Markets were mixed Friday, closing out a choppy week as rising Treasury yields weighed on sentiment and speculation mounted around the next Federal Reserve Chair. President Trump's comments signaling hesitation on nominating Kevin Hassett, a perceived dove, triggered a sharp move in rates, lifting the 10-year Treasury yield to a four-month high. Stocks held up relatively well, though major indexes ended the week slightly lower. Small-cap equities extended their strong 2026 outperformance, fueled by optimism around domestic growth and rate sensitivity. Chip stocks outperformed again, but gains were offset by weakness in utilities and large-cap defensives.

Key Headlines & Market Movers:

- Fed Chair Watch: Trump Hints Shift, Bonds Sell Off: Markets reassessed Fed policy expectations after President Trump downplayed the likelihood of appointing Kevin Hassett as the next Fed Chair. Hassett, viewed as dovish and aligned with Trump’s push for rate cuts, was seen as a front-runner. Trump's apparent pivot places Kevin Warsh, a more hawkish former Fed Governor, into pole position. While analysts suggest Warsh would still support near-term easing due to supply-side optimism, he could pivot hawkishly if inflation reaccelerates. The result: Treasuries fell, with 10-year yields jumping six basis points to 4.22%, as rate cut odds for 2026 were modestly dialed back.

Small-Caps Lead the Way Again: The Russell 2000 outperformed the S&P 500 for an 11th straight session, extending a notable early-year rotation into value and domestically focused stocks. Analysts are increasingly convinced that this move may have staying power. The outperformance reflects improving economic momentum, expectations for continued rate relief, and a broadening market rally beyond megacap tech. Historically, strong small-cap starts like this have often translated into full-year leadership, particularly when driven by fundamentals rather than speculative excess.

- Tech Gains Mask Broader Market Stagnation: Semiconductor stocks rallied again, led by Micron’s 8% surge after insider buying boosted investor confidence. However, the broader tech space was mixed, with the “Magnificent Seven” slipping slightly and indexes treading water. The S&P 500 and Nasdaq both ended little changed Friday, while the Dow dipped 0.2%. Traders pointed to pre-holiday positioning and Fed uncertainty as reasons for the market’s pause, even amid strong macro data and a positive earnings backdrop.

Earnings Kick Off - Regional Bank Divergence: Early Q4 results from regional banks were mixed. PNC Financial beat expectations thanks to strong middle-market dealmaking, sending shares up 4%. Regions Financial missed on both earnings and loan growth, guiding to lower net interest income in Q1; its shares fell 3%. The divergence highlights the uneven landscape for regional lenders navigating a flatter curve, modest credit pressure, and varying exposure to rate-sensitive sectors.

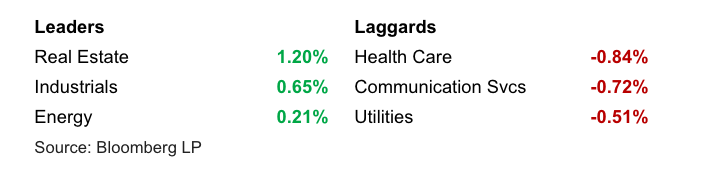

S&P 500 Sector Performance

Looking Ahead

Markets head into the shortened holiday week with Fed policy and political influence top of mind. The next major catalysts include more Q4 earnings, which will test the resilience of the current rally, especially if megacap tech and AI-linked names start to lose momentum. Bond markets remain vulnerable to policy headlines, particularly around Fed leadership, while small-cap strength will be closely watched as a barometer for broader economic confidence. With inflation under control and economic data improving, the backdrop remains supportive, but rising yields and political uncertainty could introduce near-term chop.

Disclaimer

Duncan Williams Asset Management is an SEC registered investment adviser. SEC registration does not constitute an endorsement of Duncan Williams Asset Management by the SEC nor does it indicate that Duncan Williams Asset Management has attained a particular level of skill or ability.

This material prepared by Duncan Williams Asset Management is for informational purposes only and is accurate as of the date it was prepared. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Past performance is not indicative of future results. Investing involves risks, including the risk of loss of principal. Before making any investment decision, investors should consult with their financial advisor, consider their individual financial circumstances, and carefully review all relevant information and risk factors. Duncan Williams Asset Management assumes no responsibility for errors or omissions, nor does it accept liability for any loss arising from reliance on this information.

Advisory services are only offered to clients or prospective clients where Duncan Williams Asset Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Duncan Williams Asset Management unless a client service agreement is in place.

This material is not intended to serve as personalized tax, legal and/or investment advice since the availability and effectiveness of any strategy is dependent upon your individual facts and circumstances. Duncan Williams Asset Management is not a legal or accounting firm. Please consult with your legal or tax professional regarding your specific tax situation when determining if any of the mentioned strategies are right for you.

Investment Management Group (IMG)

The Investment Management Group at Duncan Williams Asset Management is led by a team with extensive experience in investment management, financial planning, and client service. President David Scully, CFA®, CFP®, has more than 20 years of experience and is active in Memphis civic organizations. Chief Investment Officer Kyle Gowen, CFA®, CFP®, oversees investment strategy and is engaged with the local community. Investment Analyst Jack Eason, CFA®, provides research and supports charitable initiatives. The IMG team is committed to professional standards, client service, and community involvement. No statement is intended as an offer of investment advice or a guarantee of future results.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119