For many people saving for retirement, the "cash-like" part of a 401(k) plan seems straightforward. But while stable value funds, money market funds, and short-term bond funds are all considered conservative choices, they can act differently when the market, interest rates, or liquidity conditions shift.

All three options are less volatile than stocks, but they're not the same. When choosing between them, consider three things: How safe is your principal? How quickly can you access your money? And how much do returns change when interest rates move?

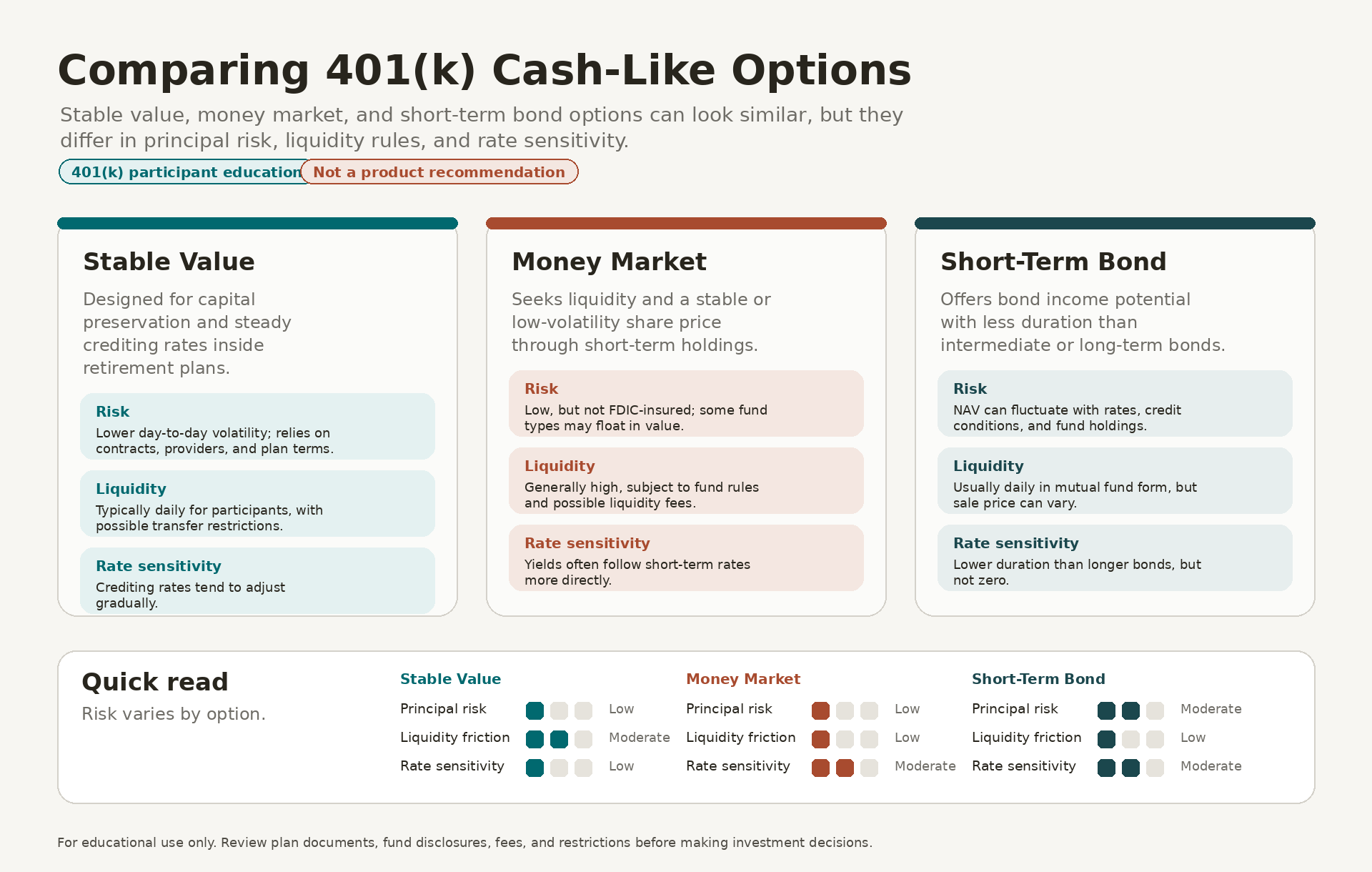

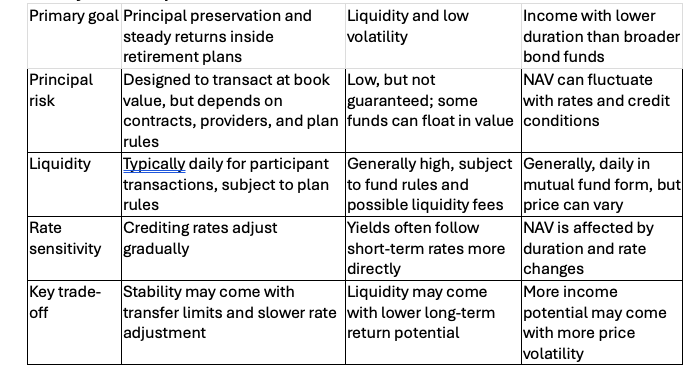

Stable Value Funds

Stable value funds are usually found in tax-advantaged retirement plans like 401(k)s, 403(b)s, and some 529s. They're designed to protect your money, offer steady returns, and smooth out some of the bond market's ups and downs. These funds invest in a mix of high-quality bonds and add insurance contracts, so you can move money in and out at "book value" instead of having to worry about daily price swings.

Stable value funds try to keep your balance steady from day to day, but they're not completely risk-free. Risks include the financial strength of the insurance company backing the fund, the quality of the bonds inside, inflation, and certain plan rules that might limit how or when you can move your money.

Liquidity is generally good—you can usually take money out as your plan allows. But some stable value funds may limit how quickly you can transfer money to similar options, like money market or short-term bond funds, to prevent quick switches that could hurt the fund.

Interest rates don't usually affect stable value funds right away. The fund's crediting rate changes slowly, which helps keep returns steady. But if short-term rates rise quickly, these funds may not keep up as fast as other cash options.

Money Market Funds

Money market funds invest in short-term, high-quality investments. Their main goal is to provide easy access to cash and keep your balance steady. Most government and retail money market funds try to keep their share price at $1.00, while some institutional funds can fluctuate a bit above or below that mark.

Money market funds are very liquid, but they're not the same as a bank account and they're not insured by the FDIC. You could lose money, and in rare cases, the fund may charge a fee or limit withdrawals if markets are stressed.

Money market funds respond quickly to changes in short-term interest rates. When rates go up, the yields on these funds usually rise fast; when rates drop, yields go down just as quickly.

Short-Term Bond Funds

Short-term bond funds buy bonds that mature sooner than those in longer-term funds. They might pay more interest than money market funds, but their prices can go up and down as the bond market changes.

The key idea here is "duration"—a measure of how much a bond fund's value moves when interest rates change. Funds with higher duration are more sensitive to rate swings.

Short-term bond funds are less sensitive to interest rate changes than long-term funds, but "short-term" doesn't mean "no risk." These funds can still lose value from things like credit problems, inflation, or other risks listed in their prospectus.

Side-by-Side Comparison

How to Think About the Choice

Stable value funds may be a good fit if you want to protect your principal and see steady returns. Money market funds make sense if you need quick access to your cash and want returns that move with short-term rates. Short-term bond funds might work if you're comfortable with some price swings in exchange for the chance at higher income.

The best option depends on your timeline, comfort with risk, need for access to your money, and what's available in your plan. Be sure to read each fund's fact sheet or prospectus before you decide.

Disclosure

This article is only for educational purposes and should not be considered investment, tax or legal advice. The information provided does not constitute a recommendation to buy, sell or hold a particular investment. All investing involves risk, including the possibility of loss of principal. Stable value funds, money market funds, and short-term bond funds have different risks, fees, liquidity features, and restrictions. Participants should review plan documents, fund disclosures, and confer with a qualified financial professional before making investment decisions.

Sources

- SEC Investor.gov: Money Market Funds Investor Bulletin

- U.S. Department of Labor: Advisory Council Report on Stable Value Funds and Retirement Securityhttps://www.dol.gov/agencies/ebsa/about-ebsa/about-us/erisa-advisory-council/2009-stable-value-funds-and-retirement-security-in-the-current-economic-conditions

- FINRA: Brush Up on Bonds, Interest Rate Changes and Durationhttps://www.finra.org/investors/insights/bonds-interest-rate-changes-duration

- Charles Schwab: Stable Value Funds 101https://www.schwab.com/learn/story/stable-value-funds-101-beginners-guide

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119