%20Plan%20Document%20Aligned%20With%20How%20You%20Operate%20the%20Plan.png)

For a business owner sponsoring a 401(k) plan, the written plan document is the foundation of everything: it describes who can participate, how contributions work, when money can be taken out, and more. To keep the plan tax‑qualified, it must be both written correctly and operated in accordance with its written document. Mid‑year is a good time to ask a simple but important question: does your day‑to‑day administration still match what your plan document says?

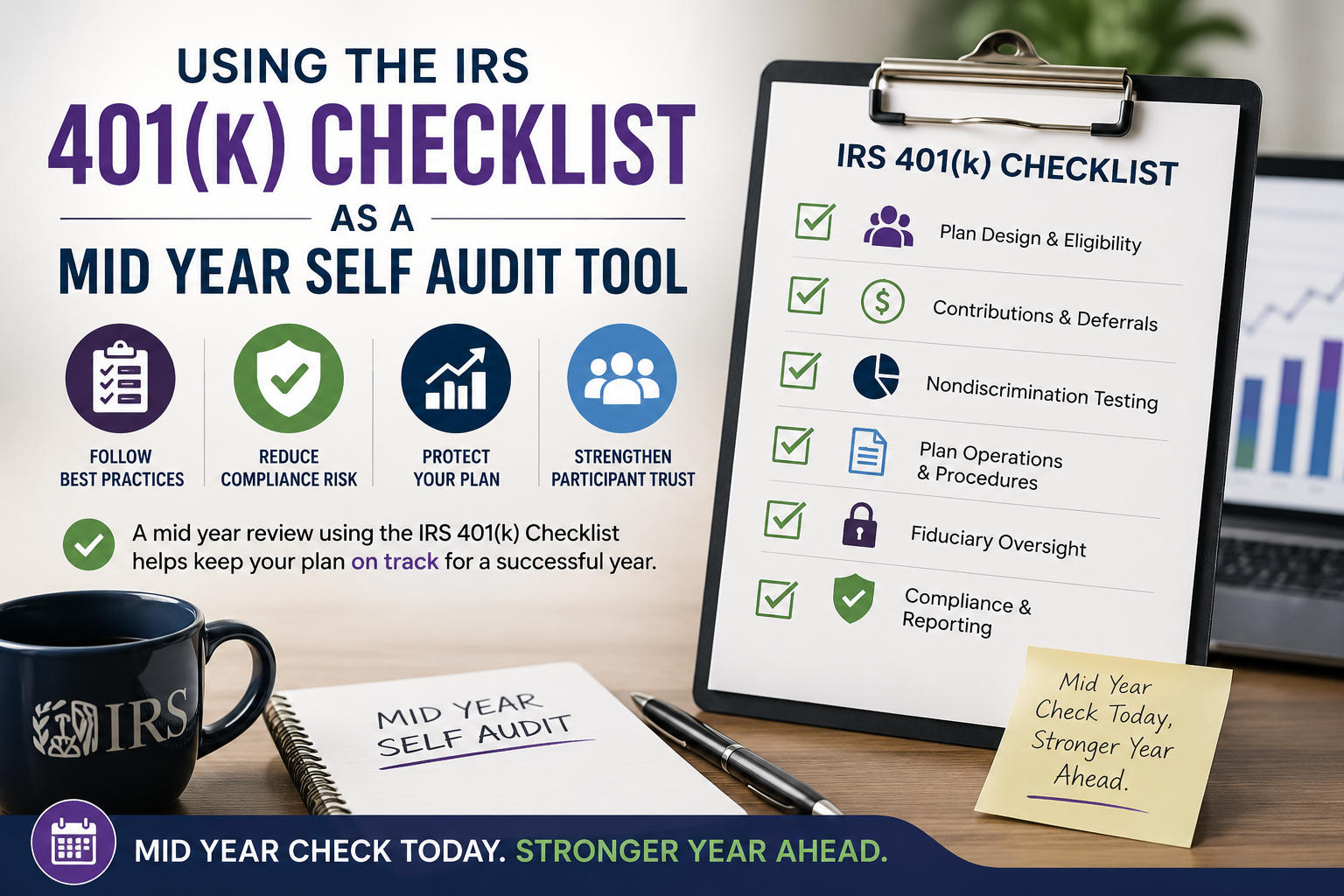

Why alignment between document and operations matters

A qualified plan must satisfy legal requirements in both form and operation. That means the provisions in your plan document must meet applicable standards, and your team must follow those provisions consistently in practice. When those two pieces do not match—for example, if eligibility is applied differently than the document describes—errors can accumulate and may eventually require corrections, including possible filings or tax consequences.

Maintaining alignment helps you:

- Reduce the risk of operational errors that could affect participants’ benefits.

- Make it easier to respond if regulators or auditors review your plan.

- Demonstrate that you are taking your responsibilities as plan sponsor seriously.

What your plan document is supposed to cover

A 401(k) plan begins with a written document that sets out how the plan is designed and how key functions will be carried out. The document typically covers several core areas, including:

- Eligibility and entry dates. Who can join the plan, and after how many service hours or years of service?

- Compensation and contributions. What counts as compensation, and how employee deferrals and employer contributions are calculated and deposited.

- Vesting and distributions. When employer contributions vest, and under what circumstances distributions or loans can be made.

- Plan administration and trustees. Who is responsible for day‑to‑day decisions and how plan assets are held in trust.

When laws change, or your business evolves, the plan document often requires amendments to continue to reflect both current rules and your intended design. That makes it useful to regularly compare the document with actual operations.

Mid‑year steps to compare document vs. operations

A mid‑year review doesn’t need to be complicated. A practical, business‑owner‑friendly process can start with a few core steps:

- Collect core documents and records.

Gather your plan document, adoption agreement, all recent amendments, and the summary plan description that participants receive. Include a sample of payroll reports and contribution records to show how the plan is applied in practice. - Review key provisions against how you actually run the plan.

-

- Compare eligibility rules in the document with how your HR or payroll systems determine who can defer and when they enter the plan.

- Check how compensation is defined in the plan against the earnings fields used to calculate deferrals and employer contributions.

- Confirm that the contribution formulas, vesting schedules, and loan or hardship policies in the document align with the procedures your team and service providers follow.

- Look for “we do it differently” moments.

If you discover that practice has drifted—for example, if you have been allowing part‑time employees to enter sooner than the document specifies—that may be a sign that either operations need to be brought back in line or the document needs to be updated. In either case, the next step is to identify the mismatch and address it promptly. - Document your findings and questions.

Make a simple list of areas where things are clearly aligned, and areas where you are uncertain or see potential inconsistencies. This written record can help guide conversations with your advisors and support your fiduciary oversight.

When to involve professionals

Plan sponsors are responsible for keeping the plan document compliant and operating the plan according to its terms. If your mid‑year review surfaces questions or possible gaps, it can be helpful to involve professionals by:

- Talk with your recordkeeper or third‑party administrator about how their systems are currently set up and whether they match the document language.

- Consult with legal counsel or other qualified professionals if amendments or corrections may be needed.

- Use official guidance and checklists to understand common issues and general correction frameworks.

In some cases, relatively small document updates or procedural changes can bring operations back into alignment, reduce risk, and help you address the most pressing issues first. That is why it helps to address issues before they become larger problems.

Making document‑to‑operations alignment a recurring habit

Reviewing plan requirements regularly—rather than only when a problem has already occurred—can make oversight more manageable. Building a habit of comparing your plan document to actual practice at least once a year, mid-year and again near year-end, helps you address the most important gaps first and keep your 401(k) a strong, reliable benefit for your employees while staying within the rules that give it tax advantages.

Ready to review your plan document?

If you’re unsure whether your 401(k) is being administered exactly as it’s written, a mid-year checkup can be a good place to start. Duncan Williams Asset Management can help you understand the questions to ask, coordinate with your plan’s service providers, and identify areas where additional professional input may be useful. To learn more about how we support business owners in overseeing their retirement plans, contact our team to schedule a conversation about your plan’s current structure and goals.

Sources

- Internal Revenue Service – IRC 401(k) Plans: Establishing a 401(k) Plan: https://www.irs.gov/retirement-plans/irc-401k-plans-establishing-a-401k-plan[irs]

- Internal Revenue Service – A Guide to Common Qualified Plan Requirements: https://www.irs.gov/retirement-plans/a-guide-to-common-qualified-plan-requirements[irs]

- Internal Revenue Service – A Plan Sponsor’s Responsibilities: https://www.irs.gov/retirement-plans/a-plan-sponsors-responsibilities[irs]

- Internal Revenue Service – Maintaining Your Retirement Plan Records: https://www.irs.gov/retirement-plans/maintaining-your-retirement-plan-records[irs]

- Internal Revenue Service – 401(k) Plan Checklist and Fix‑It Guide: https://www.irs.gov/retirement-plans/401k-plan-checklist[irs]

Disclosure

This material is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. It is not intended to be, and should not be construed as, a recommendation to adopt any specific plan design, investment, or strategy. The information here is general in nature and may not reflect the current rules or guidance applicable to your specific situation. Business owners and plan sponsors should consult with their qualified tax advisors, legal counsel, and retirement plan professionals before making any decisions regarding their 401(k) or other retirement plans.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119