Deciding between pre-tax and Roth 401(k) contributions isn’t just about retirement—it’s also about your tax bracket.

Both options help you save for retirement, but they handle taxes differently. With a traditional pre-tax 401(k), you lower your taxable income now and pay taxes later when you withdraw the money. With a Roth 401(k), you pay taxes on your contributions up front, but qualified distributions in retirement can be tax-free, according to the IRS.

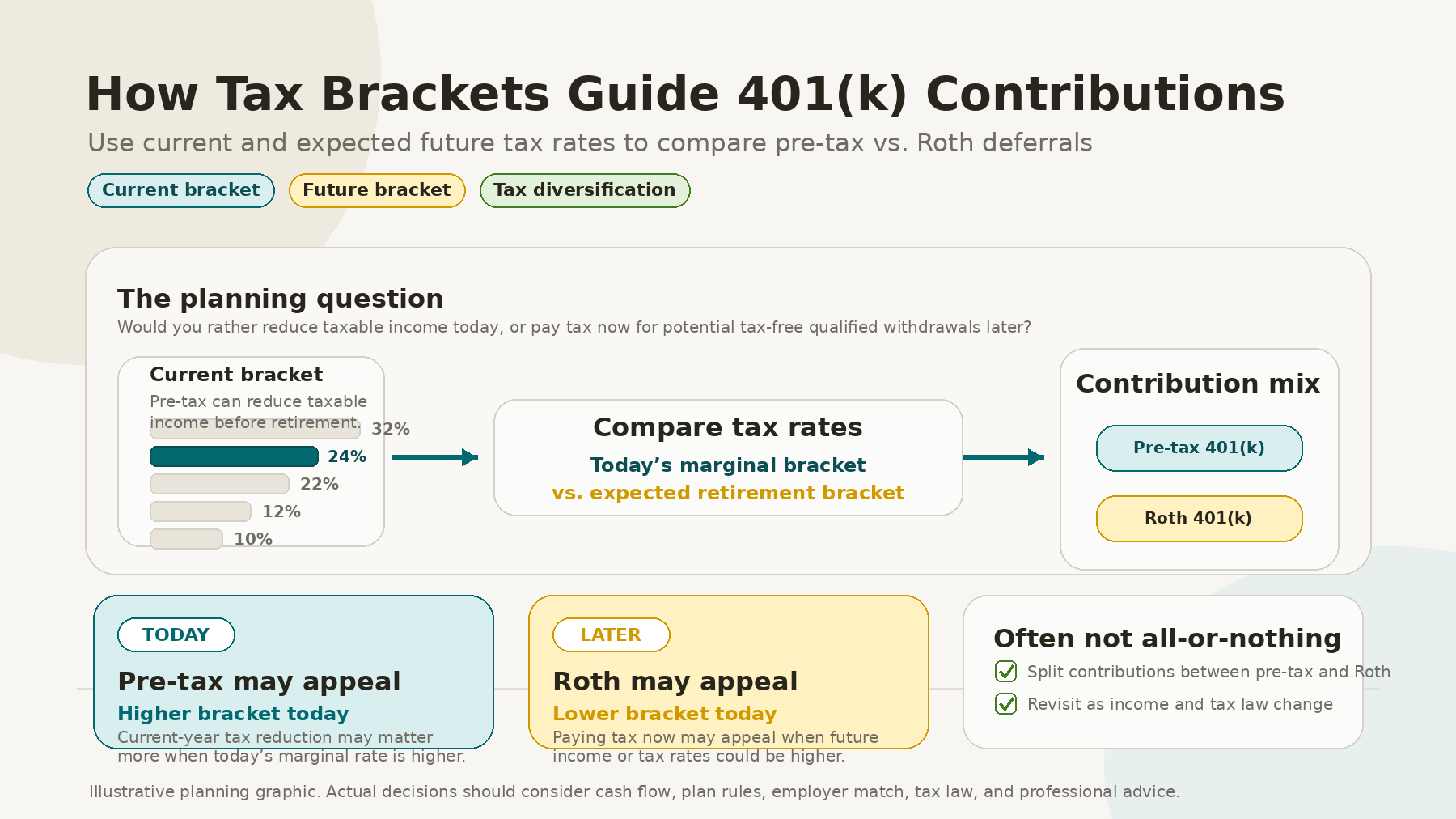

Because of this difference, your current tax bracket—and what you expect it to be in the future—plays a big role in your decision.

Start With the Basic Tradeoff

A pre-tax 401(k) might make more sense if you’re in a high tax bracket now and expect to be in a lower bracket when you retire. The immediate tax deduction is valuable because every dollar you save avoids taxes at your current rate.

On the other hand, a Roth 401(k) could be better if you’re in a lower tax bracket now and think you’ll be in the same or a higher bracket in the future. Paying taxes today may be worth it if it means tax-free withdrawals later.

The decision is not always all-or-nothing. The IRS says participants may contribute to both a designated Roth account and a traditional pre-tax account in the same year in any proportion they choose, as long as combined contributions stay within the annual limit: IRS-designated Roth accounts.

Why Marginal Brackets Matter

Investors often hear, “I’m in the 24% tax bracket,” but that does not mean all income is taxed at 24%. The U.S. federal income tax system uses marginal brackets, which means different portions of income are taxed at different rates.

For 2026, the IRS lists federal marginal rates of 10%, 12%, 22%, 24%, 32%, 35%, and 37%, with the 24% bracket beginning above $105,700 for single filers and above $211,400 for married couples filing jointly: IRS 2026 inflation adjustments.

This matters because a pre-tax 401(k) contribution generally reduces income from the top bracket first. For example, if an investor is near the top of the 24% bracket, additional pre-tax deferrals may reduce income subject to the 24% tax rate. If those deferrals push taxable income into a lower bracket, the tax benefit of the next dollar contributed may be lower.

When Pre-Tax Contributions May Be More Appealing

Pre-tax 401(k) contributions may deserve more attention when:

Current income is unusually high.

The investor is in a higher marginal tax bracket.

The investor expects lower taxable income in retirement.

The household needs current-year tax relief.

The investor lives in a high-tax state and expects to move to a lower-tax state later.

There is uncertainty about cash flow, and the current tax reduction is valuable.

This can be especially relevant for investors in peak earning years. If current income is high because of bonuses, business income, equity compensation, or a dual-income household, pre-tax deferrals may help reduce current taxable income.

For 2026, the IRS says the employee contribution limit for 401(k), 403(b), most governmental 457 plans, and the federal Thrift Savings Plan is $24,500: IRS 2026 retirement limits. The IRS also says the general catch-up contribution limit for participants age 50 and older is $8,000 in 2026, with a higher catch-up limit of $11,250 for eligible participants ages 60 through 63: IRS 2026 retirement limits.

When Roth Contributions May Be More Appealing

Roth 401(k) contributions may deserve more attention when:

Current income is temporarily low.

The investor is early in their career.

The investor expects income to rise over time.

The investor wants more tax diversification in retirement.

The investor already has significant pre-tax retirement assets.

The investor values the potential for tax-free qualified withdrawals later.

Roth contributions can be useful when today’s tax costs are manageable. For example, a younger investor in a lower bracket may decide that paying tax now is reasonable if future income and future tax rates could be higher.

The IRS says designated Roth contributions are included in gross income in the year contributed, but eligible distributions from the account, including earnings, are generally tax-free: IRS-designated Roth accounts.

Consider a Split Strategy

Many investors do not need to choose between pre-tax and Roth. A split strategy may allow an investor to receive some current tax benefit while also building future tax-free retirement assets.

For example, an investor might direct 70% of contributions to pre-tax and 30% to Roth. Another investor might use Roth contributions early in the year and switch to pre-tax contributions later if taxable income turns out to be higher than expected.

A split approach can be useful when future tax rates are uncertain. It can also help create retirement flexibility, as future withdrawals may come from different tax brackets.

Watch Bracket Thresholds

Tax brackets can also be useful for year-end planning. If an investor is close to the next bracket, additional pre-tax 401(k) contributions may reduce taxable income enough to keep taxable income within a lower bracket.

For 2026, the standard deduction is $16,100 for single filers, $32,200 for married couples filing jointly, and $24,150 for heads of household, according to the IRS: IRS 2026 inflation adjustments. Because deductions affect taxable income, investors should review brackets using estimated taxable income rather than gross salary alone.

Do Not Ignore Employer Match

The pre-tax versus Roth decision should not distract from the importance of the employer match. If a plan offers a match, contributing enough to receive it is often a high priority.

Employer contributions are typically made under plan rules and may not follow the employee’s Roth or pre-tax election. Investors should review their plan documents or speak with their benefits administrator to understand how matching contributions are treated.

The Bottom Line

Tax brackets can help investors make more thoughtful 401(k) contribution decisions. A higher current bracket may increase the appeal of pre-tax deferrals. A lower current bracket may increase the appeal of Roth deferrals.

The best answer depends on more than today’s tax rate. Investors should also consider future income, retirement timing, state taxes, employer match, cash flow, estate goals, and the value of tax diversification.

For numerous households, the right strategy is not permanent. It may change as income, tax law, family circumstances, and retirement plans evolve.

Sources

IRS, “Retirement Plans FAQs on Designated Roth Accounts”

https://www.irs.gov/retirement-plans/retirement-plans-faqs-on-designated-roth-accounts

IRS, “401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500”

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

IRS, “IRS releases tax inflation adjustments for tax year 2026”

https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

IRS, “Roth Comparison Chart”

https://www.irs.gov/retirement-plans/roth-comparison-chart

Disclosure

This material is for informational and educational purposes only and should not be considered personalized investment, tax, legal, or financial planning advice. Tax laws, contribution limits, retirement plan rules, and individual circumstances may change. Investors should consult their financial advisor, tax professional, benefits administrator, or legal advisor before making decisions about pre-tax 401(k) contributions, Roth 401(k) contributions, Roth conversions, withholding, or retirement income planning. Investing involves risk, including the possible loss of principal, and no strategy can guarantee a profit or protect against loss.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119