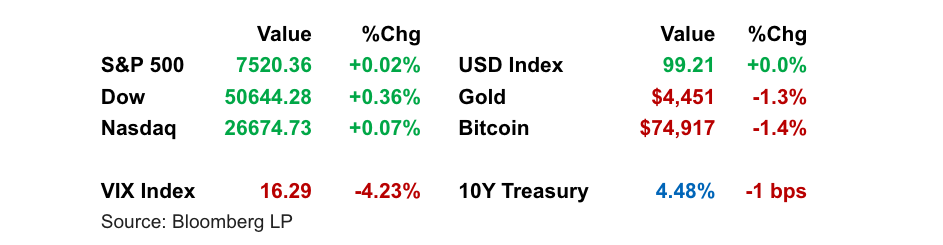

Stocks ended mixed and largely flat Wednesday as traders weighed conflicting signals on U.S.-Iran negotiations and the potential reopening of normal shipping through the Strait of Hormuz. Oil fell sharply on earlier optimism around a draft peace framework, but equities lost momentum after President Trump said he was “not satisfied” with negotiations and U.S. officials denied reports of an interim deal. The Dow reached a new high, while banks and semiconductors lagged and Meta helped support mega-cap tech.

Key Headlines & Market Movers:

Conflicting Iran Signals Drive Oil Lower but Cap Equity Gains: Crude prices dropped after reports suggested a deal could restore normal Strait of Hormuz traffic within a month, but the rally in risk assets faded as U.S. officials pushed back on the report. Trump emphasized that no one country would control the waterway and downplayed sanctions relief, underscoring unresolved sticking points. Markets appear to be pricing in eventual progress, but not a clean or immediate resolution.

- AI and Earnings Momentum Remain Core Bullish Support: Strategists continued to frame the equity rally as earnings-led rather than purely speculative, with AI-related growth still driving optimism. Goldman Sachs raised its year-end S&P 500 target to 8,000, citing earnings growth tied to the AI boom. Meta rallied on plans to sell AI chatbot subscriptions, while chip shares cooled after a strong prior session, showing investors remain selective within the AI trade.

Corporate Updates Show Mixed Sector Signals: Bank executives pointed to another strong quarter for trading revenue, even as bank stocks led broader market losses on the day. Boeing offered a more upbeat production and certification outlook, while American Airlines said travel demand remains firm despite higher fuel costs. Elsewhere, Zscaler sold off sharply on cautious guidance, Bath & Body Works jumped on better profit expectations, and Salesforce traded cautiously ahead of earnings.

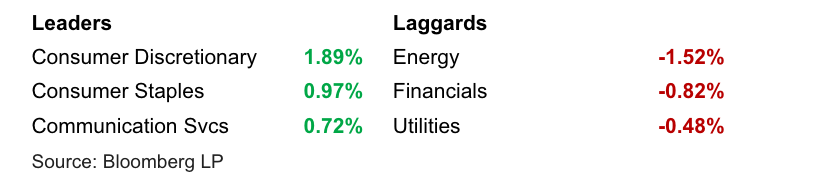

S&P 500 Sector Performance

Looking Ahead

Markets will remain highly sensitive to headlines on Iran, the Strait of Hormuz, and oil supply risks, since a durable reopening of energy flows would ease inflation pressure and support risk appetite. Investors will also watch whether AI-linked earnings can keep justifying elevated equity valuations, particularly as semiconductor momentum has become more uneven. Upcoming earnings and macro data will matter most if they shift expectations for profit growth, inflation, or the path of Treasury yields.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

%20Plan%20Document%20Aligned%20With%20How%20You%20Operate%20the%20Plan.png)

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119