For many people, filing a tax return feels like crossing the finish line. Once the return is sent off and the refund or payment is handled, most of us set taxes aside until next year.

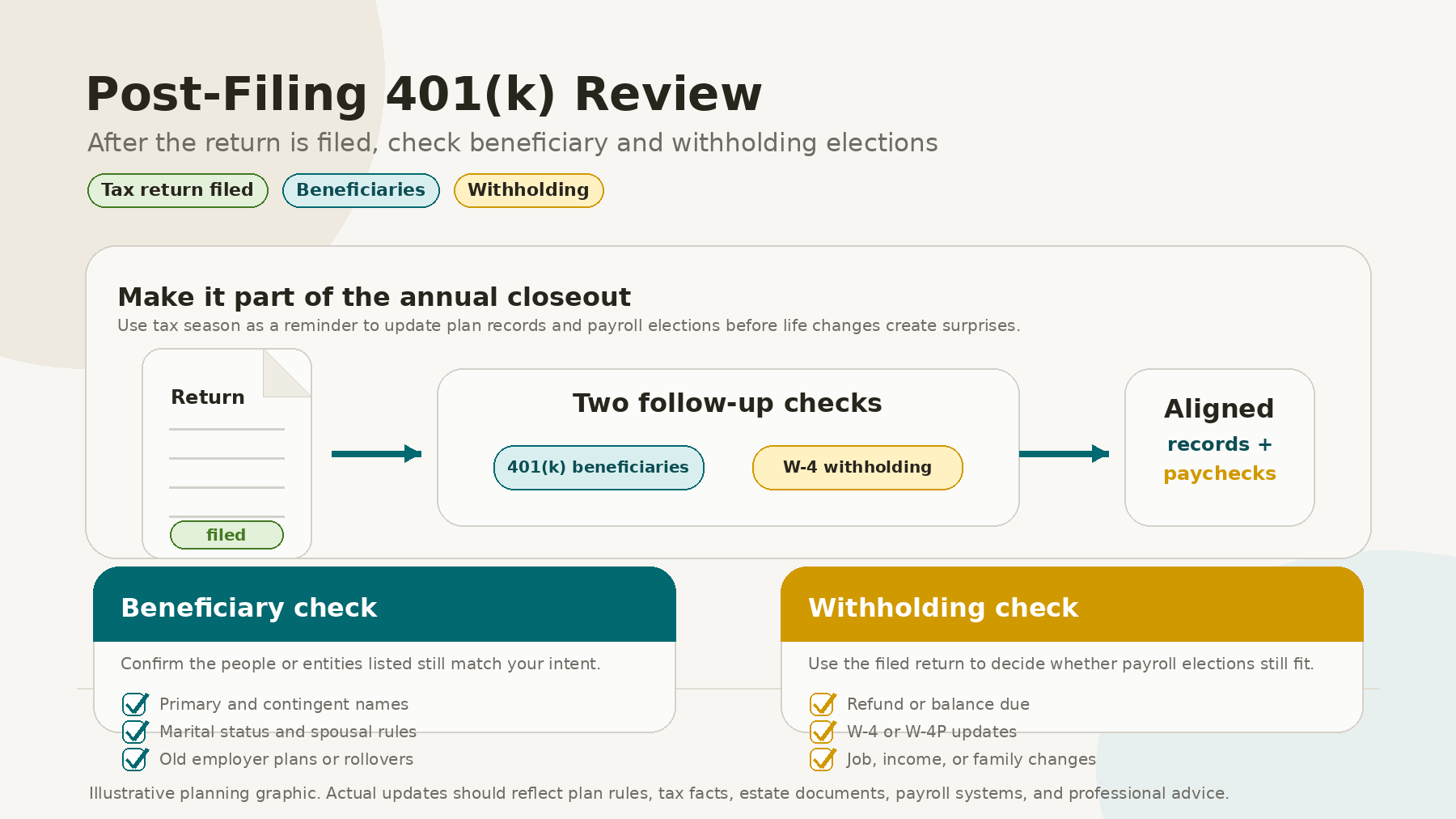

But tax season can also be the perfect reminder to do a brief financial checkup. After filing, it’s a good time to pay special attention to two things: your 401(k) beneficiaries and your tax withholding.

These are easy details to overlook, and they can easily become outdated. Yet both have a real impact on your financial life.

Why Post-Filing Is a Good Time to Review

After filing, you usually have all your latest info handy—like your income, taxes, retirement contributions, and any changes at home. That makes it a natural time to ask: do your key choices still fit your current life?

This review doesn’t have to be complicated. Think of it as a short, annual checklist:

Review 401(k) beneficiary designations.

Confirm the plan's marital status and contact information.

Check whether the beneficiary data is complete and up to date.

Review paycheck withholding.

Consider whether a new Form W-4 is needed.

Coordinate with a financial consultant, tax professional, and benefits administrator when appropriate.

Taking a few minutes now can help you avoid paperwork headaches or unexpected issues down the road.

Beneficiary Designations Can Become Stale

Your 401(k)-beneficiary form decides who gets your account if something happens to you before it’s paid out. It’s one of the most important forms in your retirement plan.

The Department of Labor notes that when reviewing defined contribution plan statements, including 401(k) plan statements, participants should check their beneficiary designation and marital status: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa.pdf.

It’s not only about having a beneficiary listed—it’s about making sure it still matches your wishes today.

Beneficiary choices can sit in your file for years—sometimes decades—without being checked. That’s why it’s so easy for them to get out of date and not reflect what you want now: https://www.dol.gov/sites/dolgov/files/ebsa/pdf_files/2012-current-challenges-and-best-practices-concerning-beneficiary-designations-in-retirement-and-life-insurance-plans.pdf.

Life Events Should Trigger a Review

A post-filing review is especially important if there was a major life event during the prior year. Examples include:

Marriage

Divorce

Birth or adoption of a child

Death of a spouse or other beneficiary

A child reaching adulthood

A change in estate planning documents

A move to another state

A new job or rollover

A change in family relationships

The ERISA Advisory Council report highlighted the importance of assessing and revising beneficiary designations after life events like marriage, divorce, the birth of a child, or the death of a spouse: https://www.dol.gov/sites/dolgov/files/ebsa/pdf_files/2012-current-challenges-and-best-practices-concerning-beneficiary-designations-in-retirement-and-life-insurance-plans.pdf.

This is especially important because your will or trust doesn’t always override what’s on your retirement plan’s beneficiary form. Make sure your 401(k) beneficiaries match your broader estate plan, but don’t assume one will automatically update the other.

Spousal Rules Matter

401(k) beneficiary rules may differ from ordinary account titling rules. In many 401(k) and other defined contribution plans, if a participant dies before receiving benefits, the surviving spouse will automatically receive them unless proper steps are taken to name someone else, according to the Department of Labor: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa.pdf.

The Department of Labor also notes that if a participant wants to select a different beneficiary, the spouse generally must consent by signing a waiver witnessed by a notary or plan representative: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa.pdf.

That’s why it’s so important to keep your marital status up to date on your plan. If you got married after enrolling, be sure to let your employer or plan administrator know and revise your records: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa.pdf.

What to Check on the 401(k) Beneficiary Side

A practical post-filing review may include the following questions:

Is there a beneficiary on file?

Are both primary and contingent beneficiaries listed?

Are names spelled correctly?

Are addresses, dates of birth, or other identifying information complete?

Does the beneficiary designation match current wishes?

Does it correspond to the estate plan?

Has a divorce, marriage, death, or birth changed the intended plan?

Does the plan require spousal consent for any changes?

Are old employer plans or rollover accounts also updated?

When you make any changes, save the confirmation. Keep screenshots, plan emails, or dated copies of forms—these can help if questions ever come up.

Withholding Elections Deserves the Same Annual Check

The second part of the post-filing review is tax withholding.

If you got a big refund or owed more than expected, it could mean your paycheck withholding isn’t quite matching your tax situation. A large refund might mean too much was withheld; a big tax bill might mean too little. Neither is necessarily good or bad, but both are worth a second look.

The IRS Tax Withholding Estimator is designed to show how withholding affects a taxpayer’s refund, paycheck, or tax due, and it can help estimate the correct amount of tax an employer or pension provider should withhold each year: https://www.irs.gov/individuals/tax-withholding-estimator.

The IRS says the estimator can generate a pre-filled Form W-4 or Form W-4P to update withholding with an employer, pension provider, or payroll or human resources system: https://www.irs.gov/individuals/tax-withholding-estimator.

When to Consider Updating Withholding

Withholding should be reviewed after filing and after any life changes. The IRS says taxpayers should check withholding when tax law changes or life changes occur, including marriage, divorce, birth or adoption of a child, home purchase, retirement, job changes, or changes in taxable income not subject to withholding: https://www.irs.gov/newsroom/tax-withholding-how-to-get-it-right.

Common reasons to revisit withholding include:

The refund was either much larger or much smaller than expected.

The taxpayer owed more than expected.

A spouse started or stopped working.

There was a second job or side income.

Investment income increased.

A child was born or aged out of a credit.

Itemized deductions changed.

Retirement or pension income began.

A taxpayer started making estimated payments.

The IRS says employees can use the Tax Withholding Estimator results to determine whether they should complete a new Form W-4 and submit it to their employer, rather than filing it with the IRS: https://www.irs.gov/newsroom/tax-withholding-how-to-get-it-right.

What Records to Gather

The post-filing review works best when the right documents are nearby. The IRS says taxpayers using the Tax Withholding Estimator should have recent paystubs for jobs, pensions, or annuities, and if filing jointly, the spouse’s recent paystubs as well: https://www.irs.gov/individuals/tax-withholding-estimator.

The IRS also says taxpayers may need the most recent federal tax return, payment records for self-employment, gig work, or Social Security, and expense records if they plan to itemize deductions or claim adjustments: https://www.irs.gov/individuals/tax-withholding-estimator.

For 401(k) beneficiary elections, investors should gather current plan statements, login credentials, estate planning documents, and any confirmation of prior beneficiary designations.

Make It a Repeatable Checklist

The value of a post-filing review is consistency. Rather than waiting for a major event, investors can build a short annual routine.

A practical checklist may look like this:

Save a copy of the filed tax return.

Record the refund or balance due.

Review paycheck withholding using the IRS estimator.

Submit a new Form W-4 if needed.

Log in to the 401(k)-plan portal.

Confirm beneficiary designations.

Review marital status and contact information.

Update beneficiaries after any major life event.

Check old employer plans and rollover accounts.

Save confirmations of any changes.

This whole review might take less than an hour, but it can help you prevent problems between your financial plans and the forms that control them.

The Bottom Line

Filing your tax return shouldn’t mark the end of tax season. Instead, think of it as the start of a brief financial tune-up.

For 401(k) participants, that means checking beneficiary designations, confirming marital status, and ensuring plan records reflect current intentions. For taxpayers, it means reviewing whether withholding still fits the household’s income, deductions, credits, and expected tax liability.

These aren’t dramatic changes—they’re just good maintenance. But taking care of these details, each year can help you avoid surprises and keep your finances on track as life changes.

Sources

IRS, “Tax Withholding Estimator”

https://www.irs.gov/individuals/tax-withholding-estimator

IRS, “Tax withholding: How to get it right”

https://www.irs.gov/newsroom/tax-withholding-how-to-get-it-right

U.S. Department of Labor, “FAQs about Retirement Plans and ERISA”

https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa.pdf

U.S. Department of Labor, ERISA Advisory Council, “Current Challenges and Best Practices Concerning Beneficiary Designations in Retirement and Life Insurance Plans”

https://www.dol.gov/sites/dolgov/files/ebsa/pdf_files/2012-current-challenges-and-best-practices-concerning-beneficiary-designations-in-retirement-and-life-insurance-plans.pdf

Disclosure

This material is for informational and educational purposes only and should not be considered personalized investment, tax, legal, estate planning, or financial planning advice. Tax laws, withholding rules, retirement plan rules, beneficiary requirements, spousal consent rules, and estate planning considerations may change and may vary by plan or jurisdiction. Investors should consult their financial advisor, tax professional, estate planning attorney, benefits administrator, or legal advisor before changing withholding elections, 401(k) beneficiary designations, estate planning documents, or other financial planning arrangements. Investing involves risk, including the possible loss of principal, and no strategy can guarantee a profit or protect against loss.

Recent Articles

Let's talk about your future.

Connect with a local Duncan Williams Asset Management advisor

5350 Poplar Ave.

Suite 600

Memphis, TN 38119