Owing taxes can be stressful. When you have a federal or state tax bill due, it’s natural to want to free up cash fast. Many people consider stopping their retirement contributions until the tax is paid off.

In some cases, that might be necessary—but it shouldn’t be your default response.

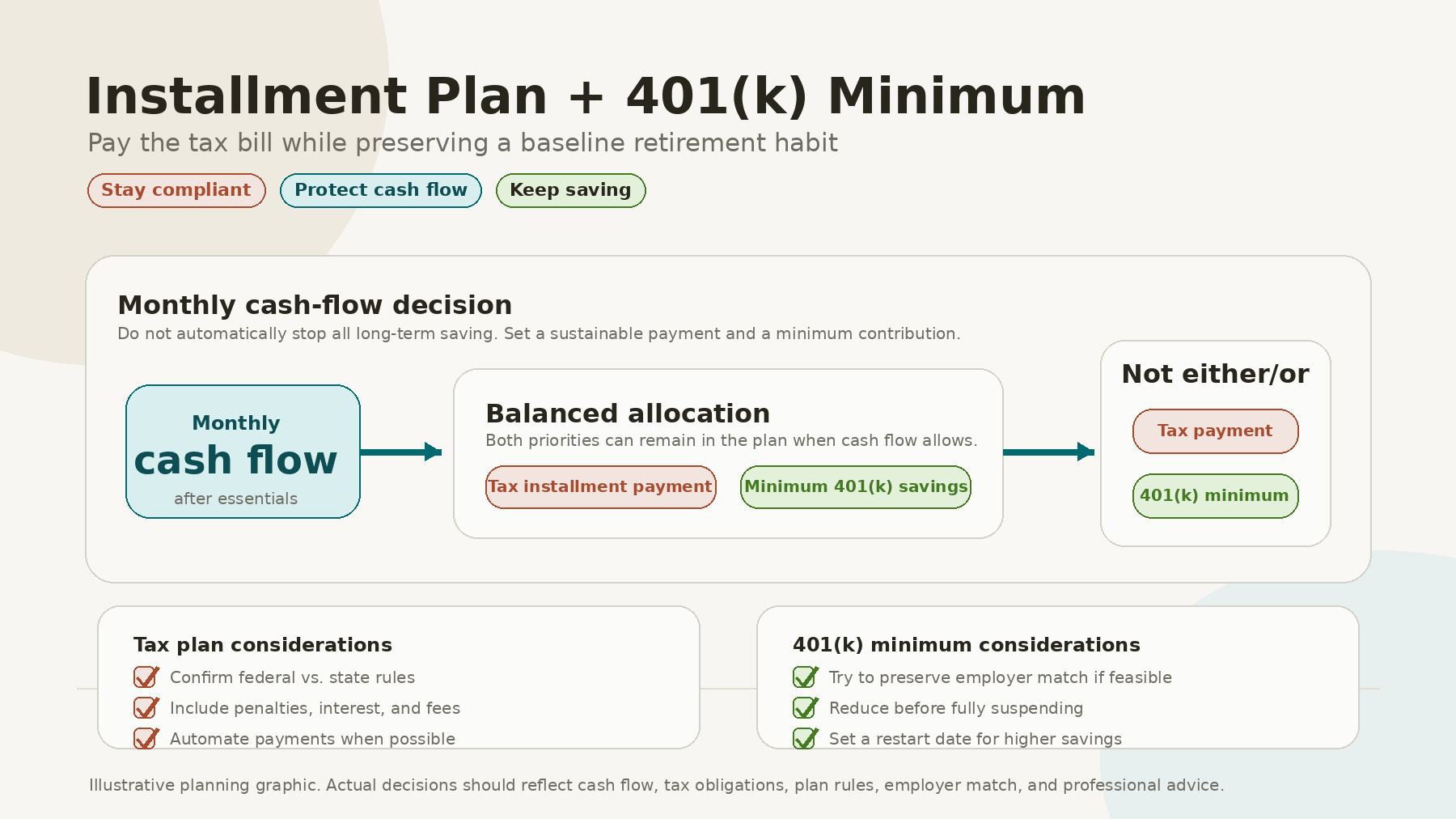

If you can handle the monthly payments, an IRS or state installment plan can help you tackle your tax bill while still maintaining some long-range savings. The key is to create a cash-flow plan that weighs three things: staying on the tax authority’s good side, avoiding penalties or missed payments, and, when possible, keeping your retirement savings on track.

Start With the Tax Obligation

The first step is to understand the amount owed, the due date, and whether the balance is federal, state, or both. The IRS says a payment plan is an agreement to pay taxes owed over an extended period, and taxpayers should request one if they believe they can pay the tax in full within that timeframe.

For federal taxes, the IRS typically offers two types of payment plans: short-term and long-term (installment agreements). You may qualify for a long-term plan if you owe $50,000 or less in combined tax, penalties, and interest and have filed all required returns. For a short-term plan, the limit is $100,000.

An installment plan doesn’t make your tax bill disappear—it just gives you more time to pay it off. Keep in mind, penalties and interest keep adding up until the debt is gone.

Why State Plans Need Separate Attention

State tax bills are a separate issue from federal ones. Every state has its own rules, systems, fees, and eligibility requirements.

For example, California’s Franchise Tax Board says individuals may be eligible for a personal installment agreement if the amount due does not exceed $25,000, the balance can be paid in 60 months or less, and the taxpayer has filed income tax returns for the past five years. That is only one state example, not a national rule.

The Federation of Tax Administrators maintains links to state tax agencies, which can help taxpayers locate the appropriate state revenue department. Investors with both federal and state balances should review each obligation separately and avoid assuming that an IRS payment plan also resolves a state tax issue.

Fit the Monthly Payment Into Your Budget

Before setting up a payment plan, figure out how the monthly payment will fit into your regular budget. The IRS asks you to choose how much you’ll pay each month and on which day (between the 1st and the 28th) you'll make the payment.

A practical cash-flow review should include:

Regular income

Mortgage or rent

Utilities and insurance

Minimum debt payments

Food, transportation, and medical costs

Emergency savings needs

Required tax installment payment

Minimum retirement contribution goal

Make sure your monthly payment is realistic. A payment plan that looks good on paper but leads to overdrafts, missed bills, or more credit card debt isn’t really solving the problem.

Do Not Automatically Suspend All 401(k) Contributions.

If money is tight, it’s okay to temporarily lower your retirement contributions. But there’s a big difference between cutting back and stopping your long-term investments altogether.

A 401(k) contribution can fulfill several functions. It may help investors build retirement assets, reduce current taxable income when made pre-tax, and qualify for an employer matching contribution if the plan offers one. The IRS says the 2026 elective deferral limit for employees participating in 401(k), 403(b), most governmental 457 plans, and the federal Thrift Savings Plan is $24,500.

During a tax repayment period, your goal isn’t to maximize your retirement contributions—it’s to keep your long-term plan intact. For many people, that means contributing enough to get your employer’s match, if your plan offers one and your budget allows.

Pausing all 401(k) savings might free up cash now, but it can break your savings habit. It’s often easier to keep making smaller contributions than to stop and try to restart later.

A Practical “Minimum Savings” Approach

One way to approach this is to set some short-term priorities.

First, stay current on required tax filings and required installment payments.

Second, sustain essential household cash flow.

Third, protect emergency savings from being fully depleted.

Fourth, continue minimum 401(k) contributions if the budget allows.

Fifth, resume higher retirement savings after the tax balance is repaid.

This way, you stay on top of tax obligations while making sure you don’t abandon your retirement goals without good reason.

For example, if you usually put 10% of your paycheck into your 401(k), you might temporarily drop it to 4% or 5% while paying the IRS. If that’s enough to get the employer match, you’ll still receive some of that benefit while freeing up cash for your tax payments.

That is not a universal recommendation. It is a planning framework. The right number depends on income, debt, tax balance, employer match formula, emergency reserves, age, and retirement readiness.

Consider the Cost of the Plan

Installment plans can be useful, but they are not free from tradeoffs. The IRS states that setup fees may apply to approved payment plans, depending on the type of plan and payment method. The IRS also states that direct debit installment agreements generally have lower setup fees than some other long-term payment methods.

Direct debit may also reduce the risk of missing a payment. The IRS says direct debit installment agreements and payroll deduction installment agreements can help taxpayers make timely payments automatically and reduce the possibility of default.

Investors should compare the cost of the installment plan with the opportunity cost of stopping retirement contributions. In some cases, paying the tax debt faster may be the priority. In others, a moderate approach may make more sense.

Stay Current Going Forward

An installment plan is more than just the old balance. It also requires staying up to date on new tax obligations.

The IRS says taxpayers on a payment plan should file all required tax returns on time and pay all taxes in full and on time, and should contact the IRS to change a current agreement if they cannot do so. The IRS also says future refunds will be applied to the tax debt until it is paid in full, and taxpayers should continue making scheduled payments even if a refund is applied to the balance.

This is an important point. If withholding or estimated tax payments are too low during the repayment period, a taxpayer may create a new tax balance while still paying off the old one. That can make the problem harder to solve.

Investors should consider reviewing their withholding, estimated payments, or business tax planning with a tax professional. The IRS Tax Withholding Estimator can help taxpayers see how withholding affects their refund, paycheck, or tax due (IRS Tax Withholding Estimator).

When Reducing 401(k) Contributions May Be Appropriate.

There are circumstances where reducing or pausing 401(k) contributions may be necessary. Examples may include:

The installment payment cannot be made without reducing contributions.

The household has no emergency reserves.

The taxpayer is relying on credit cards for basic expenses.

The tax authority requires a larger monthly payment than expected.

The investor is facing wage garnishment, levy, or other collection action.

The household needs to bring its withholding or estimated tax payments up to date.

In those cases, preserving liquidity and remaining compliant may take priority. But even then, the change should be intentional, documented, and revisited on a specific schedule.

Create a Restart Date

If contributions are reduced, investors should decide in advance when they will review the decision. A good practice is to set a restart trigger.

Examples include:

When the tax balance is paid off

When the installment payment drops below a certain level

After six months of on-time payments

At the next annual benefits enrollment period

When emergency savings reach a target amount

Without a restart date, a temporary reduction can become an extended savings gap. A calendar reminder, along with an annual financial review, can help ensure the contribution rate is revisited.

Coordinate With an Advisor and Tax Professional

This is an area where tax planning and financial planning overlap. The tax professional can help evaluate filing obligations, payment plan eligibility, penalties, interest, withholding, and estimated payments. The financial advisor can help evaluate cash flow, emergency reserves, retirement savings, debt repayment, and investment priorities.

The decision is rarely as simple as “pay the IRS first” or “never reduce retirement savings.” The better question is: what payment plan allows the taxpayer to become compliant while doing the least damage to long-run financial progress?

The Bottom Line

An IRS or state installment plan can be a useful tool when a tax balance cannot be paid immediately. But setting up a payment plan should be part of a wider financial decision, not a panic response.

Investors should understand the payment terms, penalties, interest, fees, and filing requirements. They should also evaluate whether they can maintain a minimum 401(k) contribution, especially if an employer match is available and household cash flow allows it.

The objective is balance: resolve the tax obligation, avoid default, maintain current tax compliance, and, where possible, preserve the momentum of extended savings.

Source URLs

IRS, “Payment plans, installment agreements”

https://www.irs.gov/payments/payment-plans-installment-agreements

IRS, “Online payment agreement application”

https://www.irs.gov/payments/online-payment-agreement-application

IRS, “Topic No. 202, Tax payment options”

https://www.irs.gov/taxtopics/tc202

IRS, “Instructions for Form 9465, Installment Agreement Request”

https://www.irs.gov/instructions/i9465

IRS, “401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500”

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

IRS, “Tax Withholding Estimator”

https://www.irs.gov/individuals/tax-withholding-estimator

California Franchise Tax Board, “Payment plans, installment agreement”

https://www.ftb.ca.gov/pay/payment-plans/index.asp

Federation of Tax Administrators, “FTA Members”

https://taxadmin.org/fta-members/

Disclosure

This material is for informational and educational purposes only and should not be considered personalized investment, tax, legal, or financial planning advice. Tax laws, IRS rules, state tax rules, installment agreement requirements, interest, penalties, fees, retirement plan rules, and contribution limits may change. Any examples are hypothetical and are not recommendations for any specific individual or household. Investors should consult their financial advisor, tax professional, benefits administrator, or legal advisor before entering into a payment plan, changing tax withholding, adjusting estimated tax payments, changing 401(k) contributions, or making other financial planning decisions. Investing involves risk, including the possible loss of principal, and no strategy can guarantee a profit or protect against loss.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119