes ending up just above or even below inflation. That yield that once felt “good enough” can suddenly leave you falling short of your long-term goals.

Inflation: The Risk You Don’t See on a Statement

Most investors watch for volatility, but the bigger risk for cash is inflation. If you have a lot of cash in your portfolio, your account balance might hold steady or even grow a bit, but what you can actually buy with that money can slowly slip away. The real danger isn’t seeing your balance drop—it’s realizing your lifestyle can’t keep up.

Take retirement, for example—a plan that seems fully funded today might become stretched or even fall short if your returns don’t keep up with rising costs. Over 10 or 20 years, even low inflation can shrink the real value of a portfolio that’s heavy on cash, and that’s hard to fix later on.

The Opportunity Cost of Sitting on the Sidelines

Every extra dollar you keep in cash is a dollar that’s missing out on the long-term growth that comes from productive assets. Stocks, bonds, and other investments reward you for riding out the ups and downs—cash usually doesn’t. Over 15 to 30 years, even missing a few percentage points a year can mean a much smaller nest egg and fewer choices for you and your family down the road.

This isn’t just about missing out on returns—it’s also about how you allocate your money. Having some cash set aside is useful for rebalancing or jumping on opportunities when markets dip. But if cash becomes your default place to park money whenever you’re uncertain, it can start holding you back instead of helping you.

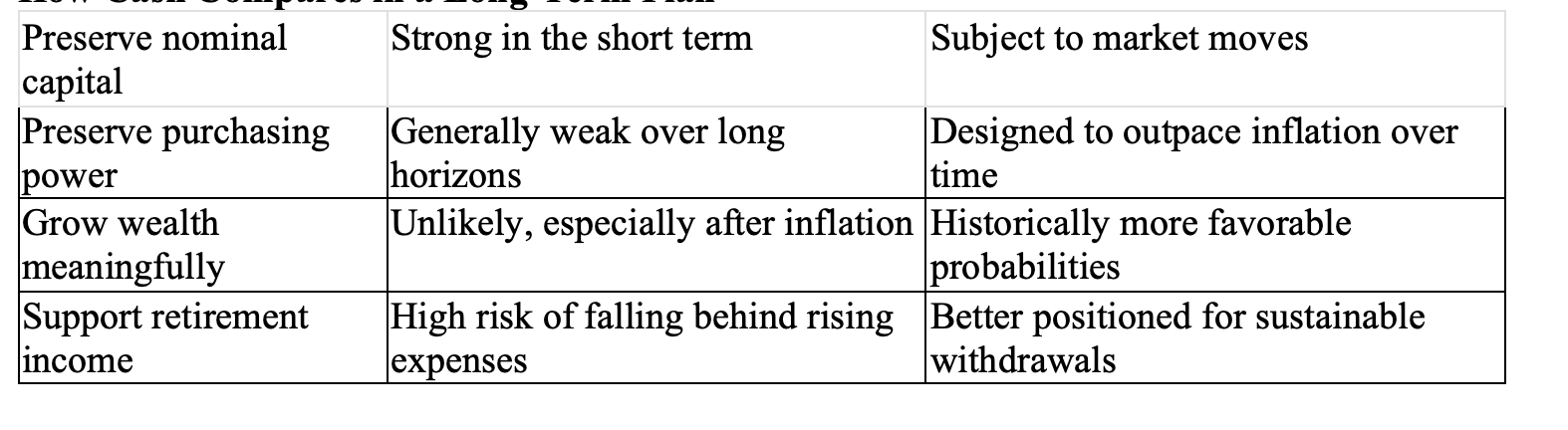

How Cash Compares in a Long‑Term Plan

Where Cash Truly Belongs in Your Allocation

To be clear, cash isn’t the enemy—it’s important when you use it intentionally. The real question isn’t “cash or no cash,” but rather, “how much, and what is it for?” Usually, cash serves its purpose in three main areas:

- Liquidity and resilience: Emergency reserves and operating cash, so that unexpected events do not force you to liquidate long‑term holdings at the wrong time.

- Known near‑term liabilities: Funds earmarked for obligations within the next one to three years—tax payments, near‑dated capital calls, tuition, or a planned purchase.

- Optionality and discipline: A measured cash allocation that allows you to rebalance into risk assets during drawdowns, acting as a source of strength instead of a sign of indecision.

Outside of these roles, holding too much cash is often just a sign that a decision hasn’t been made yet—not a true investment choice.

Putting Cash in Its Proper Place

For investors in this room, the key questions are strategic, not emotional:

- What is the explicit job of each pool of capital—safety, income, growth, legacy?

- Over what time horizon is each pool expected to be used?

- Given your return requirements and risk tolerance, how much of your balance sheet can truly afford to sit in instruments that are unlikely to beat inflation over time?

Answering these questions usually leads to a plan where cash is right-sized—not eliminated. You want enough to give you stability and flexibility, but not so much that it quietly works against your biggest goals. A disciplined approach to cash, built into your investment plan (not just reacting to today’s news), helps ensure that cash stays a helpful tool instead of becoming the whole strategy.

Disclosure:

This material is provided for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security or investment strategy. The views expressed are generic in nature, are not intended as, and should not be construed as, investment, tax, legal, or accounting advice, and may not be appropriate for all investors. Any references to asset classes (including cash, bonds, and equities) are for illustrative purposes only and do not represent a recommendation or prediction regarding any specific investment or portfolio. Investing involves risk, including the possible loss of principal, and there is no guarantee that any strategy will achieve its objectives or that any investment will maintain its value or keep pace with inflation. Past performance is not indicative of, and does not guarantee, future results. Investors should consider their individual financial circumstances, objectives, risk tolerance, and liquidity needs before making any investment decision and should consult with a qualified financial professional regarding their specific situation.

Sources

https://www.fidelity.com/learning-center/trading-investing/how-much-cash-should-you-hold

https://hbkswealth.com/insights/hidden-cost-cash-investment-strategy-market-volatility/

https://www.ml.com/articles/how-much-is-too-much-cash-in-your-portfolio.html

https://www.troweprice.com/financial-intermediary/us/en/insights/articles/2023/q3/why-holding-too-much-cash-on-the-sidelines-can

https://mai.capital/resources/why-cash-is-not-a-long-term-investment/

https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/principles-for-investing/

https://www.nixonpeabodytrustcompany.com/insights/investment-strategy-aligning-investments-with-long-term-goals

https://www.schwab.com/learn/story/yields-on-cash-have-fallen-what-is-your-plan

https://www.sec.gov/newsroom/press-releases/2020-334

https://www.sec.gov/rules-regulations/staff-guidance/division-investment-management-frequently-asked-questions/marketing-complia

https://www.law.cornell.edu/cfr/text/17/275.206(4)-1[11]

https://www.assetmark.com/blog/guide-sec-marketing-rule

https://www.finra.org/rules-guidance/notices/08-82

https://www.finra.org/rules-guidance/key-topics/suitability

https://www.finra.org/rules-guidance/rulebooks/finra-rules/2111

https://www.finra.org/investors/investing/investing-basics/ris

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119