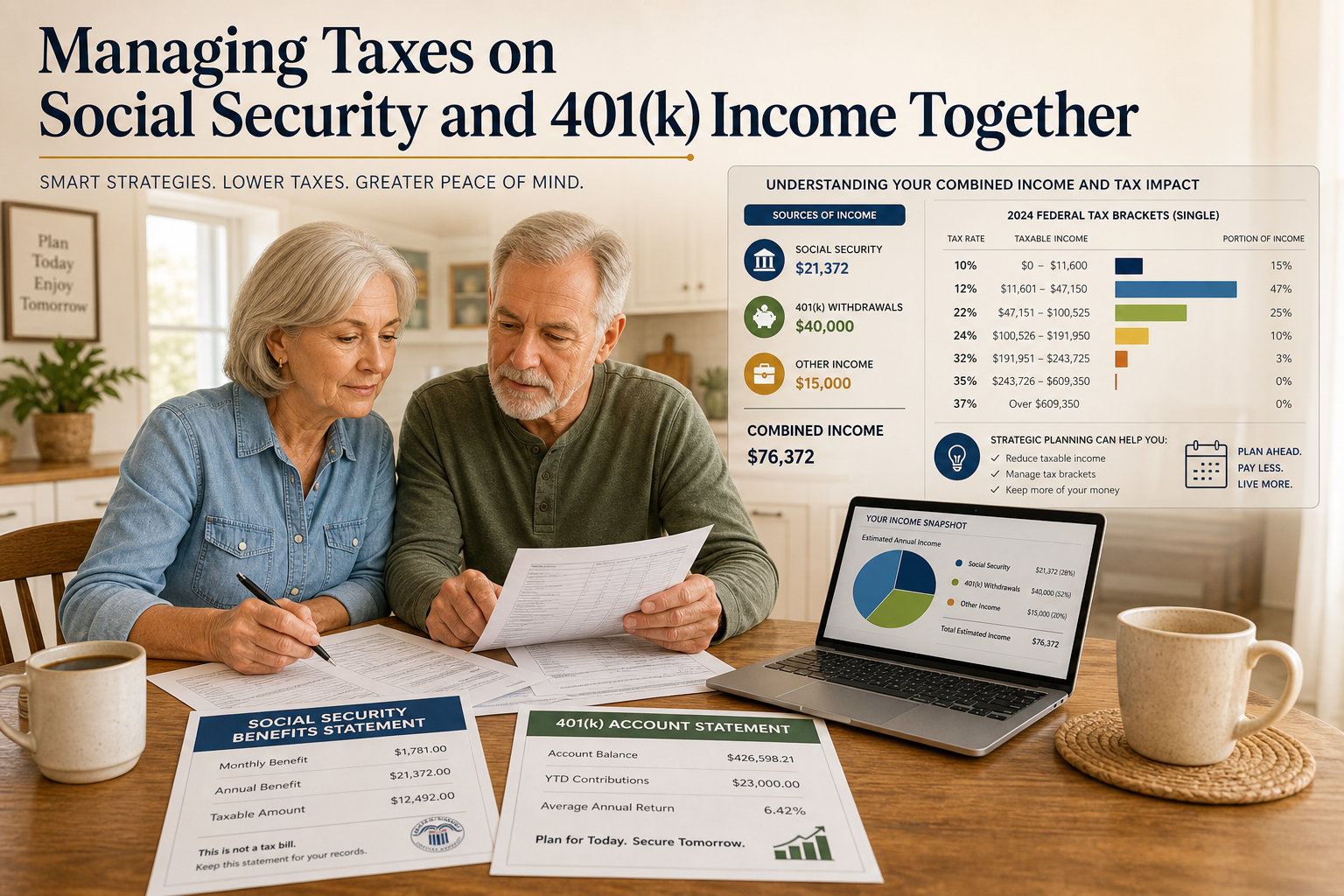

A 10-step 401(k) checkup helps ensure your 2026 retirement savings strategy aligns with your goals, plan rules, and current contribution limits. This guide is for general information and does not offer personalized investment, tax, or legal advice.

1. Confirm your 2026 contribution rate

Review your 401(k) contributions per paycheck and compare them to the 2026 limit. Experts recommend contributing enough to receive your full employer match and, if possible, targeting a long-term savings rate in the mid-teens as a percentage of your income.

2. Make sure you capture the full employer match

Understand your employer's match and ensure you contribute enough to receive the maximum each period. Otherwise, you may miss out on part of your compensation and potential growth.

3. Check how close you are to the annual limit

In 2026, most employees can contribute up to the mid-$20,000s to their 401(k), with higher limits for those eligible for catch-up contributions. If you plan to maximize contributions, confirm your payroll elections, including bonuses, do not exceed the limit or cause contributions to stop before year-end.

4. Review catch‑up contributions if you are 50+

If you are 50 or older, confirm you are using available catch-up contributions and review how new rules for higher earners and Roth catch-ups may affect your plan. Contact your HR team or plan administrator to verify plan features and enrollment procedures.

5. Revisit your investment mix and diversification

Review your investments to ensure diversification across asset classes and avoid overconcentration in any single investment, such as company stock. Align your investment mix with your goals and risk tolerance, and rebalance periodically to maintain your strategy.

6. Scrutinize plan and fund fees

Review your plan’s administrative costs and fund expense ratios, as fees can reduce your returns over time. When possible, select lower-cost funds within the same asset class that align with your strategy.

7. Consolidate old workplace plans where appropriate

Many people have old 401(k) accounts from previous employers, which can increase complexity and fees. Consider consolidating old accounts into your current plan or an IRA, but compare fees, investment options, protections, and withdrawal rules before making a decision.

8. Confirm beneficiaries and key contact information

Major life events such as marriage, divorce, the birth of a child, or a loss can make beneficiary designations outdated. Review your 401(k) paperwork and online account annually to ensure your savings are directed as intended and your contact information is current.

9. Check for required notices and statements

Ensure you receive and review your plan’s disclosures, account statements, plan descriptions, and notices about changes or fees. These documents explain how your plan operates, its costs, and your available options.

10. Align your 401(k) with your overall financial plan

Review whether your 401(k) aligns with your overall financial goals, including emergency savings, debt repayment, college funding, and other retirement accounts. An annual review can help you determine if you should adjust contributions, change investments, or consult a financial professional for personalized advice.

Disclosure

This article is provided for general educational and informational purposes only and does not constitute investment, legal, tax, or accounting advice. It is not an offer, solicitation, recommendation, or endorsement of any security, investment strategy, employer plan, or service, and should not be relied upon as a primary basis for any investment or retirement decision.

Investing through a 401(k) or other retirement plan involves risk, including possible loss of principal, and there is no guarantee that any checklist or strategy described will achieve any particular outcome. Contribution limits, catch‑up rules, tax laws, and plan features are set by the IRS, plan sponsors, and applicable law and may change over time; you should review your official plan documents and current IRS and Department of Labor guidance and consult a qualified investment, tax, or legal professional about your specific circumstances.

Any contribution levels, account balances, or allocation examples mentioned here are hypothetical and for illustration only; they do not reflect the performance of any actual account, security, or plan and do not guarantee future results.

Sources

- FINRA – Importance of an annual 401(k) checkup: https://www.finra.org/investors/insights/annual-401k-checkup

- IFA – 2026 annual retirement savings and tax guide: https://www.ifa.com/articles/annual_retirement_savings_guide_cheat_sheet_2026

- Principal – Five annual steps to build retirement confidence: https://www.principal.com/individuals/learn/5-step-yearly-financial-checkup-help-you-retire

- Savant Wealth – Big changes ahead for 401(k) plans in 2026: https://savantwealth.com/savant-views-news/article/big-changes-ahead-for-401k-plans-in-2026/

- The Statement – 401(k) catch‑up contribution changes for 2026: https://thestatement.bokf.com/articles/2025/11/401k-changes-to-know-for-2026

- Bankrate – 401(k) contribution limits for 2026: https://www.bankrate.com/retirement/401k-contributions/

- Guideline – End‑of‑year 401(k) checkup for plan sponsors: https://www.guideline.com/education/articles/an-end-of-year-checkup-8-tips-for-401-k-plan-sponsors

- Retirement Clearinghouse – Definitive guide to 401(k) consolidation: https://rch1.com/401k-consolidation

- Charles Schwab – When and how to combine 401(k)s and other retirement accounts: https://www.schwab.com/ira/rollover-ira/combining-401ks

- NerdWallet – 401(k) rollovers overview: https://www.nerdwallet.com/retirement/learn/401k-rollover-ira-guide

- John Hancock – Basics of the 401(k) coverage test (plan compliance timing): https://retirement.johnhancock.com/us/en/viewpoints/erisa--plan-design/the-basics-of-the-401-k--coverage-test

- Northwestern Mutual – New‑year financial checklist for 2026: https://www.northwesternmutual.com/life-and-money/new-year-financial-checklist/

- FINRA – Benefits checkup and reviewing available programs: https://www.finra.org/investors/military/retirement/benefits-checkup

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119