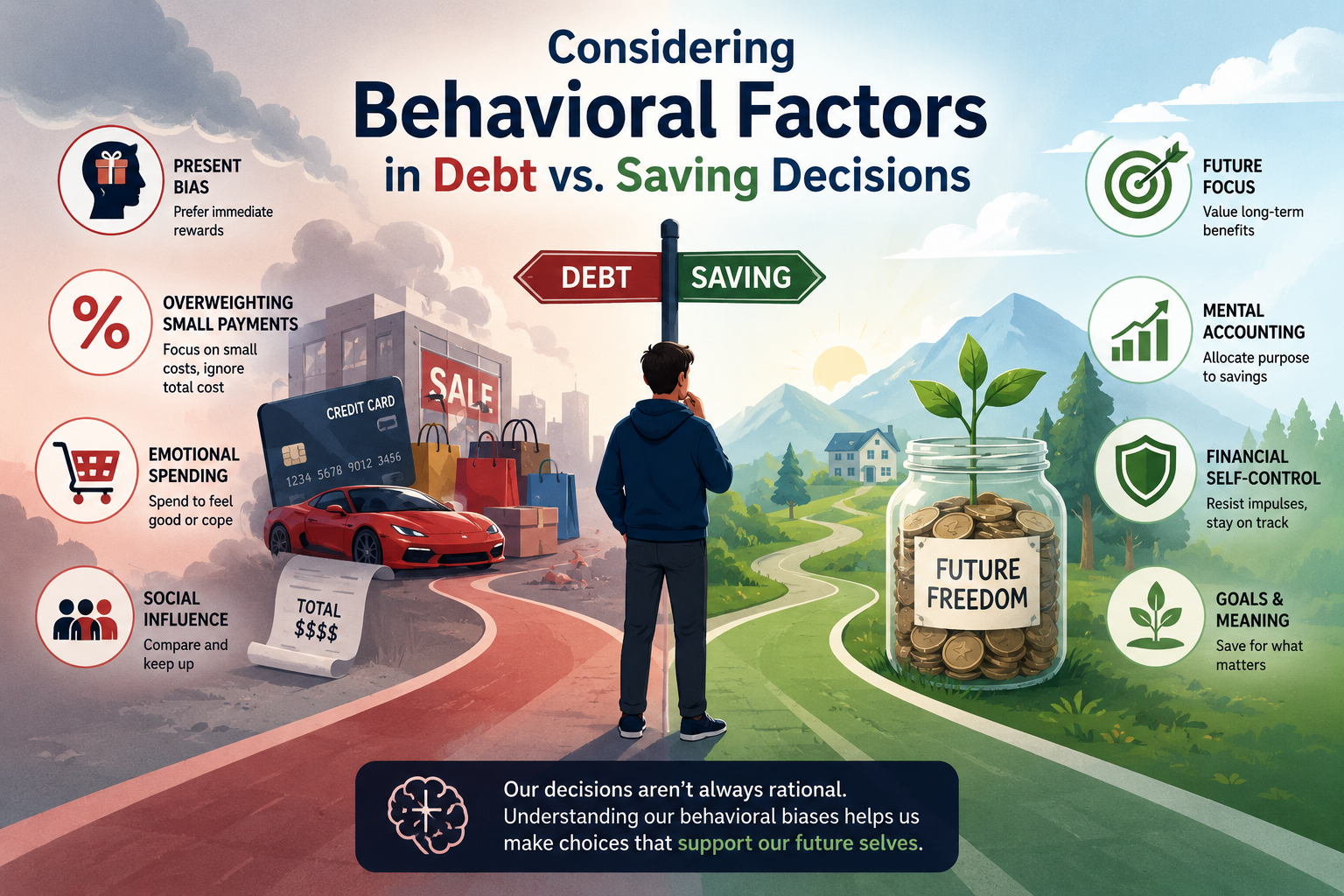

Financial decisions are more than calculations. The decision to use extra cash for debt, emergency savings, or retirement involves factors like interest rates, returns, and math—but a sharper reality is that math alone is not the full answer.

Your behavior is as critical as the numbers. A plan that works in theory fails if it doesn’t match your habits or creates stress. The strongest long-term plan is not the mathematically purest—it's the one that fits your goals and how you actually live.

Why the “best” answer is not always purely mathematical

Debt repayment and saving compete for the same dollars. Paying down high-interest debt reduces future costs, while building savings provides a buffer to avoid more debt in emergencies. Contributing to retirement can secure long-term stability and, for some, capture employer contributions.

These priorities can overlap. The Consumer Financial Protection Bureau says an emergency fund is a buffer against unplanned expenses, and that a lack of savings can turn a financial shock into lasting debt. This highlights the value of maintaining some savings even while paying down debt.

Recognize that debt and savings plans should work together. Instead of choosing between debt and savings, coordinate both so your household can manage them reliably. Free up future dollars and lower stress by maintaining a balanced, sustainable approach.

Comfort influences whether a plan is sustainable.

Comfort doesn't mean avoiding tough decisions. It's about how a plan feels day to day, not just on paper. FINRA notes that the risk you can technically afford differs from the risk you’re comfortable with. While FINRA discusses this in the context of investing, the idea applies to household finances: being able to do something doesn't mean you'll want to—or will stick with it.

You could put every extra dollar toward debt, but that can feel restrictive if it leaves no room for surprises. Or you may prefer a larger cash cushion but worry about high-interest balances lingering. A practical plan should recognize emotions—without letting them override the finances.

Understand that comfort affects your ability to follow through. If losing money or a harsh budget makes you want to quit, revise your approach. Choose a strategy you know you can sustain for the long term, not just one that works best on paper.

Motivation can shape debt payoff choices.

Consider debt payoff: the “avalanche” method targets the highest-interest debt first to save on interest, while the “snowball” method pays off the smallest balances first for quick wins and momentum.

Wells Fargo explains that the avalanche method saves money by focusing on expensive debt first. The snowball method pays off the smallest debt, then rolls that payment into the next. High-rate focus is efficient, but paying off small debts quickly can be rewarding and help motivation—especially if you like to see immediate results.

Research shows motivation affects debt repayment. A Journal of Consumer Research study examined how strategies impact the drive to pay off debt. Not everyone should chase quick wins, but motivation and persistence matter when choosing a payoff strategy.

Habits can make progress more automatic.

Saving and debt repayment are easier when built into a system. The CFPB says building savings is easier with consistent deposits and recommends goal-setting, contributions, progress tracking, and celebrating success to build strong savings habits. Automatic transfers are also an effective way to save consistently.

This habit logic applies to debt repayment. A household might schedule payments after payday, direct extra funds to one debt, or set reminders to track balances. Reducing decisions makes the process repeatable.

Habits can guard against backsliding. The CFPB recommends keeping emergency funds safe and separate from spending to limit temptation. Structure matters because plans often fail through many small slips, not one big mistake.

The role of emergency savings in debt decisions

Emergency savings can seem counterintuitive when trying to reduce debt. When a credit card has a high rate, saving instead of paying debt may seem inefficient. Yet savings can prevent turning the next unexpected expense into new credit card debt.

The CFPB explains that emergency savings help households avoid relying on credit or loans for unexpected expenses, which can grow with interest and fees. Even modest savings may offer meaningful protection.

This doesn't mean emergency savings always take priority over debt. It means decisions should weigh both debt cost and risk of having no cushion. Paying down debt aggressively while leaving no safety net may invite setbacks.

Retirement savings add another layer.

Retirement savings complicate the debt-versus-saving decision. Workers may juggle credit card, student loan, car loan payments, emergency savings, and 401(k) contributions. The right balance depends on rates, employer match, cash flow, retirement horizon, taxes, and emotional commitment.

FINRA emphasizes that financial decisions should align with objectives, needs, time horizon, market tolerance, and the situation. In debt and retirement contexts, the answer differs for someone with high-interest debt and no savings versus low-interest debt, stable income, and strong retirement habits.

Avoid all-or-nothing thinking. Some households may make required debt payments, build an emergency fund, contribute enough to get an employer match, and then allocate extra dollars based on rates and behavioral fit. Others may focus on liquidity before increasing retirement savings. Planning should reflect the full household balance sheet.

Questions that can help frame the decision

Behavioral factors don’t replace financial analysis—they test if a plan holds up. Consider questions like:

· What would make the plan feel manageable? A plan that requires extreme sacrifice may be difficult to sustain.

· What creates the most motivation? Some households are motivated by minimizing interest costs, while others need early visible progress to build confidence.

· What habits can be automated? Automatic savings, scheduled debt payments, and paycheck-based routines can reduce decision fatigue.

· What would prevent new debt? A small emergency reserve may help avoid turning the next unexpected bill into a new balance.

· What tradeoffs are acceptable? A plan may intentionally blend debt repayment and saving rather than prioritizing one over all others.

These questions shift the conversation from “What should work?” to “What will work best for this household?”

Bottom line

Debt and saving decisions require math, but ignoring behavior is a mistake. Interest, returns, matches, and liquidity are important, but the sharper truth is that comfort, motivation, routine, and the ability to follow through must be central to any plan.

A thoughtful financial plan recognizes that the most efficient answer is not always the most sustainable. For many households, lasting progress combines sound math with real behavior—maintaining a cash buffer, paying debts, automating good habits, and revisiting as life changes.

Source URLs

· https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/

· https://www.finra.org/investors/insights/know-your-risk-tolerance

· https://academic.oup.com/jcr/article-lookup/doi/10.1093/jcr/ucw037

This material is provided for informational and educational purposes only and should not be construed as personalized investment, tax, legal, credit, or retirement plan advice. The information does not constitute a recommendation to borrow, repay debt in a particular order, contribute to a retirement plan, change an investment allocation, or use any specific financial strategy. Debt repayment, saving, and investing decisions should be based on individual goals, income, expenses, interest rates, liquidity needs, risk tolerance, tax considerations, plan rules, and financial circumstances. Investing involves risk, including the possible loss of principal, and past performance is not indicative of future results. Investors should consult their financial advisor, tax professional, credit counselor, or retirement plan representative before making changes to their debt repayment, savings, or investment strategy.

Recent Articles

%20Plan%20Document%20Aligned%20With%20How%20You%20Operate%20the%20Plan.png)

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119