Markets were mixed Wednesday as tech stocks saw another steep selloff, led by software and semiconductor names. The Nasdaq 100 posted its worst two-day decline since October, dragged lower by weakness in the “Magnificent Seven” and a sharp drop in Advanced Micro Devices. However, a broader rotation into cyclicals, small caps, and value names helped cushion losses in the S&P 500 and lift the Dow. Bitcoin fell sharply, while bond yields edged higher and crude prices climbed on geopolitical uncertainty.

Key Headlines & Market Movers:

- Tech Rout Deepens Amid AI Concerns and Valuation Repricing: Another wave of selling hit software and chip stocks as fears of AI-driven disruption and valuation compression rattled investors. AMD dropped 17% despite beating earnings estimates, while the software sector slid again as funds exited momentum-heavy trades. The Nasdaq 100 breached its 100-day moving average, a technical level some see as a warning of further weakness. Short sellers have profited handsomely in the space, with AI anxiety driving indiscriminate selling, even among firms posting solid growth.

Rotation to Value and Small Caps Gains Momentum: While tech dragged on major indexes, a rotation into value, cyclicals, and equal-weighted strategies gained traction. The equal-weight S&P 500 rose 0.9%, reflecting strength outside megacaps. This shift signals increasing investor confidence in economic growth, supported by resilient service-sector data and firm earnings guidance. However, the violent unwind in momentum and high-beta strategies points to ongoing volatility beneath the surface.

- Earnings Season Sparks Divergence: Earnings results produced sharp moves across sectors. While AMD and Uber sank post-report, Enphase Energy jumped 36% and Eli Lilly surged 9% back above a $1T market cap. Silicon Labs soared 50% after a $7.5B buyout by Texas Instruments, which itself fell 2%. Alphabet and Amazon earnings are in focus, with markets watching for signs that tech bellwethers can re-anchor sentiment.

Bitcoin Slips; Commodities Mixed: Bitcoin fell below $73,000 and is testing key levels amid broader risk-off sentiment. Gold stayed under $5,000 despite intraday gains, while crude oil rose as mixed messages from U.S.-Iran nuclear talks added to supply uncertainty. Treasury yields ticked up slightly, with the 10-year finishing near 4.28%.

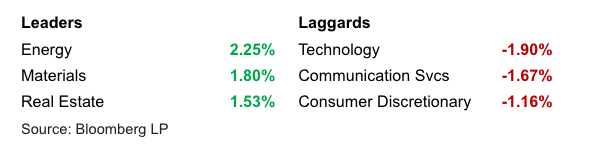

S&P 500 Sector Performance

Looking Ahead

The rotation out of megacap tech continues to reshape market leadership, but improving macro data and solid earnings trends suggest underlying strength. Investors will closely watch upcoming results from Alphabet and Amazon, as well as the broader tone of tech earnings in the days ahead. While software stocks look oversold in the near term, long-term upside may be capped if valuation multiples are re-rated lower. Diversification remains key, with consumer, financials, and healthcare sectors gaining favor as the rally broadens.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119