Stocks extended recent gains as softer labor data reinforced expectations for a December rate cut. The S&P 500 notched its seventh advance in eight sessions, supported by falling bond yields and a weaker dollar. While megacaps were mixed, dragged by Microsoft, broader participation helped lift equities. Treasury yields eased further, with the 2-year dipping below 3.5%, as traders priced in a near-certainty of Fed action next week.

Key Headlines & Market Movers:

- ADP Miss Reinforces Cut Expectations: Private payrolls declined by 32,000 in November, far below forecasts for a 10,000 gain, marking the worst print since early 2023. Small businesses were especially weak. This data, coupled with rising unemployment and layoff headlines, added to the narrative that the labor market is slowing meaningfully. The market is now assigning a 90%+ probability to a 25-basis-point rate cut at the Fed’s final 2025 meeting.

Yields Fall, Dollar Softens Sharply: Treasury yields declined across the curve, with the 2-year settling at 3.48% and the 10-year at 4.06%. The U.S. dollar saw its worst day since September, particularly under pressure against low-yield currencies like the yen. Strategists noted that the greenback is aligning more closely with the dovish shift in rate expectations, increasing downside risks in the near term.

- Tech Mixed as Microsoft Slides, AI Under Scrutiny: Microsoft fell 2.5% after reports of lower demand for AI software tools and reduced sales quotas, though the company later clarified that quotas hadn’t been cut. Nvidia also slipped amid uncertainty about chip exports to China. Broader AI sentiment remains strong, but recent headlines suggest a near-term pause in enthusiasm. Meanwhile, Tesla outperformed, up 4%, and American Eagle and Marvell both posted strong earnings-driven gains.

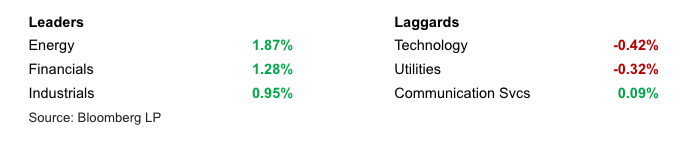

Market Breadth Strong Despite Mega-Cap Weakness: Roughly 350 names in the S&P 500 advanced, indicating broad-based buying. The Dow gained the most, up 0.9%, led by industrials and energy. The Russell 2000 rallied nearly 2%, benefiting from lower rates and a weaker dollar. Bitcoin also rose, hovering near $93,000, recovering sharply from early-week losses.

S&P 500 Sector Performance

Looking Ahead

Markets are now firmly positioned for a Fed rate cut next week, with incoming inflation data on Friday (September PCE) likely to shape messaging around future policy moves. While rate-sensitive assets are benefiting, the divide within the Fed and persistent inflation could temper expectations for aggressive easing in 2026. For now, the rally remains intact, driven by a softening macro backdrop and growing confidence in policy support.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119