Most people don’t need to choose between an HSA and a 401(k). The real question is which account to fund first, depending on your workplace benefits, taxes, cash flow, and expected health care costs.

A Health Savings Account (HSA) can be a helpful savings option if you qualify. You’re typically eligible if you have a high-deductible health plan, no other disqualifying coverage, aren’t enrolled in Medicare, and aren’t claimed as someone else’s dependent (see IRS Publication 969).

For 2026, the IRS HSA contribution limit is $4,400 for self-only high-deductible health plan coverage and $8,750 for family coverage, according to IRS Revenue Procedure 2025-19: https://www.irs.gov/irb/2025-21_IRB. Eligible individuals age 55 or older may contribute an additional $1,000 catch-up amount, according to IRS Publication 969: https://www.irs.gov/publications/p969.

401(k) limits are also meaningful. For 2026, the IRS increased the employee deferral limit for 401(k), 403(b), most governmental 457 plans, and the federal Thrift Savings Plan to $24,500, with a general catch-up contribution limit of $8,000 for participants age 50 and older, according to the IRS: https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500. A higher catch-up contribution limit of $11,250 applies in 2026 for eligible participants ages 60 through 63 in those plans, according to the same IRS announcement: https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500.

Why HSAs Deserve Attention

People often think of HSAs as just for medical expenses, but they can also help you save for the future. Your contributions may be tax-deductible, your savings can grow tax-free, and you won’t pay taxes on withdrawals if you use the money for qualified medical expenses (see IRS Publication 969).

With an HSA, you keep your money even if you don’t spend it by the end of the year. Your HSA goes with you if you change jobs or retire, so it’s useful for both current medical bills and future health care costs in retirement.

HSAs aren’t the best fit for everyone. If a high-deductible health plan would stretch your budget too much, or if you have high medical costs and little savings, it might not be wise to put extra money into an HSA.

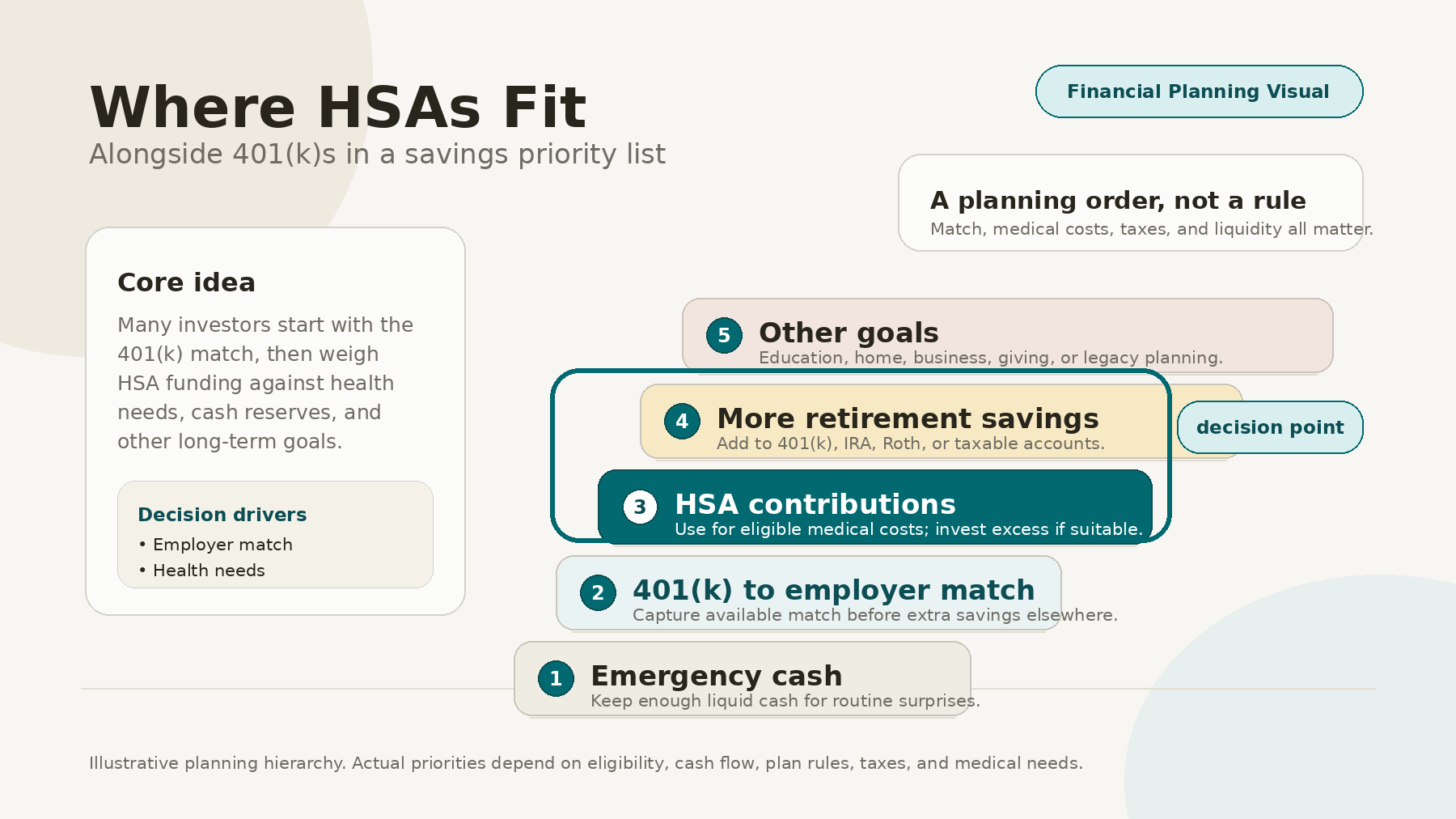

A Practical Savings Priority List

Many investors find it helpful to organize their savings in steps:

- Build a basic emergency reserve.

- Contribute enough to a 401(k) to capture the full employer match, if available.

- Fund an HSA based on expected health care costs and extended savings capacity.

- Increase retirement contributions to a 401(k), IRA, Roth IRA, or other retirement account.

- Save toward other goals, such as education, a home purchase, business needs, or taxable investment accounts.

This order isn’t the same for everyone. You should adjust it based on your health plan, employer contributions, debt, income, taxes, and your family’s medical needs.

Why the 401(k) Match Often Comes First

If your employer offers a 401(k) match, it’s usually smart to contribute enough to get the full match before putting money into other accounts. The match is a valuable benefit that’s part of your compensation.

For example, if your employer matches 50% of your contributions up to a certain percentage of your pay, not contributing enough means you’re missing out on part of your compensation. That’s why getting the full 401(k) match is often a top savings priority.

Once you’ve received the full match, the HSA can become a higher priority, especially if you have enough cash flow and can pay some medical costs out of pocket, letting your HSA investments grow.

Where the HSA May Move Ahead

For some investors, the HSA becomes the next savings priority after the 401(k) match. This may be especially true when:

The investor is enrolled in an HSA-eligible high-deductible health plan.

The household has enough emergency savings to handle deductible exposure.

The investor expects future health care expenses and wants to set aside tax-advantaged dollars for them.

The employer contributes to the HSA.

The investor has already captured the full 401(k) match.

Employer HSA contributions also matter. IRS Publication 969 states that employer contributions reduce the amount the employee or anyone else can contribute to the HSA for the year: https://www.irs.gov/publications/p969. In other words, if an employer contributes to your HSA, you should include that amount when tracking the annual contribution limit.

The Department of Labor has also noted that the mere fact that an employer contributes to an HSA does not, by itself, make the HSA an ERISA-covered plan, provided certain conditions are met: https://www.dol.gov/agencies/ebsa/employers-and-advisers/guidance/field-assistance-bulletins/2006-02.

When Health Needs Change the Order

Your health needs can affect your savings plan. If you’re healthy and have steady cash flow, you might feel comfortable putting more into your HSA and investing some of those contributions for future medical costs.

If your family has frequent doctor visits, prescriptions, or planned procedures, you might use your HSA mainly for current medical expenses. That’s still helpful, but you should match your contributions to your expected out-of-pocket costs, cash savings, and insurance deductibles.

The IRS defines a high-deductible health plan for 2026 as a plan with an annual deductible of at least $1,700 for self-only coverage or $3,400 for family coverage, with annual out-of-pocket expenses not exceeding $8,500 for self-only coverage or $17,000 for family coverage, according to Revenue Procedure 2025-19: https://www.irs.gov/irb/2025-21_IRB. Those deductible and out-of-pocket limits are important because a savings strategy that looks efficient on paper may not work if the household cannot comfortably absorb medical costs during the year.

Do Not Ignore Liquidity

A common mistake is focusing only on tax benefits when choosing accounts. Tax advantages are important, but having access to your money when you need it matters too.

HSA funds can be used tax-free for qualified medical expenses, but nonqualified distributions are generally taxable and may be subject to an additional 20% tax, according to IRS Publication 969: https://www.irs.gov/publications/p969. That means investors should avoid overfunding an HSA at the expense of emergency savings, especially if they may need the money for nonmedical purposes.

The same goes for 401(k) contributions. These accounts are meant for long-term savings, so be careful not to contribute so much that you end up needing credit cards, loans, or early withdrawals to pay for everyday expenses.

A Moderate Approach

For many people who qualify, a balanced savings plan might look like this:

First, maintain enough cash to avoid financial stress from routine surprises.

Second, contribute enough to a 401(k) to receive the full employer match.

Third, contribute to an HSA at least enough to cover expected out-of-pocket medical costs, if eligible.

Fourth, consider increasing HSA contributions toward the annual maximum if cash flow allows and health plan risk is manageable.

Fifth, continue building retirement savings in 401(k) s, IRAs, Roth IRAs, or taxable investment accounts, based on the wider financial plan.

The best order depends on your situation. If you have a generous 401(k) match, you might focus on the 401(k) first. If your employer puts money into your HSA and you have predictable medical costs, the HSA might come first. If you have high-interest debt, little emergency savings, or uncertain health care needs, it’s smart to focus on cash flow before putting more into either account.

The Bottom Line

HSAs and 401(k)s don’t have to compete. When you use both, you can tackle two of the biggest long-term financial needs: retirement income and health care costs.

The main thing is to avoid a one-size-fits-all approach. Your savings priorities should depend on factors like employer matches, HSA eligibility, deductibles, expected medical costs, tax rates, and cash reserves.

If you’re eligible and financially ready, an HSA can be more than just a way to pay for medical expenses. It can play a key role in your overall savings plan, along with your 401(k), IRA, emergency fund, and other long-term goals.

Sources

IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans:

https://www.irs.gov/publications/p969

IRS Internal Revenue Bulletin 2025-21, Revenue Procedure 2025-19, 2026 HSA and HDHP limits:

https://www.irs.gov/irb/2025-21_IRB

IRS announcement, 2026 401(k) and IRA contribution limits:

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500

U.S. Department of Labor, Field Assistance Bulletin No. 2006-02, HSA employer contribution guidance:

https://www.dol.gov/agencies/ebsa/employers-and-advisers/guidance/field-assistance-bulletins/2006-02

Disclosure

This material is for informational and educational purposes only and should not be considered personalized investment, tax, legal, or insurance advice. The information presented is based on sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Tax laws, contribution limits, and plan rules are subject to change. Investors should consult their financial advisor, tax professional, benefits administrator, or legal advisor before making decisions about HSA contributions, 401(k) deferrals, health plan elections, or retirement savings strategies. Investing involves risk, including the possible loss of principal, and no strategy can guarantee a profit or protect against loss.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119