Avoiding the most common 401(k) mistakes changes as you move through your 30s, 40s, 50s, and 60s. No matter your age, the key is to keep your savings on track and your strategy balanced for your stage of life. The ideas below are meant to educate and inform, but they aren’t personalized investment, tax, or legal advice.

In your 30s: delaying and under‑risking

If you’re in your 30s, it’s easy to put off saving for retirement, contribute only the minimum, or play it too safe with your investments. Many people also miss out on their employer match, unknowingly leaving part of their compensation on the table.

To avoid these traps, it’s smart to enroll as soon as you can, at least contribute enough to get the full match, and pick a mix of investments with enough stocks for long-term growth—not just cash or stable-value funds. Having an emergency fund outside your 401(k) can also save you from dipping into retirement savings when life throws you a curveball.

In your 40s: crowding out retirement

In your 40s, it’s common to let college costs, mortgage payments, or lifestyle upgrades eat into your retirement contributions. Debt can pile up, and it’s easy to lose track of your investments—sometimes ending up too aggressive, too conservative, or with too much in one stock (often your employer’s).

You can stay on track by making retirement contributions a non-negotiable part of your budget, bumping up your savings rate every so often, and making sure your investments aren’t all in one basket. Keeping an eye on debt and avoiding lifestyle creep can also help free up cash for your 401(k), even as you juggle other goals.

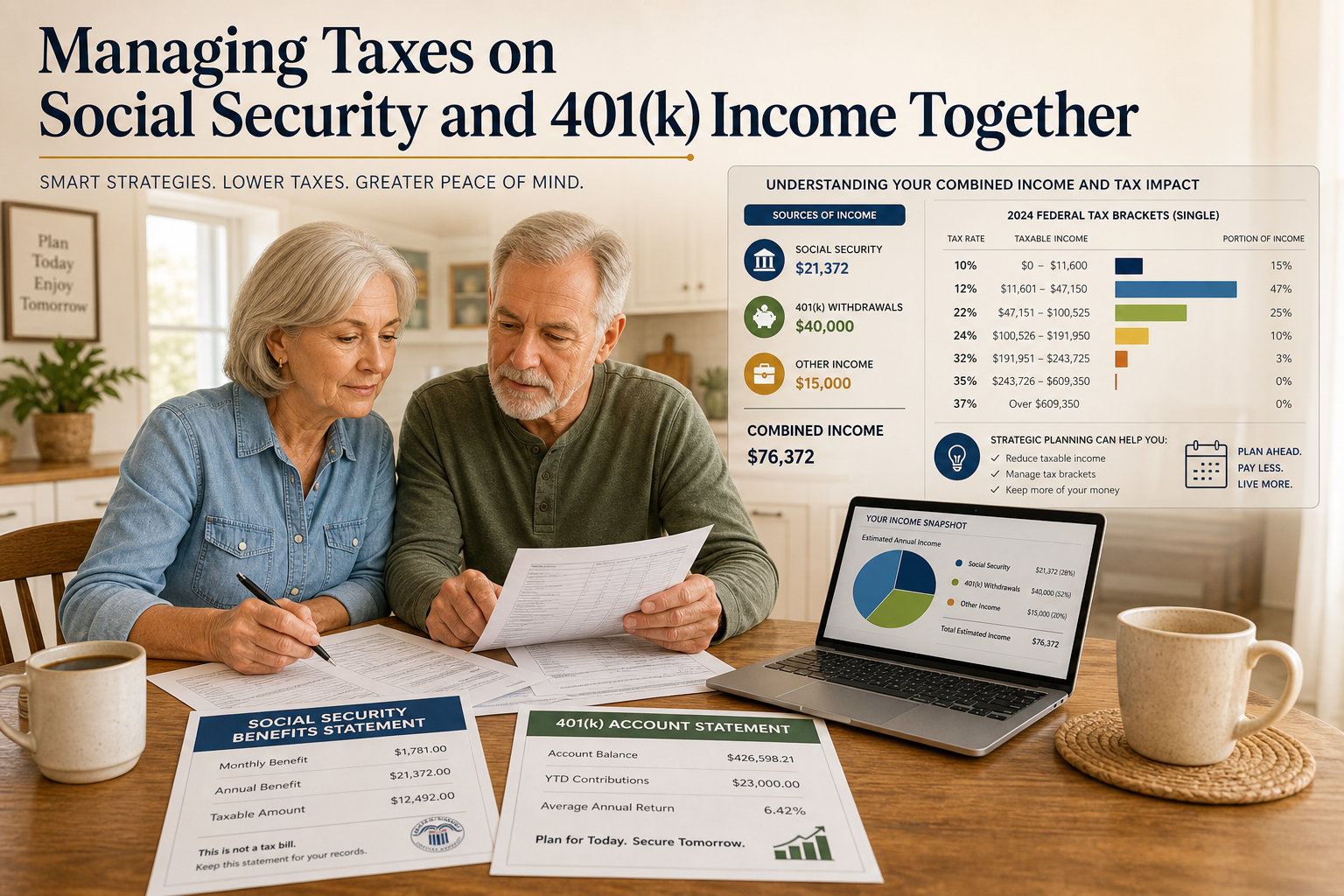

In your 50s: raiding and mis‑allocating

In your 50s, it can be tempting to dip into your 401(k) with loans or early withdrawals, but these moves often mean taxes, penalties, and less money for retirement. Others may lean too heavily on company stock or take big investment risks just as retirement is getting close, leaving their savings exposed to unnecessary ups and downs.

To help keep your nest egg safe, try to avoid early withdrawals, use catch-up contributions if you’re eligible, and slowly shift your investments to match your retirement timeline. Rebalancing once in a while and making sure no single stock takes over your portfolio can go a long way in managing risk.

In your 60s: poor coordination with retirement

In your 60s, expensive mistakes might include cashing out your 401(k) when you change jobs instead of rolling it over, underestimating how long your savings will need to last, or co-signing debts that put a strain on your retirement resources. Some people also claim Social Security early without weighing the long-term trade-offs, or keep investments that are too risky or too cautious for their time horizon.

To steer clear of these pitfalls, it’s helpful to make a written plan for how you’ll draw income in retirement—coordinating your 401(k) withdrawals, Social Security timing, and healthcare expenses. Think carefully before using retirement funds to help others, and review fees, required minimum distributions, and rollover options with a qualified professional to avoid costly surprises.

Disclosure

This article is provided for general educational and informational purposes only and does not constitute investment, legal, tax, or accounting advice. It is not an offer, solicitation, recommendation, or endorsement of any security, investment strategy, employer plan, or service, and should not be relied upon as a primary basis for any investment or retirement decision.

Investing through a 401(k) or other retirement plan involves risk, including possible loss of principal, and there is no guarantee that any strategy described will achieve any particular outcome. Contribution limits, distribution rules, tax laws, and plan features are established by the IRS, plan sponsors, and applicable law and may change over time; you should review your official plan documents and current IRS and Department of Labor guidance and consult a qualified investment, tax, or legal professional about your specific circumstances.

Any examples of mistakes, contribution levels, savings benchmarks, or asset allocations in this article are based on third‑party educational sources and are hypothetical; they do not reflect or predict the performance of any actual account, security, or plan.

Sources

- Discover – Biggest retirement savings mistakes to avoid: https://www.discover.com/online-banking/banking-topics/retirement-savings-mistakes/

- “401(k) decisions by age decade” (30s–60s): https://www.linkedin.com/pulse/401k-decisions-age-decade-20s-30s-40s-50s-60s-donaldson-cfp-ceps

- Dow Janes – Money mistakes to avoid for every age: https://www.dowjanes.com/blog/money-mistakes-to-avoid

- Kramer Wealth – Financial mistakes to avoid in your 30s, 40s, and 50s: https://www.kramerwealth.com/financial-mistakes-to-avoid-in-your-30s-40s-and-50s/

- WMAR – Money Matters: top mistakes every decade makes: https://www.wmar2news.com/local/money-matters-top-mistakes-every-decade-makes

- Brighton Jones – 401(k) mistakes and how to avoid them: https://www.brightonjones.com/blog/401k-mistakes-no-nos-to-avoid/

- Fidelity – Average retirement savings by age: https://www.fidelity.com/learning-center/personal-finance/average-retirement-savings

- Fidelity – Retirement savings mistakes young people make: https://www.fidelity.com/learning-center/smart-money/common-retirement-mistakes

- Bankrate – Biggest 401(k) mistakes to avoid: https://www.bankrate.com/retirement/401k-mistakes-to-avoid/

- 401(k) Specialist – Commonly misunderstood retirement “rules of thumb”: https://401kspecialistmag.com/6-retirement-rules-of-thumb-most-americans-get-wrong-slideshow/

- MyLife/ADP – Biggest retirement planning mistakes at every age: https://mylife.adp.com/the-biggest-retirement-planning-mistakes-at-every-age-2/

- Vision Retirement – Biggest 401(k) mistakes to avoid: https://www.visionretirement.com/articles/employee-benefits/biggest-401k-mistakes

- Consolidated Credit – Retirement planning mistakes to avoid at every age: https://www.consolidatedcredit.org/financial-news/retirement-planning-mistakes-to-avoid-at-every-age/

- BECU – Four common 401(k) mistakes to avoid: https://www.becu.org/articles/common-401k-mistakes-to-avoid

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119