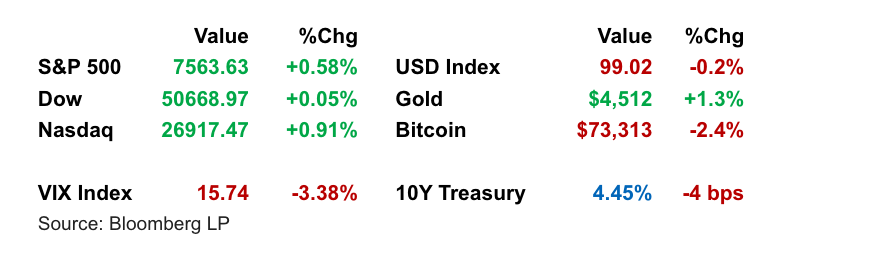

U.S. stocks pushed to fresh all-time highs as reports of a tentative U.S.-Iran ceasefire extension helped ease fears of deeper energy-supply disruption, sending Treasury yields lower and taking some pressure off oil. The rally was broad enough to lift major indexes to records, with technology leading, though the macro backdrop remained mixed as inflation stayed elevated while first-quarter growth was revised lower.

Key Headlines & Market Movers:

US-Iran Deal Reports Drive Risk-On Move: Markets rallied after reports that the U.S. and Iran reached a tentative agreement to extend the ceasefire by 60 days and restart nuclear talks. The potential reopening of the Strait of Hormuz remains the key market variable, given its importance to global oil flows and inflation expectations. Officials stopped short of confirming a final deal, so investors are pricing relief but not full resolution.

- Inflation and Growth Data Complicate Fed Outlook: April PCE inflation matched annual expectations, while monthly readings came in slightly softer than feared, helping bonds rally and supporting equities. Still, inflation accelerated from March, personal income was flat, and first-quarter GDP was revised down to 1.6%, reinforcing a less comfortable mix of slower growth and sticky prices. That combination limits the Federal Reserve’s room to cut rates and keeps policy uncertainty elevated.

Corporate Earnings Add Momentum Beneath the Surface: Snowflake surged after a stronger outlook and a major multiyear AI-cloud agreement with Amazon, reinforcing investor enthusiasm around enterprise AI spending. Retailers including Kohl’s, Best Buy, Dollar Tree, and Hormel also rallied sharply, suggesting investors found enough evidence that consumers remain willing to spend selectively. Microsoft led gains among the megacap technology names, while rail stocks weakened after regulators paused review of the Union Pacific-Norfolk Southern merger.

S&P 500 Sector Performance

Looking Ahead

Markets will remain highly sensitive to confirmation or denial of the U.S.-Iran ceasefire extension, especially any concrete path toward reopening Hormuz and normalizing energy flows. Investors will also watch whether softer monthly inflation momentum can persist despite higher oil-linked price pressures, as the Fed is unlikely to regain flexibility without clearer evidence that inflation is cooling. Corporate guidance, particularly from AI-linked firms and consumer-facing companies, will be important in determining whether record stock prices are supported by earnings momentum or simply by geopolitical relief.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

%20Plan%20Document%20Aligned%20With%20How%20You%20Operate%20the%20Plan.png)

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119