U.S. stocks ended mixed after another sharp rotation out of semiconductor and other high-profile AI names and into a broader set of companies tied to steadier growth. The headline indexes finished little changed overall, but internal market breadth was stronger, with the equal-weight S&P 500 hitting a record high as investors looked past weakness in chip stocks. Lower oil prices and signs of economic resilience helped cushion sentiment, even as valuation concerns kept pressure on parts of the technology complex.

Key Headlines & Market Movers:

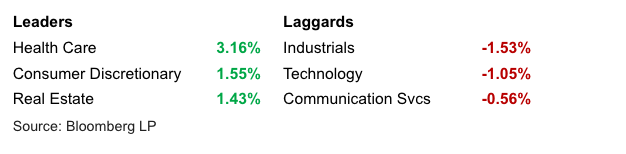

- Tech leadership pauses as AI enthusiasm meets valuation pressure: Semiconductor stocks were hit again, extending a volatile stretch for one of the market’s strongest groups this year. The selling came as investors reassessed how far AI-linked names had run and whether infrastructure spending and commercialization expectations had moved ahead of near-term reality. Even so, several market commentators in the source material framed the move as a consolidation or pause rather than a broader breakdown in the AI theme.

- Broader market strength offsets weakness in chips: While the major indexes wavered, the tone beneath the surface was firmer than the headlines suggested. Most S&P 500 constituents advanced, and the equal-weight version of the index reached a record, signaling that money continued to rotate into a wider set of sectors and stocks. That supports the view that investors are not exiting equities outright, but instead repositioning toward areas seen as better aligned with improving growth prospects and less stretched valuations.

Corporate and macro crosscurrents shape risk appetite: Reports that OpenAI may delay a wider rollout path for its next model and potentially postpone an IPO weighed on sentiment around AI-linked names and SoftBank in particular. At the same time, a drop in crude prices offered relief to markets, while Treasury yields edged lower after inflation data was described as in line with expectations. Corporate headlines also reinforced that the semiconductor and industrial landscape remains active, with major investment plans in South Korea, Onsemi’s agreement to buy Synaptics, and Boeing winning a sizable China Southern order.

S&P 500 Sector Performance

Looking Ahead

Next week, investors will likely focus on whether the rotation away from AI leaders stabilizes or broadens further, especially if incoming economic data continue to support the case for resilient growth without reigniting inflation fears. The key question is whether weaker semiconductor momentum remains a contained valuation reset or starts to weigh more heavily on overall risk appetite. If rates stay contained and earnings expectations hold up, the broader market’s recent resilience suggests leadership could continue to widen even if former highflyers remain choppy.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119